The best refinances save thousands, but a new loan can accomplish other goals like turning equity into cash, removing a co-borrower, and more.

Is now a good time to refinance? A few years ago, with mortgage rates at historic lows, the answer for millions of Americans was yes.

But that was then. Rates have since returned to market norms, and it’s hard to predict where they’ll go next.

“Whether or not to refinance isn’t always a cut-and-dry answer,” said Erik Schmitt, digital channel executive at Chase Home Lending. “It really depends on the specific homeowner’s situation.”

Reasons to Refinance

Refinancing pays off your current mortgage and rolls the debt into a new loan.

The new loan should be better, in some way, than your current loan. The new loan should provide benefits such as:

Lower monthly payments: Locking in a lower rate on the new loan, or stretching the debt across a longer term, should lower monthly payments

Lower lifetime interest costs: Getting a new mortgage with a shorter term can slash the amount of lifetime interest due. (There’s a tradeoff: This will usually increase the monthly payment)

Access to home equity: Money borrowed from home equity with a cash-out refi could pay for home improvements, college tuition, debt consolidation, or even a wedding

A better loan type: A mortgage that made sense on closing day may no longer be your best choice. For example, a homeowner who got an adjustable-rate mortgage (ARM) may want to refinance into a loan with a fixed rate

Removing a co-borrower: People who co-signed with an ex or a parent can refinance later to remove the co-borrower — but only if they can qualify for the new loan based on their personal finances alone

Most people refinance to save money. “That said, the need for (other kinds of) financial stability can be very real,” said Sara Levy-Lambert, vice president of growth at Red Awning, which helps people finance vacation rentals.

“If long-term goals are on the board, then refinancing can make way for financial liberation in the long run,” Levy-Lambert said.

Borrowers with other goals, like taking out cash or locking in a fixed rate and level payment, should still compare mortgage rates and fees, she said. Finding the best deal on a new loan could save thousands.

When Should You Refinance Your Mortgage?

A homeowner should refinance when a new mortgage can improve their financial life in a way their current loan can’t.

A new refinance could:

1. Lower the Interest Rate

The New York Fed estimates about a third of all Americans with open mortgages refinanced between the fall of 2020 and the spring of 2022. Historically low rates during those months sparked this refinance boom.

Homeowners who bought their homes back then, when rates were uncommonly low, probably won’t find a lower rate today, though some homeowners can still lower their rate.

For the lower rate to pay off, homeowners should aim for a rate reduction of about 1 percent. Statistics show a rate reduction of less than 1 percent won’t save enough money to cover the cost of the refinance.

Calculating Your Break-Even Point

When will a lower interest rate start saving money? The answer depends on your loan’s break-even point. The break-even point is the month when your loan’s savings outweigh your loan’s upfront costs.

For instance, if you paid $15,000 in closing costs to refinance, how long would it take to get that $15,000 back? If the new loan saves you $400 a month, your breakeven point would arrive in about 38 months — just over three years.

Selling the home or refinancing again before the break-even point means you’d lose money on the refinance.

Learn how to find your break-even point here.

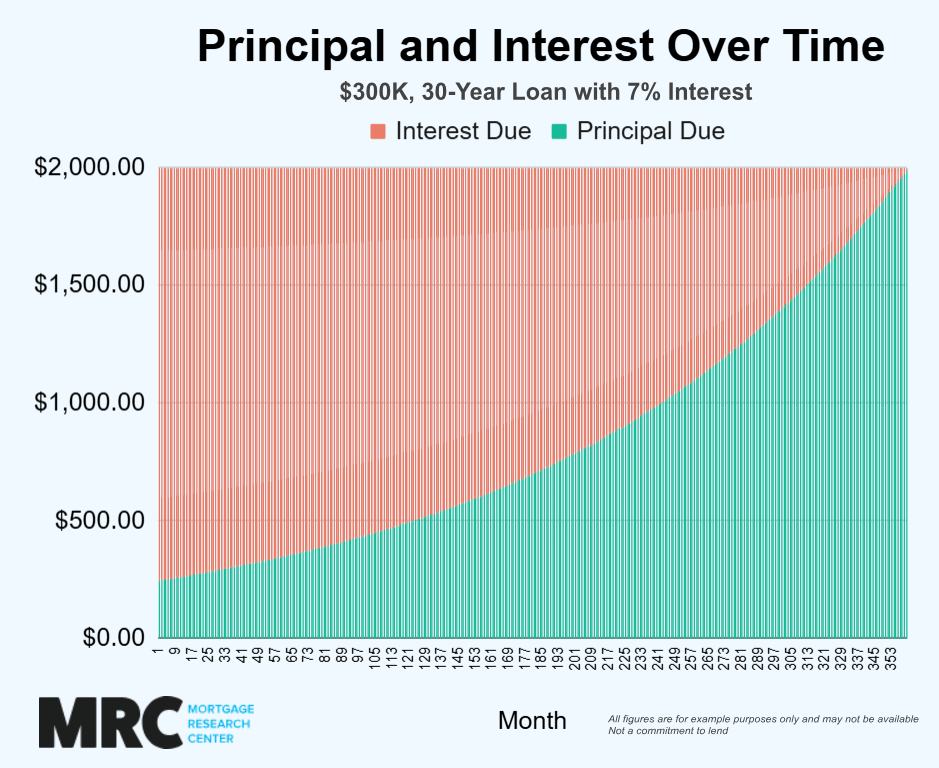

2. Shorten the Term to Save Money in the Long Run

Shorter loan terms — replacing a 30-year loan with a 15-year loan, for example — have a couple benefits.

First, shorter loan terms typically charge lower interest rates than longer terms for the same borrower refinancing the same home. But that’s not where the big savings come from.

Homeowners can save massive amounts of money in interest by switching to a shorter term.

This example shows interest due on a $300,000 mortgage at an example rate of 6.125% for different loan terms:

| Loan Term | Total Interest Paid | Monthly P&I Payment |

|---|---|---|

| 10-year term | $101,937 | $3,349 |

| 15-year term | $159,337 | $2,552 |

| 30-year term | $356,219 | $1,823 |

All figures are for example purposes only.

Those are six-digit savings. But notice how the monthly payment increases as the total interest due decreases. This is the tradeoff. Shorter terms give the lender less time to charge interest, but they also leave less time for the borrower to pay off the principal.

Can’t afford the bigger payment on a shorter term loan? Making extra payments on a 30-year mortgage can create a similar effect. For example, if you get a big tax refund each spring, you could put that windfall directly onto your loan’s principal balance. The results can be powerful.

Of course, the lower the new loan’s interest rate, the more money a shorter term can save.

3. Change Your Loan Type

Some homeowners outgrow their mortgage before they pay it off. A refinance can fix this. Refinancing closes the current loan and opens a new one, creating a chance to get a loan that better fits your current life.

Common loan type refinance scenarios include:

Replacing an ARM with a fixed-rate loan: After the initial fixed-rate period expires, rates and payments on adjustable-rate mortgages (ARMs) will change each year. Some homeowners refinance into a fixed rate to avoid this instability

Getting a conventional loan to cancel FHA fees: Conventional private mortgage insurance expires when the loan’s balance reaches 78 percent of the home’s value. (And borrowers can actually cancel PMI a little sooner.) FHA mortgage insurance premiums (MIP) usually apply for the life of the loan. Refinancing out of FHA ends the loan’s life early

Converting a primary residence to a rental: Government-insured loans (FHA, VA, USDA) and some special conventional programs finance only residences the borrower plans to live in. A homeowner who wants to convert a primary residence to a rental or vacation home will need a refinance

The best refinances achieve these goals while also cutting the mortgage rate or shortening the loan’s term.

4. Renovate Your Home

Home renovations cost a lot, but by doing the right projects, renovations could also make the home more valuable. A refinance can help fund renovations.

Refinancing through the FHA’s 203K loan program, for example, leverages the home’s equity to pay for home renovations. This type of refinance combines two loans into one:

First, the loan pays off the existing mortgage

Then, additional money built into the loan pays for the renovations

FHA 203k funds can’t pay for a pool or a pickleball court, but they can pay for cosmetic or functional kitchen and bath upgrades, major maintenance projects like roofs and plumbing systems, projects to increase the home’s energy efficiency, and improvements that make the home more accessible.

Homeowners who need fewer limits on their renovation projects should use a cash-out refinance.

5. Access Equity As Cash

A cash-out refinance pays off the current mortgage while also paying out additional cash to the homeowner.

For example, if your home is worth $350,000 but you owe only $200,000 on the mortgage, you’d have $150,000 in equity. A cash-out refinance could pay off your $200,000 loan balance while also taking cash from your $150,000 in equity.

This extra cash isn’t free. It’s added into the new loan, increasing your mortgage debt. The new must be repaid, with interest, so this asset should be reinvested in the future, not used to cover living expenses or to pay for a vacation.

The best cash-out refinances pay off high-interest debts to save on interest, pay for college tuition that unlocks a higher earning potential, finance home improvements that increase the home’s value, or cover any other need that should pay off later.

Related: How Much Does a Cash-Out Refinance Cost?

6. Add or Remove a Borrower

Removing a co-borrower from a mortgage loan will often require a refinance into a new loan.

Why? Because the family member or friend who co-signed on your mortgage was key to the loan’s approval. For a typical lender, removing a co-borrower after the loan has been approved would be like removing part of your home’s foundation after you’ve moved in.

Some lenders or loan servicers make exceptions, especially if the remaining borrower can show they have the income, debt ratio, and credit history to continue making payments.

However, many lenders will require a full refinance. Divorcing spouses can face this dilemma. Some spouses who plan to keep the home can use a cash-out refinance to pay out their ex’s share in equity.

Adding a co-borrower? This will usually require a full refinance, too. Depending on the new co-borrower’s personal finances, among other variables, adding the borrower could lower the loan’s mortgage rate.

Refinancing should be seen strategically. The timing and financial commitment should make sense for your long-term objectives.

When Not to Refinance

“Refinancing should be seen strategically,” said Ali Zane, a credit consultant at Imax Credit Repair Firm. “The timing and financial commitment should make sense for your long-term objectives.”

Your timing may be off when:

1. You Might Sell the Home Soon

Refinancing costs money upfront, in the form of closing costs, but the savings from the new loan happen gradually, in the form of lower monthly payments.

Selling the home too soon stops the new loan from ever paying off, meaning the new loan, even with its lower rate, wound up costing you money.

And keep in mind other incentives for refinancing, like changing the loan type or eliminating mortgage insurance, will no longer matter after the home has sold. So if there’s a good chance you’ll sell the home within a year or two, just hang onto the current mortgage and its problems until then.

2. You’ve Had Your Current Mortgage Too Long

Lower mortgage rates could end up costing more if you refinance a loan that’s almost paid off.

Lenders’ amortization schedules collect most of a loan’s interest in the first half of the loan’s term. Starting a new 30-year schedule over, from Month 1, even at a lower rate, could mean more net interest paid on the same house.

That said, if you need to refinance an older mortgage, try to get a shorter term, like a 12- or 15-year loan. These can keep you on track to save.

3. Your Interest Rate Will Go Up

Accepting a higher interest rate on a large loan balance should always be a last resort.

In this example, you can see how payments and lifetime interest on a loan balance of $300,000 change as the interest rate goes up:

| Interest Rate | P&I Payment | Total Interest |

|---|---|---|

| 4% | $1,432 | $215,609 |

| 5.5% | $1,707 | $313,212 |

| 7% | $1,996 | $418,527 |

All figures are for example purposes only.

To some borrowers, paying an extra 1.5 percent in interest might not seem like much, but for a loan this size, 1.5 percent adds about $100,000 to the loan’s lifetime costs. This will likely undermine any savings the loan could provide.

Of course, there are exceptions: Homeowners refinancing out of an adjustable-rate mortgage might still save with a higher interest rate. These borrowers have to consider whether their ARM’s rate will climb even higher than the fixed rate they could lock in today. (The ARM’s lifetime rate cap can help them decide.)

4. You Don’t Really Need the Cash

Equity is a form of wealth homeowners can access by getting a cash-out refinance (or a second mortgage). But, borrowing from equity also increases mortgage debt and monthly payments.

So homeowners shouldn’t refinance to access equity unless the new loan is worth the borrowing costs and loss of equity.

The best uses of borrowed equity include:

making the home more valuable through renovations

consolidating punitive debt payments that threaten the homeowner’s ability to make mortgage payments

paying tuition that leads to a higher earning career

making a down payment on a second home or investment property

This list does not include using equity to pay for a new car or a vacation or any other temporary need.

How Much Can You Save by Refinancing?

Below is a table of estimated savings if you reduce your rate by 0.25%, 0.50%, or 1.0%. To find your breakeven point in months, divide your closing costs by monthly savings.

Monthly Savings by Rate Reduction*

| Loan Balance | 0.25% | 0.50% | 1.00% |

|---|---|---|---|

| $75,000 | $13 | $25 | $50 |

| $100,000 | $17 | $34 | $67 |

| $125,000 | $21 | $42 | $84 |

| $150,000 | $26 | $51 | $101 |

| $175,000 | $30 | $59 | $118 |

| $200,000 | $34 | $68 | $134 |

| $225,000 | $38 | $76 | $151 |

| $250,000 | $43 | $85 | $168 |

| $275,000 | $47 | $93 | $185 |

| $300,000 | $51 | $102 | $201 |

| $325,000 | $55 | $110 | $218 |

| $350,000 | $60 | $119 | $235 |

| $375,000 | $64 | $127 | $252 |

| $400,000 | $68 | $136 | $269 |

| $425,000 | $72 | $144 | $285 |

| $450,000 | $77 | $153 | $302 |

| $475,000 | $81 | $161 | $319 |

| $500,000 | $85 | $170 | $336 |

| $550,000 | $94 | $187 | $369 |

| $600,000 | $102 | $203 | $403 |

| $650,000 | $111 | $220 | $436 |

| $700,000 | $119 | $237 | $470 |

| $750,000 | $128 | $254 | $504 |

| $800,000 | $136 | $271 | $537 |

| $850,000 | $145 | $288 | $571 |

| $900,000 | $153 | $305 | $604 |

| $950,000 | $162 | $322 | $638 |

| $1,000,000 | $170 | $339 | $671 |

| $1,100,000 | $187 | $373 | $739 |

| $1,200,000 | $204 | $407 | $806 |

| $1,300,000 | $221 | $441 | $873 |

| $1,400,000 | $239 | $475 | $940 |

| $1,500,000 | $256 | $509 | $1,007 |

| $1,600,000 | $273 | $543 | $1,074 |

| $1,700,000 | $290 | $577 | $1,141 |

| $1,800,000 | $307 | $610 | $1,209 |

| $1,900,000 | $324 | $644 | $1,276 |

| $2,000,000 | $341 | $678 | $1,343 |

*Assumes current rate of 7.5%. All figures are estimates and depend on the interest rate and age of your current loan.

A mortgage refinance is a financial tool, one that performs differently in different circumstances.

At its best, a refinance can save thousands of dollars a year and hundreds of thousands over the life of a loan.

The following scenarios show which costs to consider when refinancing. You can also plug your own numbers into a refinance calculator to measure your costs.

Best Case Scenario: Large Rate Reduction

Someone who got a $300,000 mortgage in August of 2018 at a rate of 4.5% would have started homeownership with:

$1,520: Monthly principal and interest payments

$247,220: Lifetime interest due if loan paid on schedule

In December of 2020, when rates hit 2.7%, this homeowner refinanced into a new loan with:

$1,217: Monthly principal and interest payments

$138,045: Lifetime interest due if loan paid on schedule

By shaving almost 2 percentage points, this borrower saves $303 a month and $3,636 a year. The new loan would require $109,175 less in interest over its 30-year term than the old loan.

Even after taking out the $37,000 or so the homeowner has already paid in interest on the original loan, the new loan saves more than $72,000.

This borrower paid $8,000 in closing costs upfront to refinance. To recoup this loss, the borrower will need to keep the new loan for at least 27 months, just over two years. After reaching that break-even point, every additional monthly payment will save another $303.

So-So Scenario: Average Rate Reduction

Let’s say the borrower in the scenario above had a few credit blemishes in December of 2020 and couldn’t get that 2.7% rate. Instead, the homeowner qualified for a rate of 3.5%, 1 percentage point below their current rate of 4.5%.

This rate reduction would lower costs from:

$1,520: Monthly principal and interest payments

$247,220: Lifetime interest due if loan paid on schedule

to:

$1,347: Monthly principal and interest payments

$184,968: Lifetime interest due if loan paid on schedule

This saves $173 a month and $2,076 a year. The new loan also charges $62,252 less than the current loan. It looks OK at first glance, but now the $37,000 or so in interest already paid on the old loan is more significant. It eats up more than half of the loan’s savings.

And that $8,000 spent on closing costs? It’ll take nearly four years of monthly payments on the new loan to save those costs.

If the homeowner really needs the $173 in monthly savings, this refi is a great deal. If not, it’s just an average deal because there’s a better chance the borrower will sell or refinance again before saving money long-term.

Questionable Scenario: Small Rate Reduction

Now let’s say the homeowner can save only 0.5%, lowering the rate to 4%, taking the figures from:

$1,520: Monthly principal and interest payments

$247,220: Lifetime interest due if loan paid on schedule

to:

$1,432: Monthly principal and interest payments

$215,609: Lifetime interest due if loan paid on schedule

The $31,611 saved in lifetime interest is less than the $37,000 already paid in interest on the old loan, so we’ll add that difference — $5,389 — to the new loan’s costs. Combined with the $8,000 in closing costs, the refinance cost $13,389.

Yes, the loan saves $88 a month, but it’ll take nearly 13 years for the $88 in monthly savings to equal the $13,389 spent. Most borrowers would do best to skip this refinance.

Exceptions: Achieving Another Goal

Even the worst scenario above could still help someone who is refinancing for another purpose:

To get an ex-spouse off the loan

To access equity for an urgent and long-term need

To lock in a fixed rate before an ARM’s rate starts to soar

But some people can achieve these goals without refinancing.

Alternatives to Refinancing

Because refinancing closes the old mortgage, it’s the ultimate solution to the old mortgage’s problems. But some borrowers can find less aggressive solutions, including:

Mortgage recasting: If you’re ahead of schedule on a loan, the lender may be willing to recast the balance over a new schedule. This could lower payments without standard refi costs.

Loan modifications: A borrower in danger of falling behind on the mortgage should ask for a loan modification. The lender doesn’t have to provide this, but most lenders can be more flexible when borrowers ask for help before falling behind on the loan’s payments.

Streamline Refinancing: When market rates fall below the rate on your FHA, USDA, or VA loan, a Streamline Refinance could help lower payments at a lower upfront cost. Conventional borrowers won’t have this option.

Second mortgages: Home equity loans and home equity lines of credit (HELOCs) borrow against a home’s equity without refinancing the primary mortgage. Borrowers keep making their existing mortgage payments while adding a second payment.

If a refinance costs as much as, or more than, the current loan, these alternatives will be worth pursuing.

It’s All About Timing and Your Specific Goals

Like any financial tool, a mortgage refinance works best when used in the right way and at the right time.

The best refinances set homeowners on a path to more financial stability by achieving specific goals or saving lots of money.

Interest rates aren’t the only factor to consider, but they’re at the center of conversations about any new mortgage for a reason: They, along with upfront fees, help set the new loan’s potential to save and achieve goals.

Take the next step in your refinance process by exploring rates here.