USDA Loan Pre-Approval: Everything You Need to Know

USDA loan pre-approval provides an accurate idea of the loan size you may qualify for and gives you a competitive advantage when making offers on homes.

If you're considering purchasing a home in a rural or suburban setting, a USDA-backed mortgage could help you buy with no money down and a competitive interest rate. But before you get serious about home shopping, you will want to apply for USDA loan pre-approval.

What Does It Mean to Be Pre-Approved for a USDA Loan?

Pre-approval is the first step in obtaining a mortgage from a USDA-affiliated lender. This initial process involves a comprehensive look into your:

Credit profile

Employment and earnings history

Existing debts

Other financial qualifications

Borrowers who qualify for a USDA loan are given a pre-approval letter outlining the maximum loan amount they're eligible for and the interest rate they're likely to receive.

Getting pre-approved does not mean you are guaranteed a USDA-backed mortgage. However, it does provide you with peace of mind that you meet the agency's requirements and can reasonably expect to receive financing to purchase your home.

Getting Pre-Approved is Different From Prequalifying

Prequalification is based on self-reported figures that you provide to a lender. Pre-approval uses documentation from your credit report, tax returns, and bank/asset statements.

Although prequalification can help prospective homebuyers establish a price range for which they may be eligible, it does not carry the same weight as being pre-approved for a loan. If you're serious about purchasing a home with a USDA loan, you will want to go through full USDA pre-approval.

Why Should You Apply for USDA Loan Pre-Approval?

Pre-approval is a vital part of the home shopping process. While it does not assure you a mortgage, it gives you more certainty that you can obtain a loan than simply being prequalified.

Plus, USDA loan pre-approval shows sellers that you are serious about buying and can give you an advantage in getting your offers accepted. Many real estate professionals will only work with buyers who have obtained a pre-approval letter from their lender.

Another advantage of getting fully pre-approved for a USDA loan is that it can save you time once you have a property under contract. While lenders are typically able to verify your financial information within a few days, this process may take longer when documents are missing or for applicants with complex situations, such as those who own their own business or are otherwise self-employed.

“One of the biggest traps is underestimating the processes involved; while it's important for responsible lending to take place, the actual process can take a lot longer than you're used to,” according to Sief Khafagi, co-founder of short-term rental investment platform Techvestor.

Time is short when buying a home. Even a brief delay can impact your ability to close on time, putting your purchase (and earnest money deposit) at risk.

One of the biggest traps is underestimating the processes involved; while it's important for responsible lending to take place, the actual process can take a lot longer than you're used to.

Requirements for USDA Loan Pre-Approval

USDA loan pre-approval involves meeting the eligibility requirements established by the USDA for its Single Family Housing loan program. While lenders are free to set their own standards, meeting these basic eligibility guidelines means you're likely to find a mortgage company willing to issue you a loan.

Credit Score

The USDA does not have a fixed credit score requirement for the residential mortgages it insures. This means that borrowers who cannot qualify for other types of mortgages due to their low credit score may still be eligible for a USDA-backed loan.

However, many lenders look for a credit score of at least 640, which is the lowest eligible for instant approval through the USDA's Guaranteed Underwriting System. Borrowers with lower scores can still be approved through manual underwriting, although not all mortgage companies offer this option.

Applicants with little to no credit history who do not have a reported credit score are still eligible for USDA loan pre-approval through a non-traditional credit history. This involves analyzing tradelines with at least a 12-month payment history, such as rent, utilities, auto loans, and insurance premiums.

Debt-to-Income Ratio

USDA guidelines allow borrowers to have a debt-to-income (DTI) ratio as high as 41%. This ratio represents the portion that your monthly debt payments — which includes your future housing costs — make up of your total qualifying income.

In addition to the loan you’re applying for, your DTI is comprised of installment obligations such as:

Auto loans

Credit card minimums

It does not include expenses like your utility bills, cellphone payments, or monthly subscription fees.

Applicants with positive compensating factors such as at least two years of continuous employment or a suitable cash reserve may qualify for a debt ratio waiver, allowing for a total DTI of 44%.

Household Income Limits

One unique requirement of getting pre-approved for a USDA loan is meeting the program's household income limits. These limits apply to all adults who will be sharing the home, not just the mortgage applicants.

Income limits vary by location and household size. However, most communities have a maximum limit of $112,450 for households of up to four members and $148,450 for households between five and eight. Areas with an elevated cost of living may have higher limits.

Other Things to Keep In Mind

If you’re planning to get pre-approved for a USDA loan, there are a few other things to keep in mind that could impact the full approval of your mortgage:

Eligible Property Locations: The USDA home loan program is designed to improve homeownership in designated rural and suburban areas. Locales are typically allowed to have up to 20,000 residents. However, exceptions apply for some communities with rural characteristics where the population is as high as 35,000. Check USDA’s eligibility map to make offers in eligible areas only.

Property Restrictions: Unlike most mortgage programs, you cannot take out a USDA loan to purchase a multifamily rental property – even if you plan to occupy one of the units as your primary residence.

Minimum Property Requirements: All loans must meet the USDA's minimum property requirements, which restrict properties with problems like structural deterioration or foundation issues, leaking or overly-layered roofs, non-functional HVAC systems, and unrepaired termite damage.

Non-Occupant Cosigners: If you plan to have a friend or family member cosign on your mortgage to help you qualify, you will only be pre-approved for a USDA loan if they’re going to reside in the home. Unlike other mortgages, the USDA program does not allow for non-occupant cosigners.

“Determining eligibility can be a bit of a challenge, so make sure the property is in a qualified rural area and that your income meets the requirements,” advises Mike Roberts, co-founder and CEO of City Creek Mortgage. “Once you're in the system, though, the process is pretty streamlined.”

Documents Needed for USDA Loan Pre-Approval

Since USDA mortgage pre-approval requires a full assessment of your credit and finances, your lender will request various documents to process your loan estimate. While the paperwork necessary can depend on your individual situation and financial profile, some common items you may need include:

Government-issued photo ID

Recent paystubs or other proof of employment

Two years of W-2 or 1099 forms

Two years of filed and accepted federal tax returns if self-employed

Two months of bank statements

Two months of asset/investment account statements (if applicable)

Documentation of court-ordered payments such as alimony or child support (if applicable)

How Long Does USDA Pre-Approval Last?

Pre-approval letters typically last 60 to 90 days, but that doesn't mean you shouldn't apply earlier. Talking to a lender well in advance of when you plan to buy can make you aware of potential problems and give you an appropriate amount of time to rectify any issues.

Some reasons why it’s better to get USDA pre-approval sooner than later are:

Your actual credit score may be lower than you think

Errors on your credit report can impact your loan eligibility

Your income level may not support the price range you’re considering

You will be ready to make an offer if you chance upon the perfect home

Lenders Can Cancel Your Pre-Approval

Pre-approval doesn't mean you're guaranteed a mortgage. In some cases, particularly when you have a significant change in your finances, such as losing your job or taking out another type of loan, a lender can revoke your pre-approval. This can also happen when interest rates rise, pushing your payment and DTI above acceptable levels.

Do You Have to Use the USDA Lender That Pre-Approves You?

Getting pre-approved for a loan does not mean you're locked into using the first mortgage provider who pre-approves you. In fact, experts recommend that you shop around with at least three different USDA lenders to ensure you're getting the best rate and lowest closing costs.

Applying for pre-approval with multiple companies does not have any additional impact on your credit score so long as you do so within 45 days of your initial application. Credit checks within this timeframe are recorded as a single inquiry on your credit report.

You can even change lenders after you get a property under contract, although doing so has the potential to delay the underwriting process and your full loan approval.

In most cases, you should decide on a lender prior to choosing a home, although well-qualified borrowers without a complex loan application may still be able to switch companies soon after signing a purchase agreement and still be able to close on time.

Alternatives to a USDA-Backed Mortgage

While the USDA residential mortgage program offers competitive rates and flexible credit requirements, it may not be the best option for all borrowers. That's because it:

Restricts you to specific geographic locations

Has income limits based on all adults in your household

Places lower limits on your DTI, which means less purchasing power

May make your offers less appealing to sellers compared to a traditional loan

Before deciding to go ahead with USDA loan pre-approval, make sure to consider these other mortgage programs as well.

Conventional Loans

Conventional loans are mortgages issued by private lenders and not insured by a government agency such as the USDA. The majority of these loans are conforming, meaning they follow the lending guidelines established by Fannie Mae and Freddie Mac. Credit requirements may be higher than with USDA-backed mortgages, but conventional loans tend to be otherwise more flexible for qualified borrowers.

Features of conventional loans include:

Minimum credit score of 620

Debt-to-income ratio up to 50%

3% to 5% down payment required

No household income limits or geographic restrictions on most loans

Ability to buy a 2-4 unit home

Often considered more desirable to sellers when making an offer

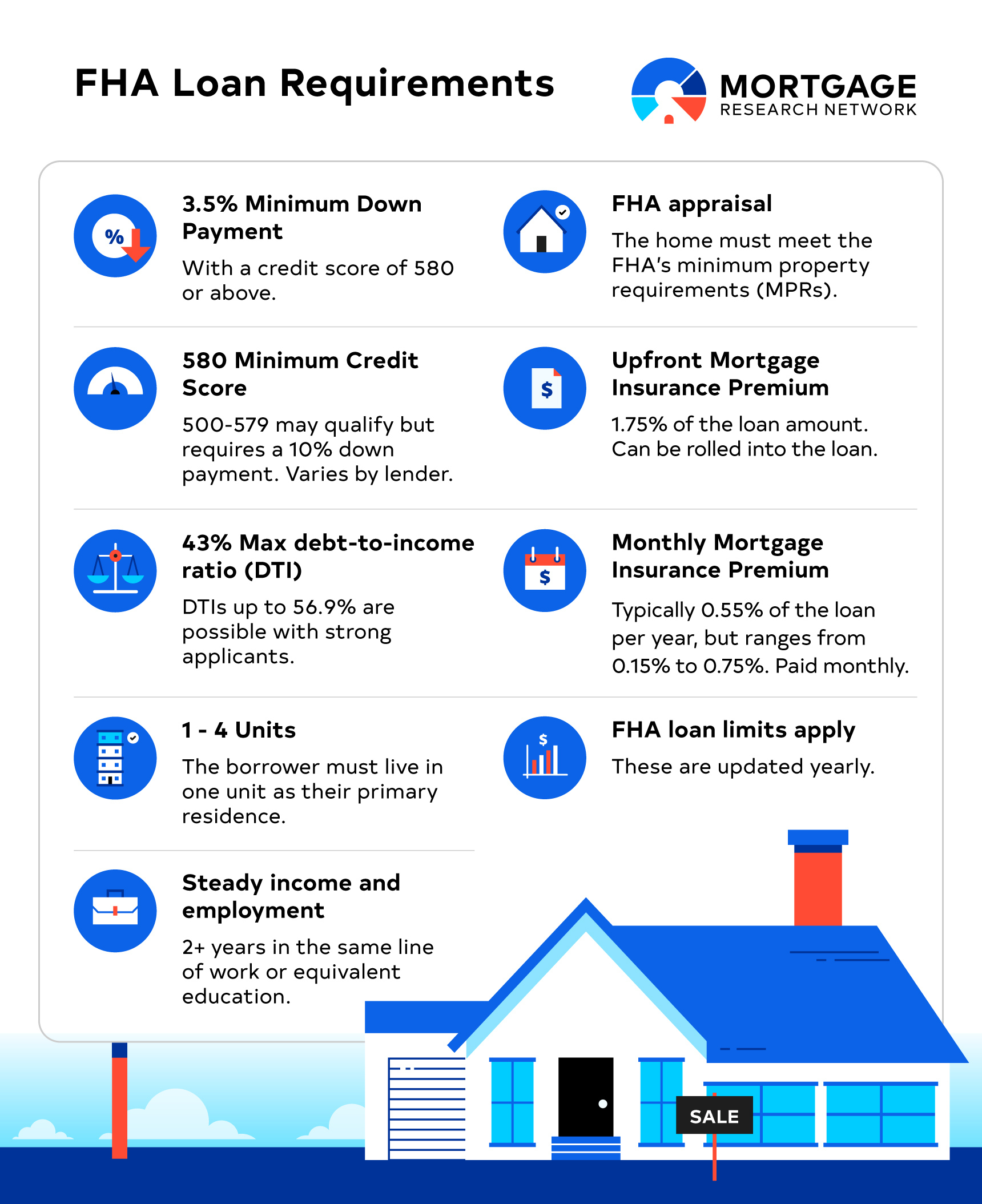

FHA Loans

FHA loans are another type of government-backed mortgage insured by the Federal Housing Administration. Qualifying for a loan through the FHA is typically easier than with the USDA, although the program does require you to make a small down payment.

FHA loan requirements include:

Minimum credit score of 580

Debt-to-income ratio up to 56.9% for top-tier borrowers

3.5% down payment required

No household income limits or geographic restrictions

Multifamily properties allowed with no increased down payment

VA Loans

VA loans are government-backed mortgages insured by the US Department of Veterans Affairs. They're only available to active-duty servicemembers, veterans, and some surviving spouses but are widely considered one of the best mortgage options for borrowers who qualify.

Features of VA loans include:

No minimum required credit score (similar to USDA loans)

No fixed maximum debt-to-income ratio

Zero down payment required (similar to USDA loans)

No income limits or geographic restrictions

No restrictions on owner-occupied multifamily properties

No required mortgage insurance or ongoing annual fee

Applying for USDA Loan Pre-Approval

USDA loan pre-approval is an essential first step in obtaining a mortgage through the USDA's Single Family Housing program. By getting pre-approved, you can gain a solid idea of what priced property you can afford and be able to make a competitive offer that shows sellers you're serious about purchasing their home.

If you're ready to start the pre-approval process, apply with a USDA-affiliated lender for a personalized loan estimate.