Suddenly, Refinancing May Be An Option For Post-2022 Homebuyers

Anyone who bought a home after September 2022 might be “in the money” to refinance, new data shows.

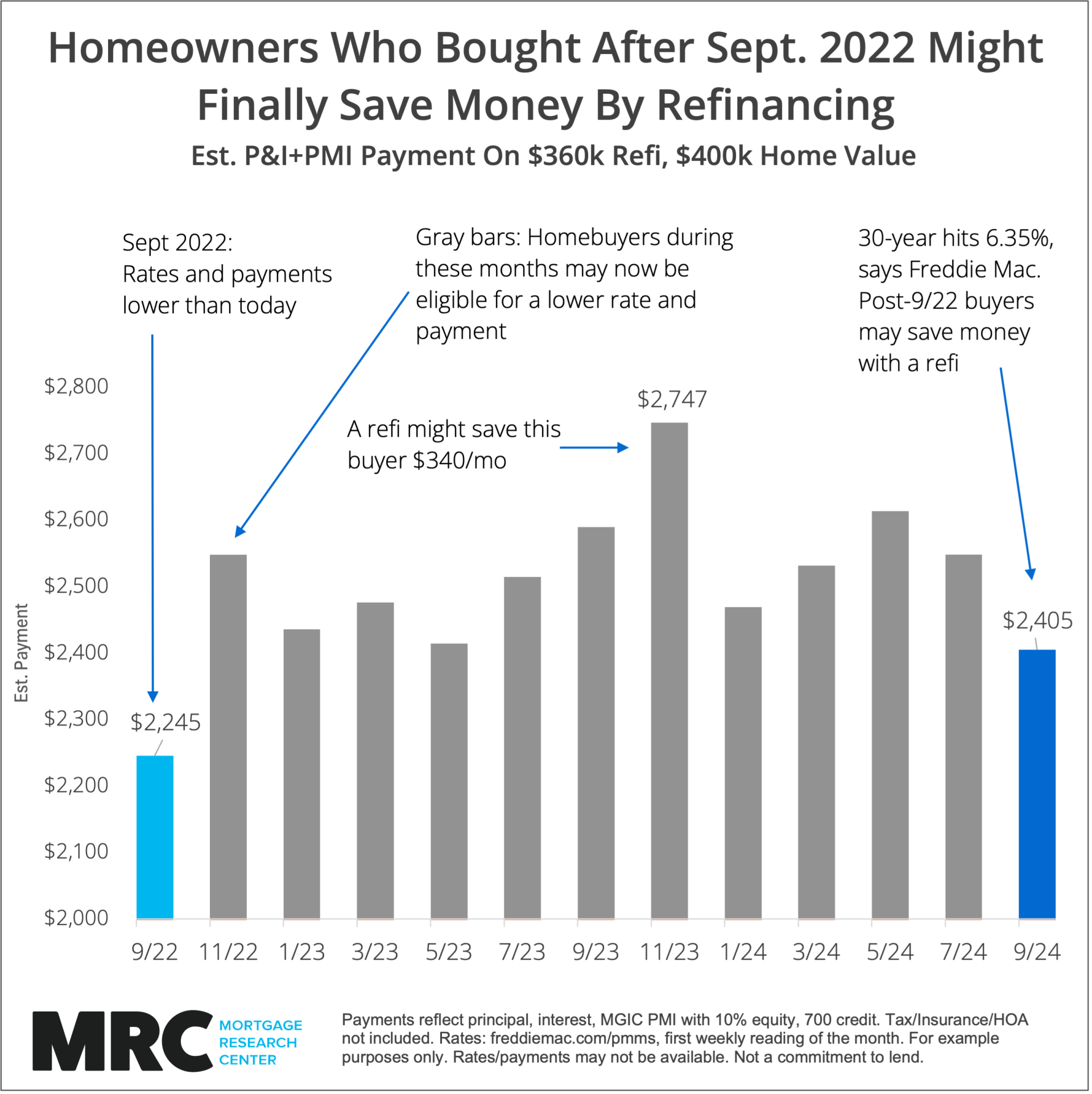

Freddie Mac, which has tracked mortgage rates since 1971, just published its weekly 30-year fixed average rate on September 5. It came in at just 6.35%.

This could mean homebuyers who bought a home since late-2022 might finally be eligible to save money on their mortgage each month. Mortgage rates are now lower than they have been for most of the past two years.

If someone purchased a home in November 2023, for example, they might have a rate near 7.76%, the average Freddie Mac reported that month. Refinancing to 6.35% could save them around $340 per month on a $360,000 mortgage.

While 6.35% might not seem low to those who have been watching rates since 2020, it’s significantly better than rates captured by most mortgage shoppers since 2022.

What Does a Refinance Do?

Those who are new to homeownership probably haven’t thought much about how refinancing works. Rates haven’t been low enough to look into it yet. Until now.

A refinance replaces your current mortgage with a new one with better terms.

People typically refinance because rates improved since they purchased the home. There are other reasons to refinance, like exchanging a 30-year mortgage for a 15-year one, turning home equity into cash, eliminating mortgage insurance, or changing an FHA loan to conventional. Still, dropping the homeowner’s rate and payment is the most popular purpose.

Refinancing is similar to getting a new loan to buy a home. But it eliminates steps like dealing with the seller and being on a tight timeline. Refinancing homeowners may also be asked for less documentation. In fact, some refinance types waive the appraisal and income documentation requirement entirely.

Still, refinancing is exchanging your old mortgage for a new one, potentially dropping your rate and payment and freeing up room in your budget.

Will Rates Drop Further?

Though rates are comparatively low right now, rates could continue to drop. The downward drift tempts homeowners into serial refinancing. Multiple refinances may not be wise.

Should homeowners take advantage of current low rates or wait it out?

Economists believe the U.S. economy could be near the end of an expansion cycle. What happens then? The economy and inflation soften, as they are starting to do now according to Forbes.

The Federal Reserve is expected to cut its key interest rate on September 18. While this is already factored into today’s rates, there’s a good chance of more aggressive cutting in late 2024.

“The markets still have at least 100 basis points (1%) of cuts priced in for this year,” says Afifa Saburi, Capital Markets Analyst at Veterans United Home Loans, “which means that they’re betting on the Fed to cut by 50 basis points either in November or December.” (Mortgage Research Center is Veterans United's parent company.)

Interest rates could continue to drift downward for years. Or, they could grind on in the low- to mid-6s. Few expect mortgage rates to rise.

Currently, it might pay to be patient. There’s more downside than upside to rates, and homeowners shouldn't refinance more often than they have to.

Refinancing comes with closing costs, up to 2-5% of the loan amount.

The refinancing homeowner can typically roll these costs into the new loan. But this removes some equity from the property. They also pay interest on these costs for as long as they have the new loan.

A refinance also extends the loan term, effectively making a 30-year loan a 32-year loan, for example, if the refinance occurs two years into the current mortgage.

Some homeowners need instant relief from high payments, though. For them, it could be very wise to refinance. Cutting monthly outflow in the short term could be more important than long-term savings.