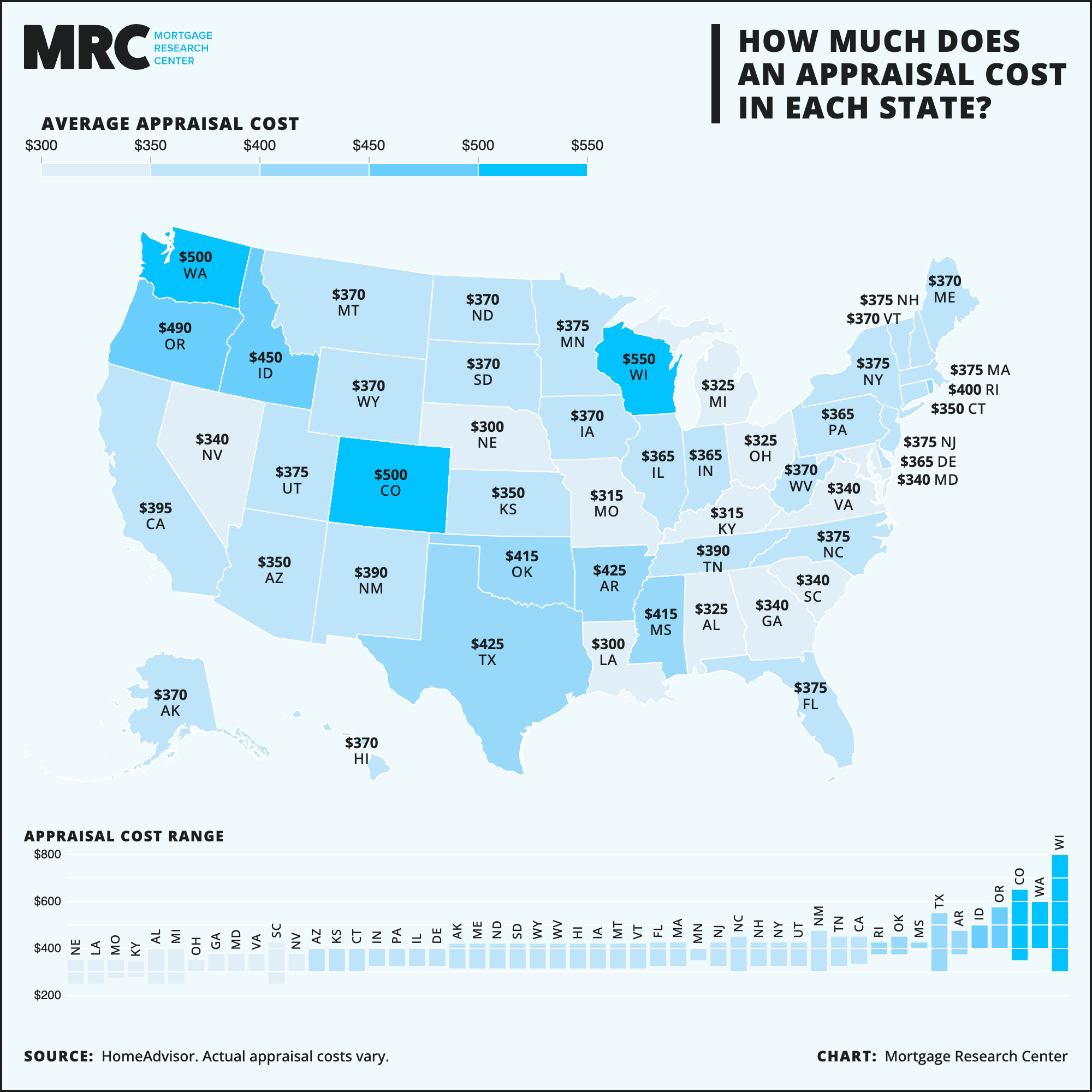

Low Appraisal? Request a Reconsideration of Value (ROV)

")

A reconsideration of value (ROV) is a way to dispute the accuracy of a home appraisal. With solid data, the appraiser might update their original valuation.

If you’re unsatisfied with the results of a home appraisal, you may have recourse: a reconsideration of value, or ROV, can result in the appraiser updating their report to provide a more accurate property valuation.

Understanding ROV Appraisals

If you recently had an appraisal completed, whether because you’re trying to purchase a home or refinance one you already own, and the value came in low, you may be able to request an ROV.

An ROV is the process through which your lender can ask the appraiser to reassess their conclusion by pointing out the use of erroneous data, providing more appropriate comparable sales, or highlighting apparent bias that influenced the price estimate.

Why Request an ROV?

Having an appraisal come in low can throw a wrench in the lending process. What are some of the biggest downsides that can result from undervaluation?

If you’re buying a home, you may be approved for a smaller loan than you planned on and need to come up with additional funds to complete your purchase or refi

Your loan-to-value ratio will be larger, which often translates to higher interest rates

You may not be able to tap into as much equity as you planned if you’re applying for a cash-out refinance

With a reconsideration of value, you can obtain a more accurate valuation, avoid these issues, and potentially save a purchase or refinance that otherwise could have fallen through.

“Many homeowners think they have no control over the process, but an ROV provides an opportunity to correct errors and ensure the appraisal reflects the property's real market value,” says Betsy Pepine, broker and owner of Pepine Realty.

Many homeowners think they have no control over the process, but an ROV provides an opportunity to correct errors and ensure the appraisal reflects the property's real market value.

What Is the Success Rate of an ROV?

In practice, reconsiderations of value are rejected far more frequently than they are approved. According to corporate relocation firm Dwellworks, only around 24% of ROV requests result in a modified appraisal.

Why are so few reconsiderations of value successful? An ROV can be denied for a variety of reasons, including:

Insufficient evidence to prove that the appraiser made an error

A third-party review could agree that the original appraisal is correct

Appraisers don't like ROVs because they call into question the accuracy of their work, and approving a request forces them to admit an oversight

However, if you're confident that the value provided in an appraisal is incorrect and have proof to back up the claim, talk with your lender about submitting a request for reconsideration.

There's always a chance – especially with well-documented evidence – and even if your request is denied, you're unlikely to be any worse off than with the current price estimate.

When You Should Request an ROV

You can’t request an ROV simply based on a gut feeling that the value estimate should be higher. You'll need evidence supporting your claim, which can come in several forms. Here are some examples of when you should ask your lender about submitting a reconsideration of value.

You Suspect Errors

Factual errors, such as missing information, mathematical mistakes, or the use of incorrect data, can often result in an inaccurate valuation.

Some of the most common appraisal errors include:

Incorrect number of bedrooms or bathrooms

Wrong age of the home

Inaccurate square footage

Features such as garages, pools, patios, or decks not being accounted for

Property condition ratings lower than they should be

Quality of construction ratings not appropriate for the materials and workmanship present

“When one of our renovated properties was undervalued last summer, we successfully appealed by showing detailed documentation of $45,000 in improvements that weren't reflected in the initial appraisal,” states Sean Grabow, owner of Central City Solutions, an Ohio-based real estate investment group.

When one of our renovated properties was undervalued last summer, we successfully appealed by showing detailed documentation of $45,000 in improvements that weren't reflected in the initial appraisal.

How Does Requesting an ROV Work?

How, precisely, does the process of requesting an ROV work? Here are the steps of a reconsideration of value from beginning to end.

1. Identify the Issues

In most cases, if you suspect an error with an appraisal's valuation, you will want to comb through the appraisal report and identify the issues yourself. Your lender will likely review the appraisal for any fundamental errors, but ROV requests are typically initiated by the borrower.

2. Gather Documentation

Reconsideration requests should always be accompanied by factual evidence. This involves providing documentation of errors made or more accurate sales data that should have been used.

If you’re working with a real estate agent, they may be able to help you verify information about the property and find more relevant comparable sales.

“The request should be clear, professional, and backed by data. Instead of simply arguing that the value feels too low, showing why it is incorrect with concrete examples makes a much stronger case,” says Justin Landis, founder of the Justin Landis Group of real estate professionals.

3. Approach Your Lender

Once you have hard proof that shows why the appraiser's valuation may be incorrect, submit it to your lender and ask that they request an ROV. Your loan officer will review your provided information and decide whether submitting for a reconsideration is the right choice.

4. Submit the Request

If your lender believes that an error was made, they will formally submit a reconsideration of value request to the appraisal management company, which acts as a middleman between lenders and the appraisers who conduct the appraisals.

5. Appraiser Review

Once the appraiser has received an ROV request, they will read through the evidence provided and determine whether an alteration to their original valuation is warranted.

6. Final Decision

Depending on the amount of work required, receiving a final decision – which will come as an update to the appraisal report – may take as long as two weeks. However, appraisers can often complete simple requests within a few days.

This update will be sent to your lender, who will then share the appraiser's final decision with you, the borrower.

What to Do If Your ROV Is Denied

Lending guidelines generally only allow for one reconsideration of value per appraisal. If the appraiser decides an update is not warranted – or does not update the value to the amount you were hoping for – you are unlikely to be able to request another ROV.

If your ROV is unsuccessful, you can ask your lender to order an entirely new appraisal. Be aware, though, that not all lenders will be willing to do so, and even when they are, you will be on the hook for paying the second appraisal fee.

This may not be an option with all loan types – appraisal values often "stick to" properties for a set period when applying for government-backed mortgages. However, FHA guidelines allow agency-affiliated lenders to request a second appraisal if they feel that the original is materially deficient and the appraiser is unwilling to correct the deficiencies.

Alternatives to an ROV

If a reconsideration of value is not an option – such as when you can't provide conclusive evidence why the appraiser should review their estimate – what other alternatives do you have?

In this situation, you may want to try:

Negotiating with the seller for a lower purchase price that reflects the appraised value estimate

Ask your lender to order a second appraisal

Consult a different lender, depending on your loan type (appraisal values generally stick with FHA-backed mortgages for 180 days)

Make a larger down payment on your purchase loan

Accept a lower valuation on your refinance

Pros and Cons of Requesting an ROV

A reconsideration of value can help you obtain a mortgage when an appraisal comes in lower than you were planning. However, requesting one isn’t without its downsides. Here are some of the pros and cons to consider.

Pros

An ROV can lead to a more accurate valuation and prevent issues with obtaining a loan

Providing factual evidence of errors can significantly improve your chances of success

A successful reconsideration lets you avoid paying for the costs of a second appraisal

Cons

Most ROV requests are denied, with less than a quarter of reconsiderations being approved

Waiting for an updated appraisal can delay the underwriting process and potentially prevent you from closing on time

You can typically only submit one ROV, meaning you have to identify and document all issues with your initial request

Should You Request a Reconsideration of Value?

Reconsiderations of value are not always successful. However, if you have documented evidence of errors, inappropriate data, or bias in your appraisal report, it's worth asking your lender to request an ROV.

Instead of submitting an ROV request, you may also ask your lender to order an entirely new appraisal. If this isn't possible, consider applying with a different lender who may still be able to get your loan approved.