What's The Real Deal on Down Payments: How Much Do I Need to Buy a House?

Some loan programs offer a zero down payment option. But more than likely, you'll need at least 3% down.

You’re excited about the prospect of purchasing a home. Only you’ve heard that you may need to put more money down than you expected. Confused and concerned, you ask yourself: How much of a down payment do I need for a house?

Some loans require making at least a 20% down payment, although other forms of home financing can be had for much less—even zero money down. Your down payment will depend on the loan program you choose, and other factors.

Key Takeaways

A down payment is your portion of the home’s purchase price you are fronting. The rest is covered by the lender

While a 20% down payment is a traditional benchmark offering benefits like lower monthly payments, no PMI, and better loan terms, many loan programs accept smaller percentages or even zero down payments for eligible borrowers

Saving for a down payment requires disciplined strategies like automating savings, increasing earnings, cutting expenses, and leveraging assistance programs

What is a Down Payment and Why Is It Needed?

A down payment is the cash you need to pay at closing toward the purchase price of a home. It’s expressed as a percentage of the total home price, such as 5% or 10%. Your down payment shows that you are financially invested and decreases a mortgage lender’s risk. That’s because the more you pay upfront, the less you need to borrow and the more equity you immediately earn. If you put down 20% for example, your equity position is 20%.

“Think of it as your ‘skin in the game’– a way to prove you are serious about homeownership,” explains Andrew Latham, a certified financial professional and mortgage expert at SuperMoney.com.

The down payment also factors into determining your loan-to-value (LTV) ratio, which is a key number lenders examine to evaluate loan risk. Your LTV is calculated by dividing the loan amount by the home’s appraised value. The higher the LTV ratio, the higher the risk for the lender. Making a larger down payment lowers the LTV ratio and decreases the lender’s risk. For instance, if you purchase a $300,000 house with a $60,000 down payment (20%), your loan amount is $240,000 and your LTV is 80%.

Some lenders and loan programs mandate at least a 20% down payment, while others require less, such as 10%, 5%, or 3%. Two government-backed loan programs actually offer zero-down mortgage loans.

What’s the Deal with a 20% Down Payment?

Lenders traditionally prefer no less than a 20% down payment because it significantly lowers their risk.

“By contributing 20% minimum, borrowers have more equity in the property, thereby reducing the likelihood of default,” notes Steven Kibbel, a certified financial planner and senior editor at InternationalMoneyTransfer.com. “Historically, 20% is the metric that has been considered a safe threshold that balances borrower commitment and lender security. The 20% standard evolved over time through industry practices and risk assessments, becoming a widely accepted norm.”

David Milo, a mortgage lender with Independent Lending, says the 20% rule has been a trend ever since the Great Depression.

“With at least a 20% equity position, it’s safe to assume that the borrower is not going to abandon their home anytime soon,” adds Milo.

Additionally, says Carl Holman with A&D Mortgage, “properties with higher equity are more likely to retain value during market downturns, further protecting the lender’s investment.”

This 20% benchmark also removes the need for the borrower to pay for private mortgage insurance (PMI). PMI safeguards the lender if the borrower defaults but is unnecessary when the LTV is 80% or lower.

As mentioned, however, not every lender or loan program obligates putting at least 20% down, as we’ll cover soon.

Benefits of 20% Down

Making at least a 20% down payment provides several advantages to borrowers. These include:

Lower monthly payments. “By reducing your loan amount, the borrower saves on both principal and interest payments,” says Holman. “For example, on a $300,000 home with a 7% fixed interest rate, putting 20% down – $60,000 – instead of 10% down, which would be $30,000, reduces the loan amount from $270,000 to $240,000. Over 30 years, this could save thousands in interest.”

No PMI. Keep in mind that PMI often costs 0.5% to 1% of your loan amount every year. On a $240,000 loan, bypassing PMI could save $1,200 to $2,400 annually.

Improved equity position. “With a 20% down payment, borrowers began with immediate equity in their home. This can provide financial security and options for refinancing or borrowing later,” continues Holman.

Improved loan terms. Your lender may offer a lower interest rate if you pledge a higher down payment, potentially saving thousands over the loan’s life, per Kibbel.

Better home options. Being able to put 20% down minimum may help you qualify for a larger loan that can enable you to buy a more coveted, expensive home.

Cons of 20% Down

On the other hand, forking over 20% or more may not be the right move for you. Let’s examine a few of the downsides.

Higher upfront cost. Salting away $60,000 to make a 20% down payment on a $300,000 home can be difficult, particularly in high-cost areas. “This large financial commitment could deplete your savings, leaving little room for emergencies or other investments,” warns Holman.

Missed opportunities. Home prices could increase faster than your ability to save for that higher down payment. The time it takes you to sufficiently pad your savings could result in losing out on possible homes for sale you might have been interested in. “Or, you could lose out on investing that cash instead into unsecured accounts like retirement plans or other secured assets that yield higher returns than home equity growth, assuming you were okay with delaying your home-buying dream,” says Milo.

Market risks. If it takes a long time to save up at least 20%, home prices and interest rates may rise more rapidly than expected during that period, making homeownership less affordable.

How Much Down Payment Do You Really Need?

Again, just because 20% down is the standard benchmark lenders prefer doesn’t mean it’s a requirement. Here’s a breakdown of the minimum down payment needed based on different loan options.

Conventional mortgage loans. Standard conventional loans require at least 20% to avoid PMI but can be had with PMI attached for as little as 3% (for qualified first-time buyers using the HomeReady or Home Possible program) to 5%.

FHA home loans. You’ll need at least 3.5% down if you have a credit score of 580 or higher, and at least 10% down with a credit score of 500 to 579.

USDA home loan. No down payment is necessary if you qualify, but the property must be located in a USDA-eligible rural area.

VA home loan. No down payment is required for qualified veterans, active-duty service members, or surviving spouses.

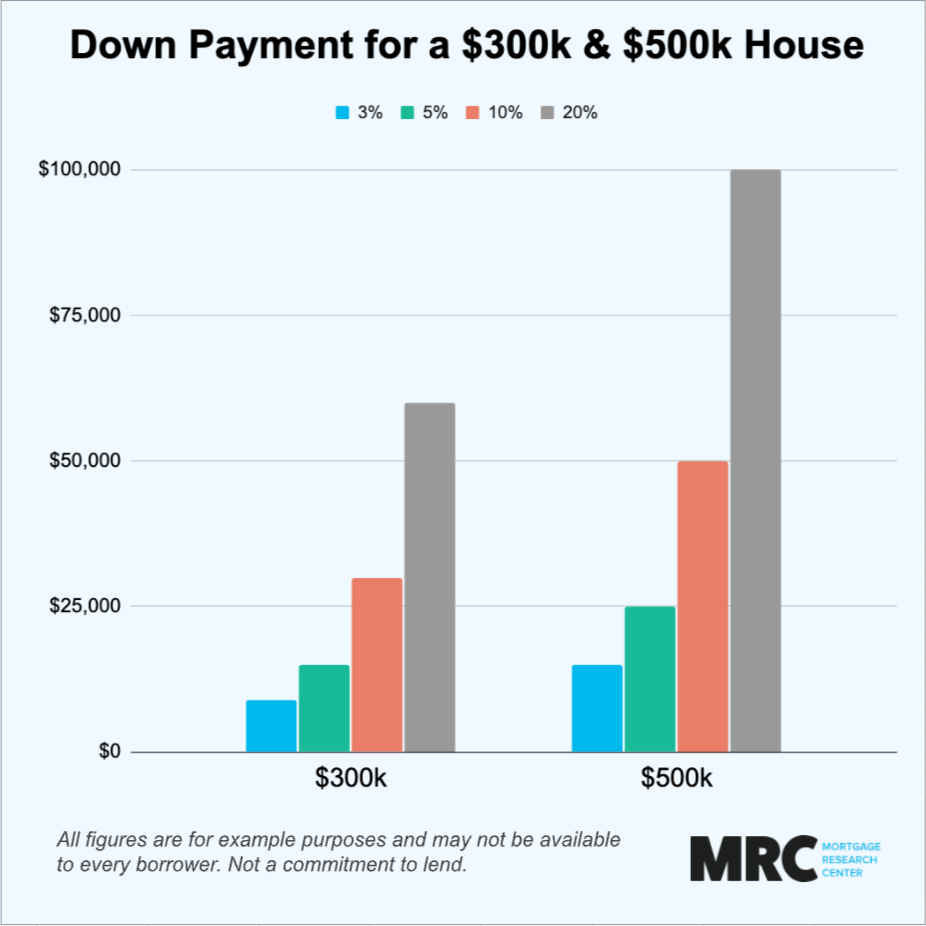

Wondering how much down payment for a 300k house is required? Curious how much down payment for a 500k house is needed? Here’s the down payment amount you’ll need for these two purchasing scenarios:

| % down | $ down for a $300,000 home | $ down for a $500,000 home |

|---|---|---|

| 3% | $9,000 | $15,000 |

| 5% | $15,000 | $25,000 |

| 10% | $30,000 | $50,000 |

| 20% | $60,000 | $100,000 |

Best Tips on Saving For A Down Payment

Unless you qualify for a zero-down loan like the USDA or VA mortgage, you’re going to need to save plenty for a down payment amount between 3% and 20%. Doing so may not be easy, especially if you aim to avoid PMI with a full 20% down. But getting to your savings goal is doable with the right plan.

Automate savings. “For consistent progress, set up automatic transfers into a separate financial account dedicated solely to saving for a home,” recommends Kibbel. Consider a high-yield CD or savings account or even a low-risk investment option to grow your funds more quickly.

Increase earnings. Accept freelance work, start a side hustle, get a second job, or ask for a raise. However, don’t plan on being able to use this income to qualify.

Cut expenses. Scrutinize your discretionary spending and eliminate unnecessary items like dining out and subscriptions.

Use windfalls. “Direct tax refunds, work bonuses, and gifts toward your down payment fund,” Kibbel adds.

Check out assistance programs. Explore state and local programs that provide down payment grants or forgivable loans. “Also, take advantage of any employer-provided assistance program in place that can help with the down payment,” advises Milo.

Additionally, avoid common mistakes that prospective borrowers make, which can hurt your chances of affording a house.

“Remember to budget for additional homebuying costs like closing fees, inspections, and moving expenses,” suggests Latham. “Also, be careful not to rely on volatile investments in the hope for quick gains – only to lose savings when the market dips.”

Beware of waiting too long to pull the trigger on a purchase, as well.

“Trying to save the perfect amount could delay your purchase and result in higher prices or interest rates. Evaluate whether a smaller down payment with PMI attached might be a smarter move sooner based on your market and financial situation,” says Holman.

Don’t over-prioritize saving for a down payment at the expense of contributing to crucial emergency funds or retirement contributions, either.

“To avoid these pitfalls, maintain a balanced financial plan, use stable, proven savings options, and research total homebuying costs early in the process,” Latham continues.

Your next steps

The down payment amount is an essential metric that sets the tone for the entire borrowing and buying process. Putting down at least 20% is ideal in most situations, but if you can’t save that much remember that other financing options exist that require little to no down payment, assuming you qualify. The important thing is to begin saving responsibly and early in the process and research different loan options based on your personal finances and goals.

Above all, don’t feel intimidated by the 20% down recommendation: There are ways to accomplish your dream of homeownership with a lesser amount saved, although it may involve some trade-offs.