When Do You Start Paying Taxes on New Construction?

Property taxes on new construction homes are often based on the land value only, but after completion they are reassessed to include the structure. Your lender may collect estimated taxes right away through escrow to cover the upcoming tax obligations.

Got your eyes on a new construction home you want to purchase? Freshly built residences offer peace of mind knowing that all the materials, components, and systems are brand new. But you may have some lingering doubts about property taxes.

That begs an important question: When do you start paying taxes on a new construction home?

When Do You Start Paying Taxes on New Construction?

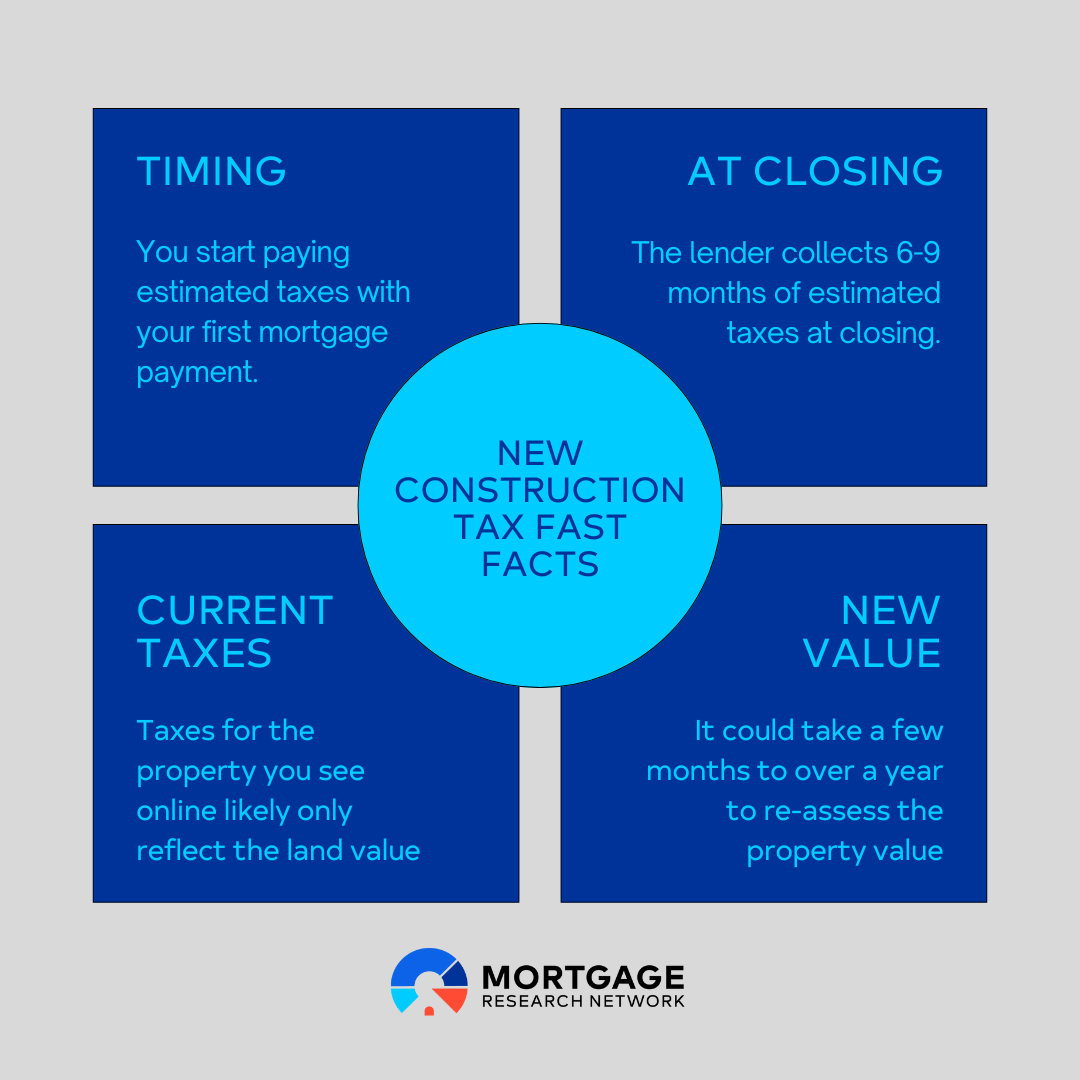

You start paying estimated taxes on new construction at closing. (The lender typically collects three to nine months of property taxes at closing for any home.) Then, you continue paying an estimated amount with your first mortgage payment. But you won’t know your exact tax bill until later.

“Property taxes on a new construction home typically commence once the property is assessed by the local tax authority,” explains attorney Christopher Migliaccio, founder of Warren and Migliaccio LLC. “This assessment occurs after the construction is completed and a certificate of occupancy is issued. However, the exact timing can vary depending on local regulations and the efficiency of the assessment process.”

New construction property taxes technically begin accumulating the day you take ownership of the property. However, you may not know how much taxes will be in the long run.

Initially, taxes are based on the value of the land only. But, once your home is completed and reassessed, your tax bill will reflect the full property value, including the land and structure. This could mean quite a jump from property taxes you see online for the home.

How Long Before I Know My True Tax Bill and What If I Overpay?

The reassessment period for new construction homes will vary by jurisdiction, spanning from a few months to over a year. Over this time, your lender will estimate property taxes based on comparable properties in the area and collect these estimated amounts via escrow as part of your monthly mortgage payment.

After the actual assessment is determined by your jurisdiction, your monthly mortgage payment may adjust to reflect the accurate tax obligation.

“If your lender estimates lower taxes than expected, your mortgage payments could be artificially low in the first few months but rise significantly once the assessment is finalized,” cautions Realtor Eli Pasternak, founder/CEO of Liberty House Buying Group.

Related: Should You Get a Home Inspection on New Construction?

If your lender estimates lower taxes than expected, your mortgage payments could be artificially low in the first few months but rise significantly once the assessment is finalized

If you overpay property taxes before the reassessment, you might receive a refund or have the excess applied as a credit toward future payments, depending on your jurisdiction's policies. Some local governments automatically roll the overpayment into the next tax cycle, while others allow you to request an adjustment if your property is later reassessed at a lower value.

On the other hand, if you underpay you could face penalties, interest, or even a delinquency notice, requiring you to settle the difference once the reassessment is complete. However, if the reassessment results in a lower tax obligation, you may only need to pay the adjusted amount.

If you’ve set up escrow to pay your property taxes and homeowners insurance, you will start paying taxes with your first mortgage payment.

“These funds aggregate in your escrow account and are dispersed on your behalf when the next tax bill is due,” Matt Schwartz, founding partner of VA Loan Network, notes. “The date your taxes are due every year will depend on the state your property is in. Whether yours is a new construction home or a pre-existing residence will not change the date when your tax bill is due.”

How Much Might My Property Taxes Rise?

Your new construction property taxes may spike after the assessment, depending on the property’s assessed value, its size, location, and features, local tax rates, current market circumstances, and any applicable exemptions.

“It’s not uncommon for property taxes to rise significantly after a new assessment especially if the initial estimates were conservative,” Migliaccio continues.

Martin Orefice, CEO of Rent To Own Labs, recommends bracing yourself for a higher bill than you might think post-assessment.

“Because pre-construction property taxes are based solely on the value of the land, your taxes will likely go up considerably after assessment. Just from a land value perspective, you may be looking at more than tripling that value even with a fairly modest home,” he says.

Let’s say you purchase a newly built home for $400,000; initially, your property taxes will be based on the land's value alone, which, in this example is $60,000. Assuming your tax rate is 2%, your initial annual tax bill would be $1,200 ($60,000 × 2%). However, once your home is reassessed to include the completed structure, its total value would rise to $400,000, and your new tax bill would increase to $8,000 ($400,000 × 2%) for the year, reflecting the full value of both the land and the home.

However, if your lender set up your escrow account properly ahead of time based on “improved value” (the property’s expected value after construction is completed) your increase could be moderate – within a 5% to 10% higher range, per Schwartz.

“It’s when your escrow account is set up based on unimproved value that you can face a major increase in your property taxes after the house is assessed based on improved value. Property taxes are handled at the local level, so be sure to consult with your lender or title company on when your jurisdiction assesses properties,” Schwartz continues.

Consider that property taxes are typically used to finance local government operations, including roads, schools, and fire and police services.

“The more services your local jurisdiction offers and the smaller the tax base is, the higher your property tax bill will probably be,” says Orefice.

How Much in Taxes Does the Lender Collect at Closing with New Construction?

At closing, your lender will likely collect an initial escrow deposit to cover upcoming property tax obligations. This often equates to three to nine months' worth of property taxes to properly fund the escrow account.

“For new construction, this amount is often based on estimated taxes derived from comparable properties or projected assessments, considering the home’s anticipated value in prevailing tax rates.”

Rest assured that your lender will collect enough escrow funds from you at closing to ensure you have sufficient dollars to pay your taxes.

“For instance, if your property taxes are due in December and you close in July, your lender is going to collect seven months of taxes, plus two months of taxes to account for the fact that you’re not going to have a first mortgage payment due, in this example, until September 1 – which is at least 30 days after you close,” says Schwartz.

What’s next?

It’s smart to have a discussion about your expected property taxes with your real estate agent and mortgage loan officer. The experts recommend asking the following questions:

How are property tax estimates for my new construction home calculated?

Will the estimated property tax funds I need to put into my escrow account, prior to assessment, be based on improved value or unimproved value?

What’s the process for adjusting my escrow payments after the actual tax assessment is available?

How often will my escrow account be reviewed and adjusted?

Are there any local property tax exemptions or abatements I qualify for?

If you have further property tax questions, consult with your local tax assessor’s office or your city or county treasurer’s office.