One Extra Mortgage Payment Per Year: How Overpaying Your Mortgage Works

Maybe, in the excitement of closing on your new home, the numbers dissolved into a blur. But now, after making a few mortgage payments, you’ve started to notice how much interest you’re paying to the lender.

A $300,000 loan at 7 percent a year will pile up $418,527 in interest charges over the course of a 30-year term. That means for every $100 borrowed, you’d be paying back $239 — more than double the amount borrowed.

What’s more, during the first few years of a mortgage, almost all of your monthly payment goes toward interest. The principal balance — which is the amount you borrowed — hardly budges.

There’s a simple way to cut down on all this interest: pay extra towards your principal.

You may have heard the common advice to pay one extra mortgage payment per year because it can save you money in lifetime interest costs and cut back on the life of your loan (we’ve heard anywhere from seven to thirteen years).

So, is this advice true? And how does that work, exactly?

The Power of One (Extra Mortgage Payment)

To understand how overpaying on the mortgage works, let’s consider a specific example: the purchase of a $325,000 home.

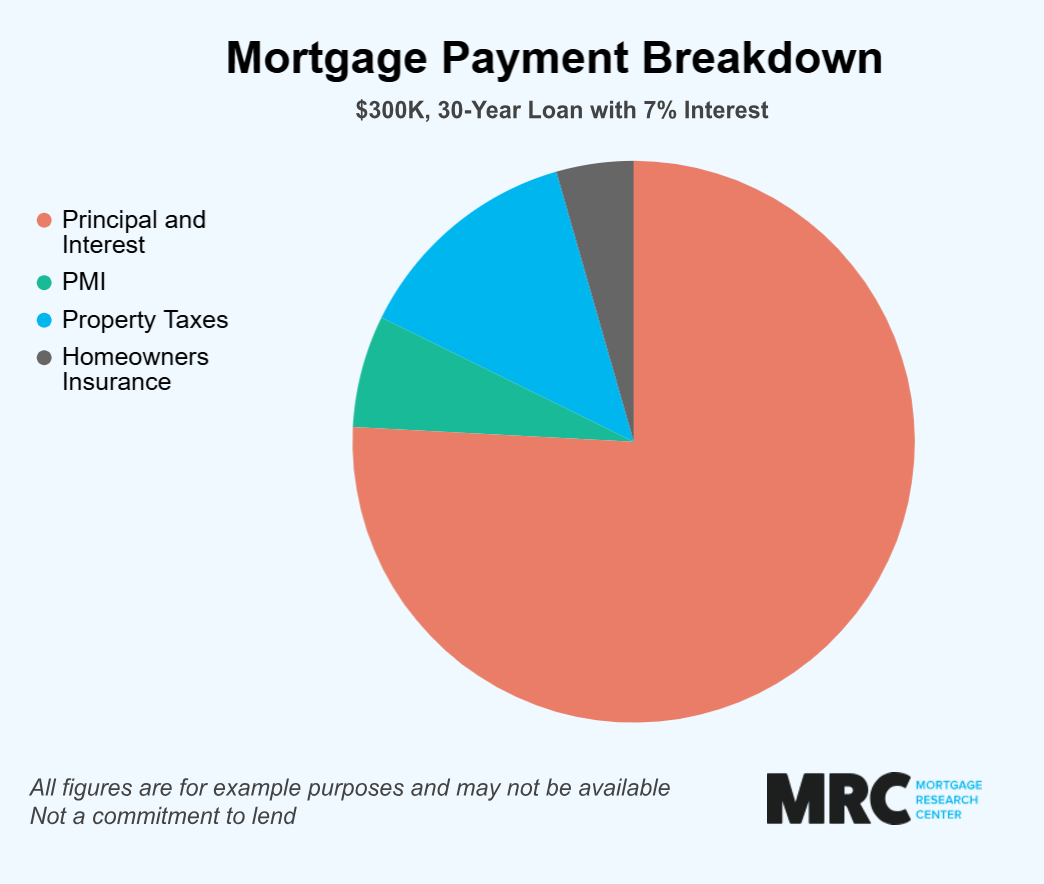

We’ll say you paid $25,000 down on the home, leaving $300,000 to be mortgaged. At 7 percent over 30 years, a $300,000 loan’s payment will be $2,635 a month.

This $2,635 monthly payment includes:

$1,996 for principal and interest

$170 for private mortgage insurance (PMI)

$349 toward annual property taxes

$117 toward annual homeowners insurance

$0 in HOA fees (this home is not part of an HOA)

Actual insurance premiums, taxes, and HOA fees will vary by borrower. These are just examples. But the principal and interest (PI) portion of the payment will almost always be the largest part of the payment. This part of the payment services the mortgage debt.

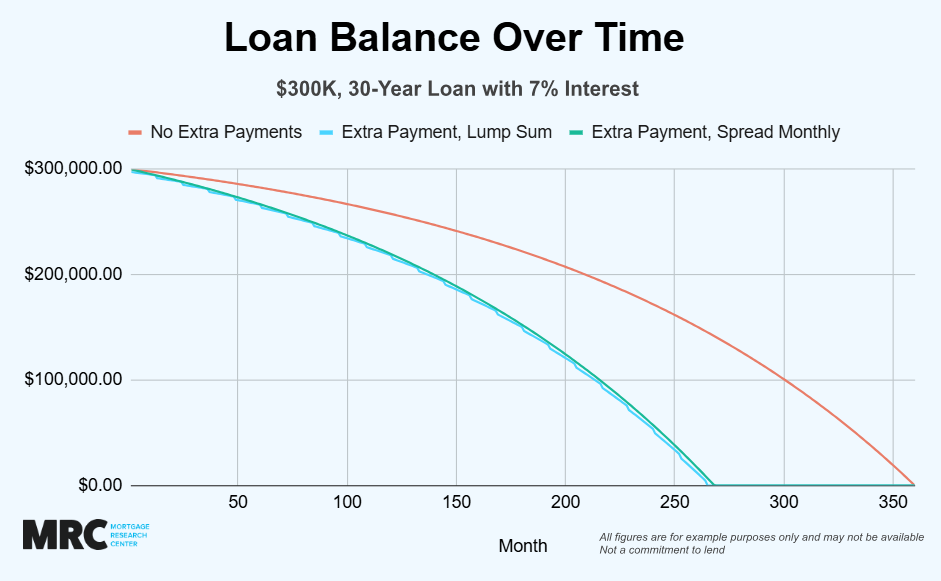

We ran three repayment scenarios:

Scenario 1: No extra payments are made

Scenario 2: An extra payment of $2,635 is made yearly in a lump sum payment at the beginning of the year

Scenario 3: An extra payment of $2,635 yearly, spread out over 12 months (just under $220 extra each month)

In summary, here’s what we found:

Paying an extra mortgage payment each year in this example can shave up to seven years and eleven months off your mortgage repayment and save you up to $128,759 in lifetime interest.

There was little difference between paying a lump sum at the beginning of the year and paying in smaller increments monthly. The lump sum scenario did, however, pay the mortgage off three months sooner and saved around $4,000 more in lifetime interest.

Let’s see how each of those scenarios plays out:

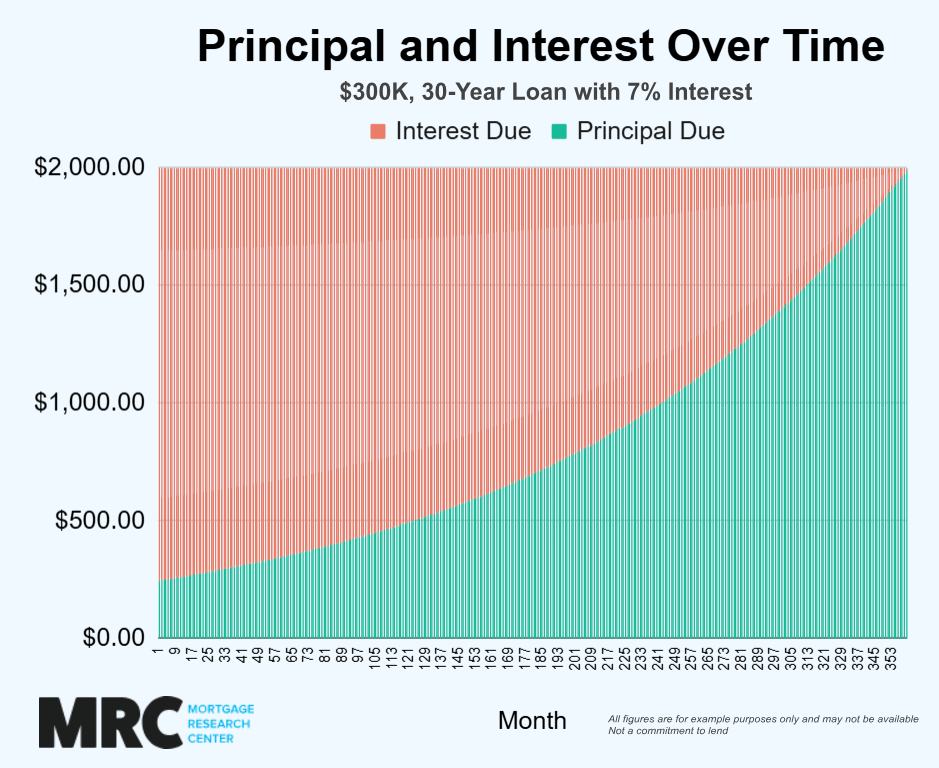

Scenario 1: Paying On Schedule with No Extra Payments

Since this is a fixed-rate loan, the principal and interest due each month stay the same ($1,996) for all 360 monthly payments. But how much of this $1,996 payment is principal and how much is interest? That answer changes each month based on the loan’s amortization schedule.

Assuming the borrower stays on schedule with the loan, here’s what happens:

On the loan’s first payment, only $246 of this $1,996 PI payment goes toward the principal; the other $1,750 pays interest

With every payment made on schedule, the principal portion of the payment increases by a few dollars, and the interest portion decreases by a few dollars to compensate. Payment 120, 10 years into the loan, sends $638 to the principal and $1,358 to the interest

With each passing payment, more of the payment goes to the loan’s principal. By the 360th and final payment, $1,984 of the $1,996 pays on principal; only $12 goes to interest

This table shows the incremental increase in money going onto principal:

Month | Principal Due | Interest Due |

1 | $246.00 | $1,750.00 |

2 | $247.43 | $1,748.57 |

3 | $248.88 | $1,747.12 |

4 | $250.33 | $1,745.67 |

5 | $251.79 | $1,744.21 |

6 | $253.26 | $1,742.74 |

7 | $254.74 | $1,741.26 |

8 | $256.22 | $1,739.78 |

9 | $257.72 | $1,738.28 |

10 | $259.22 | $1,736.78 |

*All figures are for example purposes only

On this schedule, all of the interest payments add up to $418,527; all of the principal payments add up to $300,000.

So, in total, this repayment schedule for a $300,000 loan at 7 percent requires $718,527 in principal and interest.

Scenario 2: Paying an Extra Lump Sum Payment Each Year

Making extra payments, in addition to the monthly payments required by the amortization schedule we just described, can do two things:

All of the extra payment goes directly onto the principal, speeding up the loan’s schedule. This gives the lender less time to charge interest

Since the entire payment goes onto the principal, the principal balance decreases faster, decreasing the interest charged and helping the homeowner earn more equity sooner

Here’s the effect of making one extra payment at the beginning of each year on our $300,000 loan:

The extra payments shave seven years and 11 months off the 30-year term, saving $128,759 in interest along the way. The home would be paid off in 22 years and one month instead of 30 years

After the first year, the mortgage balance would be about $294,400 instead of about $297,000, creating an extra $2,600 in equity

Saving $128,759 in interest probably got your attention. Compared to that, building an extra $2,600 in equity a year might not seem like much, but 10 years later, that $26,000 in extra payments actually translates to over $40,000 in additional equity, thanks to how the extra payments reduce interest and accelerate future principal paydown — and that’s without accounting for any home appreciation.

Scenario 3: Spreading One Extra Payment Throughout the Year

Not every homeowner can part with an extra payment all at once. It’s easier to break the extra payment down into installments. For our $300,000 loan example, spreading one $2,635 payment across 12 months would require paying just under $220 extra on the mortgage each month.

This $220 extra a month strategy also has a powerful effect:

The extra payment cuts seven years and eight months off the mortgage, saving $124,217 in interest

The extra payment still adds almost $2,600 a year in equity by lowering the loan balance faster

Most loan servicers make it easy to pay extra on principal each month. Many even have a “pay on principal” link set up for this. If you’re not sure whether your extra money is going onto the loan’s principal, be sure to ask. Otherwise, the extra money may be credited to the next month’s scheduled payment, lessening its impact.

This graphic shows the impact of each scenario: making no extra payments, paying a lump sum extra payment, and spreading the monthly payment across the year:

Why One Extra Payment is So Powerful: Principal and Interest Portions of Your Mortgage Payment

Some homeowners don’t believe it. Can one extra payment a year really save between $124,000 and $128,000? It sounds too good to be true.

This power of one extra payment makes more sense when you know how a 30-year amortization schedule works.

Like we described in Scenario 1 above, amortization splits each PI payment into principal and interest. In the first few years of the mortgage, almost all of the payment goes to interest; only a small fraction pays down the principal.

So even though you made your first $2,635 monthly payment, your $300,000 mortgage balance would go down by only $246. The next month’s $2,635 payment reduces the loan balance by another $247.

So far you’ve paid $5,270 but lowered your mortgage balance by $493. At this rate, it takes years to put a noticeable dent in the loan balance, as this graph shows:

The extra $2,635 payment each year bypasses this schedule. The entire $2,635 goes onto the loan’s principal, paying it down much faster and shortening the term length. To put that into perspective, it takes nearly eleven months of normal payments in the first year to pay down $2,635 worth of principal. So, by putting that amount straight towards the principal, you’re effectively making the equivalent of 11 monthly payments - just without the high interest costs of the early payments.

As time passes, the extra payments change the shape of the amortization curve above. The new curve cuts into the interest due, saving money.

Paying Extra Makes All Your Future Payments More Powerful

Then, this extra traction you’re generating by paying extra on principal gets amplified over time.

Banks charge interest as a percentage of the loan’s balance. A lower balance means less interest can be charged, even though the interest rate stays the same. Paying less interest allows more of the regular payment to be applied to the principal.

This is how the momentum really starts to build.

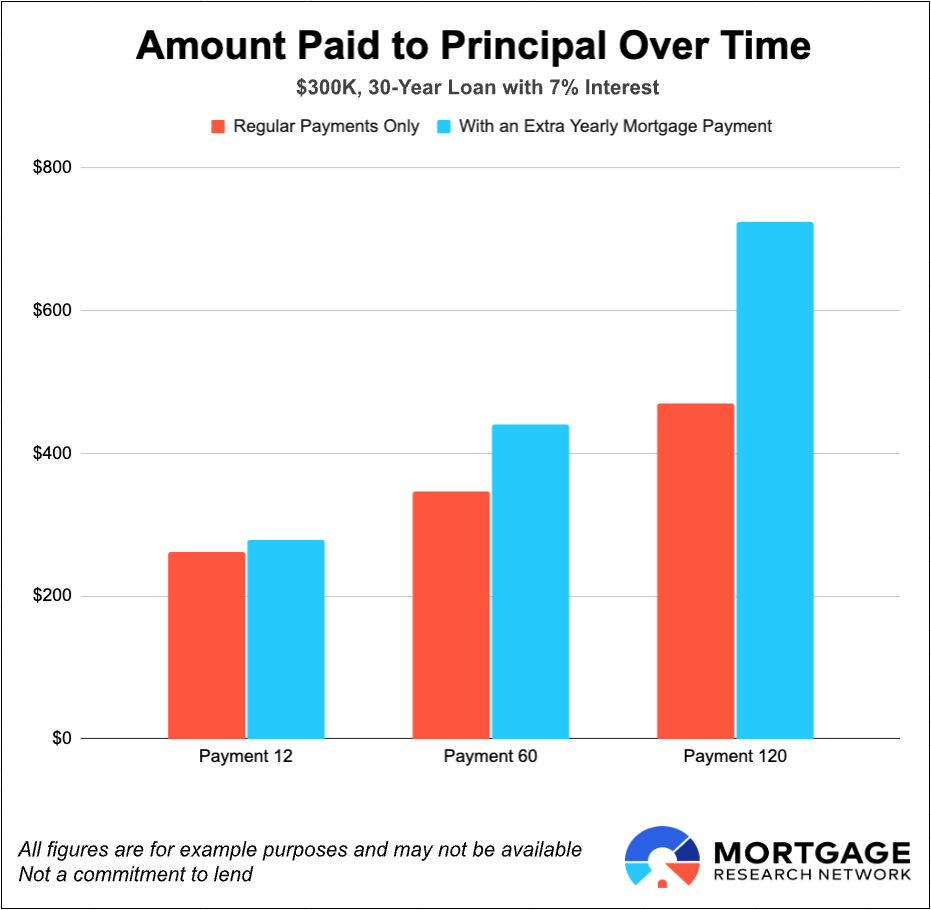

Let’s compare payments on our $300,000 loan at 7 percent interest:

Amount to principal on regular schedule | Amount to principal when making 1 extra payment at beginning of year | |

Payment 12 (end of year 1) | $262 of $1,996 to principal | $278 of $1,996 to principal |

Payment 60 (end of year 5) | $347 of $1,996 to principal | $440 of $1,996 to principal |

Payment 120 (end of year 10) | $469 of $1,996 to principal | $724 of $1,996 to principal |

*All figures are for example purposes only

The momentum continues to build over the next 10 years, between Payment 120 and Payment 240. By then, almost all of each payment will go onto principal — and the loan will almost be paid off about eight years early.

Should I Pay Extra on the Mortgage Yearly or Monthly?

In the table above, the borrower paid an extra payment at the beginning of each year. Not every homeowner can afford to pay two mortgage payments in one month, even if it happens just once a year.

It’s easier for many borrowers to split the extra monthly payment into 12 equal installments. For our $300,000 loan at 7 percent interest, this would mean paying an extra $220 a month directly onto the loan’s principal.

Which strategy is more powerful? Paying the one payment in a lump sum — but not by much.

The lump sum payment saves almost $128,759 over the life of the loan and pays off the home seven years and 11 months early (Scenario 1 above)

Splitting the extra payment into 12 installments saves $124,217 and pays off the loan seven years and eight months early (Scenario 2 above)

Yes, paying annually instead of monthly saves $4,500 more and pays off the loan three months earlier, but paying monthly is a close second. Both scenarios outpace the loan’s amortization schedule.

Interest is a Factor

Paying extra on the mortgage dampens the power of the loan’s interest rate to rack up huge long-term charges. But the loan’s interest rate still affects the bottom line, even when paying extra.

Since homeowners with higher interest rates pay more, they also have more potential to save by making an extra payment:

Interest rate | Interest saved with 1 extra payment spread out monthly | How early loan will be paid off |

4.0% | $44,895 | 5 years, 6 months early |

7.0% | $124,217 | 7 years, 8 months early |

9.0% | $207,070 | 9 years, 3 months early |

*All figures are for example purposes only

Of course, borrowers with higher interest rates pay higher monthly payments. This means the extra payment will require more out of pocket.

What About Making Two Extra Payments?

Making two extra payments per year, instead of one, cuts even deeper into a loan’s lifetime interest charges.

For our sample mortgage, the $300,000 loan at 7 percent, making two payments:

Cuts 11 years and 10 months off the term (compared to 7 years, 8 months for making one extra payment)

Saves $187,523 (compared to saving $124,217 with one extra payment)

In this example, we spread the two extra payments across all 12 months. On our sample loan ($300,000 at 7 percent) this would require paying $440 extra a month onto principal.

Biweekly Mortgage Payments Make Paying Extra Easier

Given a choice between…

Saving hundreds of thousands of dollars and owning our home sooner, or

Spending six figures more on interest and staying in debt longer

…most of us would choose option A. So why don’t more people pay extra on their mortgage payments to achieve this goal?

Many people can’t afford to pay more; others fail to get into the habit.

Paying biweekly on the mortgage can solve both of these problems. Biweekly means every other week. Here’s how to do it:

Take the loan’s monthly payment and split it in half

Make this half payment every other week

That’s all. Doing this creates an extra payment per year without really creating a budget crunch. Why? Because paying half the monthly payment every other week for 52 weeks creates 26 half payments (or 13 full payments). When you make 13 payments instead of 12, one of them is, of course, extra.

One note of caution: Make sure to submit both halves of the payment before the loan’s monthly due date to avoid late fees. Some lenders offer biweekly payment programs that automate this schedule and ensure timely payments.

Paying Extra vs. Shortening Your Loan Term

We’ve explored only 30-year fixed-rate loans, the most popular mortgage for American homeowners. A 30-year loan charges a lot more interest than a loan with a shorter term.

So, homeowners who want to save on interest could also refinance into a loan with a shorter term when they’re financially ready for this.

For example, a 15-year loan of $300,000 at 7 percent charges only $185,367 in interest over the 15-year term. The same loan amount at the same rate over 30 years charges $418,527.

However, the 15-year loan’s monthly payment would be $3,332, compared to $2,635 on the 30-year term. Plus, refinancing requires paying closing costs again, which usually total 2 to 4 percent of the loan amount.

For many homeowners, paying extra on a 30-year loan offers the best of both worlds: A way to save on interest without the firm commitment of making a bigger payment each month.

Should You Overpay On Your Mortgage?

There’s a lot to be gained from consistently overpaying on your mortgage:

You’ll be out of debt sooner

You’ll save a significant amount in interest

You’ll build equity faster

That said, some homeowners may still want to stay on their loan’s schedule. Either the strain of paying more causes too much stress. Or they’d rather invest the extra payment elsewhere.

What’s best for you? Your answer should match your personal finances and goals.