Title insurance can feel like an overpriced, unnecessary add-on at closing—but in a housing market full of hidden risks, it might just be your best protection against a costly legal headache. While not everyone needs it, this one-time policy can serve as a safety net if an unexpected claim ever threatens your ownership.

You’ve been saving your money diligently, but home prices (and interest rates) seem to just keep rising. Once you’ve finally found a home and are preparing to close, you’re hit with the closing cost estimate: Now you’ve got to add title insurance to the bill, too? Isn’t buying a home expensive enough?

For many sticker-shocked homebuyers already pummeled by a brutal housing market, paying an average of $2,000 for title insurance at closing can feel like pouring salt on the wound. After all, it’s a four-figure expense with little to no tangible benefit (unless, that is, something goes catastrophically wrong).

Some buyers regard title insurance as little more than a scam – a “cash cow for lawyers”, as a Weekend Edition report from NPR phrases it. But if something does go seriously, unavoidably wrong, title insurance protection could save you much, much more than a few thousand dollars.

Title insurance is designed to protect your investment from the hazard of a dirty title – the notion that someone, somewhere, can pop up out of the blue and lay legal claim to your property. According to the American Land and Title Association (ALTA), approximately 25% of all residential real estate transactions have issues with the title. But does that mean title insurance is worth the cost?

The Argument Behind Title Insurance

“Collectively, the title industry protects policyholders from more than $600 billion of estimated risk exposure every year,” says Marcus Ginnaty, spokesperson and senior strategic communications manager at First American Title. That risk is at least partly related to the idiosyncrasies of the U.S. real estate market.

As First American’s vice chairman Kurt Pfotenhauer points out, the U.S. is unique in the way it enables real estate transfers: no advance government approval is required, unlike in other countries. All you need are two parties willing to close the deal. The upside, of course, is incredible speed and financial lubrication, allowing real estate transfers to transact in a matter of weeks without a lot of bureaucratic red tape.

Collectively, the title industry protects policyholders from more than $600 billion of estimated risk exposure every year.

The downside is that the chain of title can get a little … rusty. An unsatisfied mortgage here, a forgotten last will and testament there, and next thing you know, a once-clean title has become defective somewhere along the line.

“According to an ALTA study, 36% of all transactions require extensive, non-routine title clearance efforts,” Ginnaty said in an email. And that’s where title insurance pays off: with that one-time premium, you’ve purchased a promise from the title insurance company that they will do what needs to be done to resolve the claim.

In 2023 alone, the [title insurance] industry paid almost $640 million in claims.

Megan Hernandez, who serves as senior director of public relations & marketing at ALTA, notes that “in 2023 alone, the industry paid almost $640 million in claims.” Mortgage lenders require title insurance if you want to borrow money to buy a home; they stand to lose their investment if someone with a legal claim to the property emerges from the woodwork.

But what about you, the homebuyer? You may be required to buy a lender’s title policy (or at least get an attorney opinion letter), but an owner’s title insurance policy – which protects you, not the lender – is optional. Still, having that protection could help you avoid a wide range of title problems caused by things such as:

Unpaid taxes

Fraud

Forgery

Missing heirs

Undiscovered wills

Void deeds

Errors or omissions in county records

Delinquent tax liens

HOA liens

Child support judgments

Contractor liens

If any of those issues are discovered after you purchase the home, you could be in for a very expensive, very time-consuming journey.

Imagine a contractor discovers the previous owner sold the home – and never completed payment for their costly kitchen remodel? You’d need to hire a lawyer to defend yourself, and could face the very real risk of the home going up for sale to satisfy that lien.

Or suppose the granddad of the person you bought the home from actually bequeathed it to a different family member? Your right to ownership is suddenly called into question. Title insurance protects you from the costly process of defending yourself against the unexpected.

How Title Insurance Helps

A title insurance premium is typically cheaper than an attorney’s retainer fee, yet still provides very real legal protection in the event a defect turns up.

“Title insurance coverage includes a ‘duty to defend,’ meaning the title insurer will hire lawyers and pay defense costs for the homeowner for matters covered by the policy,” Ginnaty said, noting that the investment is relatively small compared to the thousands of dollars you’d have to pay a real estate lawyer to defend your rights in court. Those costs could provide a significant, if not impossible, financial hurdle for some families.

“Title insurance acts as a safety net,” explains Kevin Bazazzadeh, a real estate investor in Houston. “Essentially, you're paying a fee to have someone confirm, ‘We've thoroughly checked this title, and if we've missed anything, you're covered.’ In my opinion, title insurance is not a waste of money,” he said.

What Happens if You Skip Title Insurance?

The fact remains, though, that $2,000 or so is still a lot to pay when the odds are pretty good that nothing will go wrong — and if it does, that you’re otherwise protected or able to cover it out of pocket.

“Most claims are mechanics’ liens equal to tens of thousands of dollars at most,” write Laurie Goodman, Ted Tozer, and Alexei Alexandrov in a 2023 article for the Urban Institute, a nonprofit think tank. They argue that finding ways to bring down the cost of title insurance could make a serious difference for home buyers. Especially since, as they point out, there is a dramatic difference between the cost of a title insurance premium and the losses paid out by title insurance companies.

In fact, by some estimates, title insurance companies pay out only 10% — or even less — in claims compared to what they bring in. (The real cost, title insurance companies will tell you, lies in preventing claims from arising in the first place.)

“It’s important to consider that title insurance providers work to prevent claims from happening in the first place, so most title issues get identified and cleared,” Ginnaty says. “Title insurance has a lower claims rate than auto insurance, for example, because title professionals do a great job of stopping problems before they start. Without that work, the claims rate would be much, much higher.”

So what happens if you keep that money for yourself? While you may not be able to avoid buying a lender’s title insurance policy, an owner’s policy is optional. You might even be able to get a little peace of mind a different way.

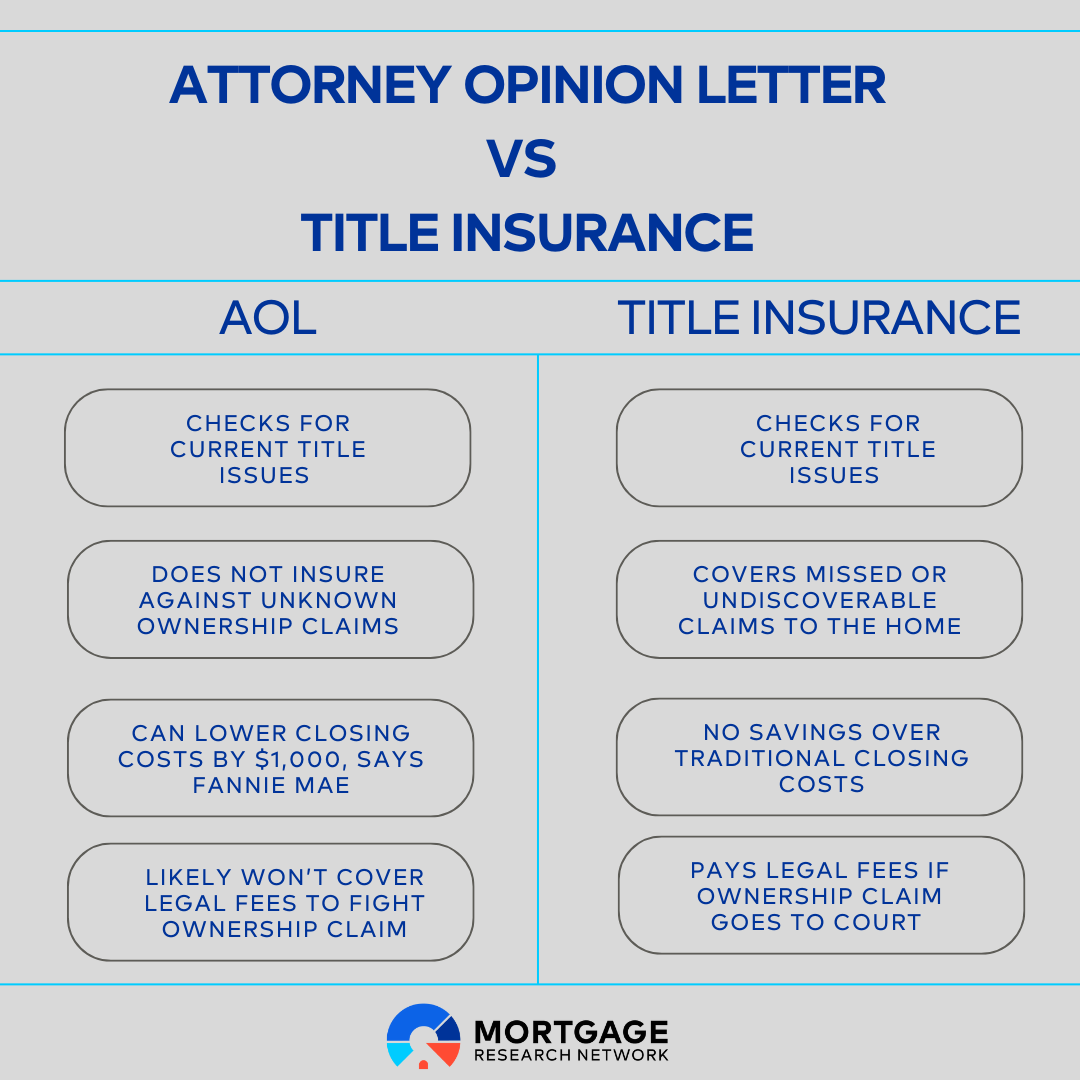

Title Attorney Opinion Letters

Some buyers use title attorney opinion letters to forego title insurance, relying instead on the attorney’s expert opinion on whether the title appears clear. Some Fannie Mae and Freddie Mac loans allow for title attorney opinion letters in certain circumstances. However, the coverage is not the same as what you’d receive through an owner’s policy. You could still be at risk if the title defect was caused by fraud or forgery, for example. According to ALTA, fraud and forgery account for 20% of losses paid out since 2013.

Taking Your Chances

Another method is to close your eyes and roll the dice, as Bazazzadeh, the real estate investor, says.

“In some situations, buying the property at a cheap enough price is such a good deal that it is worth rolling the dice, working through the legal system and waiting,” he said. “If it works out, it is a home run. If it doesn't, it isn't a big enough hit to knock you out of business.” Of course, Bazazzadeh is speaking in terms of a real estate investment business, not from an owner-occupant’s viewpoint. Still, some homeowners could be willing to chance it.

State Guarantee

You could also consider home shopping in Iowa, the one state that outlawed title insurance decades ago. Buy a home there, and you could pay just a couple hundred dollars for a guarantee from the state that your title will be clean.

Is Title Insurance Right For You?

Owner’s policies are optional, and you just may decide to opt out. If you’re trying to save some cash at the closing table, you can ask your closing agent to drop the title insurance, or at least see if there’s any way to negotiate a discount or deal.

As with any insurance product, there’s no benefit to the policyholder if nothing goes wrong. But then again, that’s why they call it insurance. Title insurance is a way to manage (a possibly very expensive) risk, but it isn’t the only way to manage that risk. Only you can decide at which price point title insurance is worth it, and at which point you’d rather play the odds.