What Income Do You Need for a $300k Home?

Exact amounts will vary, but most borrowers will need to earn between $75k and $95k to qualify for a mortgage on a $300k home.

Lenders take various factors into account when determining the income you’ll need to get a mortgage on a $300k home. While your exact number will depend on your financial profile and individual situation, you can expect to be required to have annual earnings somewhere between $75,000 and $95,000.

Factors That Affect Affordability

So, what are the primary factors impacting the size of the monthly payments you qualify for, in turn determining overall home affordability?

The most prominent include your:

Down payment

Debt-to-income ratio

Interest rate

Loan term

Other factors impacting home affordability include your property taxes, home insurance premiums, and any homeowners association dues you’re responsible for. If you’re qualifying with a co-borrower or cosigner, their finances can affect the amount of home you can buy as well.

Related: What's the Real Deal on Down Payments: How Much Do I Need to Buy a House?

Methodology for Our Income Calculations

Before we dive into how each factor impacts the income needed to buy a $300k home, let's go over the standard assumptions we’ll be using (unless otherwise noted) for our calculations:

30-year fixed-rate conventional mortgage

7% interest rate

5% down payment

36% front-end (housing) DTI and 43% back-end (total) DTI

$138 monthly mortgage insurance premium

$125 monthly homeowners insurance premium

$275 monthly property tax payment

$0 homeowners association dues

Minimal monthly debt obligations

Keep in mind that these are just baseline assumptions; your individual figures will likely differ.

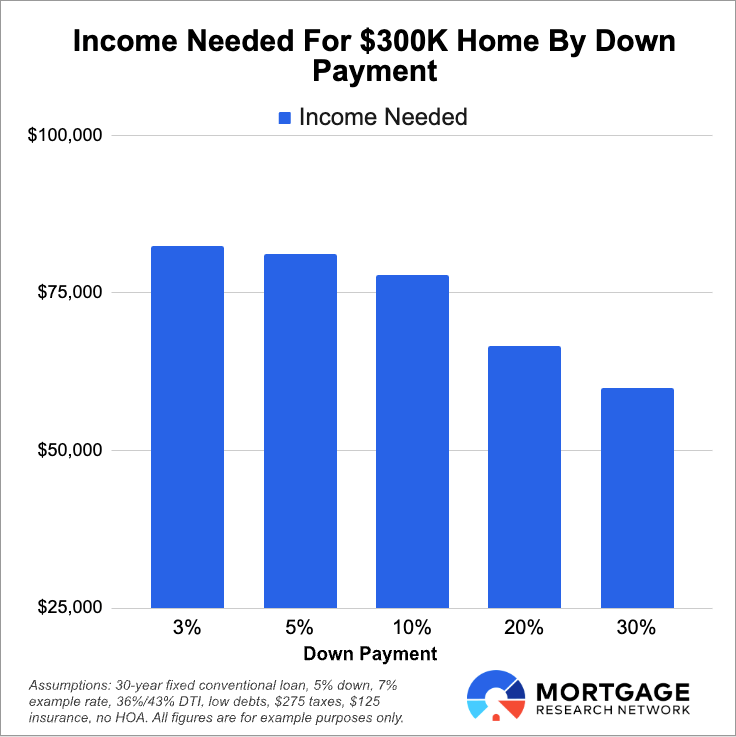

How Your Down Payment Impacts Affordability

The size of your down payment directly correlates to the amount you'll have to borrow for your purchase. By putting more money down, you will need to borrow less, resulting in smaller monthly payments.

Conventional loans typically require 5% down, except for first-time and lower-income buyers eligible for a reduced 3% down payment.

Using our standard assumptions, here’s a chart comparing how different down payments will impact the annual income needed to buy a $300k home.

| Down Payment $ | Down Payment % | Monthly Payment (PITI) | Income Required |

|---|---|---|---|

| $9,000 | 3% | $2,474 | $82,467 |

| $15,000 | 5% | $2,434 | $81,133 |

| $30,000 | 10% | $2,334 | $77,800 |

| $60,000 | 20% | $1,997 | $66,567 |

| $90,000 | 30% | $1,797 | $59,900 |

*estimates with a down payment of 20% or more do not require PMI

A slight increase in your down payment doesn't have a large impact on affordability. Putting 10% down instead of 5% only reduces the income needed by about $3,000 annually.

However, this difference becomes much more pronounced once you reach 20% down and can avoid paying for private mortgage insurance (PMI).

Debt-to-Income Ratio

As we covered earlier, lenders utilize your debt-to-income ratio to determine the size of the payments and loan you're eligible for. This includes a front-end (housing) DTI and a back-end (total) DTI.

Remember that your total DTI includes your proposed mortgage costs as well as any other ongoing debt obligations like:

Auto loans

Personal loans

Student debt

Credit card minimums

Different lenders and loan types may have their own maximum DTI limits, impacting the income you'll need to qualify for a $300k home.

We'll use our standard assumptions for these calculations to show the income needed for a $300k home based on varying amounts of existing debt obligations.

Related: Buying a Car Before Buying a House: Does It Hurt Your Approval Chances?

| Other Debt Payments | Mortgage Payment (PITI) | Total Monthly Debt | Income Required |

|---|---|---|---|

| $0 | $2,434 | $2,434 | $81,133 |

| $250 | $2,434 | $2,684 | $81,133 |

| $500 | $81,133 | $2,934 | $81,879 |

| $750 | $2,434 | $3,184 | $88,856 |

| $1,000 | $2,684 | $3,434 | $95,833 |

| $1,250 | $81,133 | $3,684 | $102,809 |

| $1,500 | $2,434 | $3,934 | $109,786 |

You can have about $500 in non-housing debt payments before it starts affecting the required income, assuming DTI ratios of 36%/43%.

FHA Debt-to-Income Ratio

FHA loans are another popular type of mortgage with a higher debt-to-income limit than conventional lenders allow. Here’s an idea of how much you would need to make to buy a $300k house using an FHA loan based on a 40%/50% DTI and a 3.5% down payment.

| Non-Housing Debt Payments | Mortgage Payment (PITI) | Total Monthly Debt | Income Required |

|---|---|---|---|

| $0 | $2,494 | $2,494 | $74,820 |

| $250 | $2,494 | $2,744 | $74,820 |

| $500 | $2,494 | $2,994 | $74,820 |

| $750 | $2,494 | $3,244 | $77,856 |

| $1,000 | $2,494 | $3,494 | $83,856 |

| $1,250 | $2,494 | $3,744 | $89,856 |

| $1,500 | $2,494 | $3,994 | $95,856 |

Despite making a smaller down payment and having slightly larger monthly payments, the higher DTI ratio on FHA loans can expand your purchasing power and allow you to qualify with lower income levels than comparable conventional mortgages.

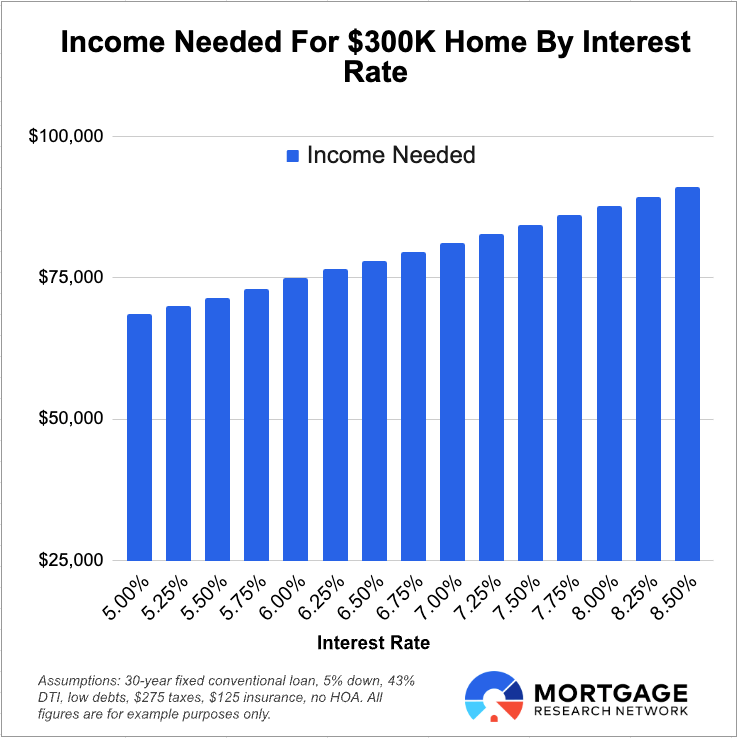

When interest rates go up, your monthly payment goes up too - because you're paying more in interest on the loan. That means lenders might approve you for a smaller loan than you expected, which could change the type of home you can afford.

Interest Rates

Your interest rate affects the income you need, perhaps even more than the home price.

Factors that impact your qualifying interest rate include:

Your credit score

The size of your down payment

Loan type and term

Trends in the financial markets

Rates have risen in the past few years from their all-time lows, which dropped below 2.75% in late 2021 according to Freddie Mac. Based on our methodology, a borrower qualifying at a 3% interest rate could have afforded a $300k home with an income of $58,000 versus $81,000 with rates at 7%.

Currently, however, rates are hovering around 7%, although that can change and the figure you qualify for may be higher or lower depending on market trends and your individual circumstances.

“When interest rates go up, your monthly payment goes up too - because you're paying more in interest on the loan. That means lenders might approve you for a smaller loan than you expected, which could change the type of home you can afford,” says Michael Branson, CEO of All Reverse Mortgage.

Here's an idea of how likely interest rates could affect your monthly payment and, in turn, the income you'll need to purchase a $300k property.

Loan Term

The vast majority of homebuyers take out 30-year mortgages offering lower monthly payments – and a lower required income – than other conventional alternatives. However, shortening your term can save you a significant amount of interest over the life of your loan.

Here’s a look at different mortgage lengths and their payments, the amount they’ll cost in lifetime interest, and the income level needed to support each term.

Loan Term | Mortgage Payment (PITI) | Lifetime Interest | Income Required |

10-Year | $3,847 | $112,091 | $128,233 |

15-Year | $3,100 | $176,099 | $103,333 |

20-Year | $2,748 | $245,304 | $91,600 |

25-Year | $2,552 | $319,296 | $85,067 |

30-Year | $2,434 | $397,600 | $81,133 |

Related: Types of Conventional Loans and Their Uses

Property Taxes

According to the Tax Foundation, effective property tax rates across the United States range from 0.285% to 3.636%, depending on your county. On a $300,000 home, this equates to an annual tax bill between $855 and $10,908.

While home affordability for a buyer in a locale on the lower end of the spectrum won't be largely impacted, shopping in an area with higher property taxes could substantially reduce your purchasing power.

Based on Tax Foundation data, the states of New York, New Jersey, and Illinois consistently have some of the highest effective rates. However, costs can vary by county and location within special tax districts.

Before making an offer on a home, talk with your real estate agent to determine your prospective tax rate and consult your lender to understand how it may impact your financing needs.

Loan Type

We've primarily used conventional loans to determine home affordability so far, but other types of loans may need a higher or lower income to qualify for a $300k home.

A conventional loan is any mortgage issued by private lenders without government backing, but multiple federally insured programs are available to fund buyers who qualify.

The most common program is the FHA loan, which may be cheaper for borrowers with lower credit scores and a small down payment. Homebuyers planning to purchase in rural areas may also be eligible for a USDA loan, while veterans and active-duty servicemembers will want to consider VA loans.

FHA Loans

The Federal Housing Administration insures FHA loans to provide financing for buyers who may not be eligible for a mortgage through conventional lenders, or who may qualify but with payments larger than they can afford.

FHA lending guidelines require:

Credit score of 580

Down payment of 3.5%

Debt-to-income ratio below 50% (56.9% for well-qualified borrowers)

Upfront mortgage insurance premium of 1.75%

Annual mortgage insurance premium between 0.15% and 0.75% (most buyers pay 0.55%)

USDA Loans

Buyers searching for a home in approved rural communities may be able to qualify for a 0% down USDA loan. Insured by the United States Department of Agriculture, these mortgages do not require a down payment and have lower fees than FHA-backed alternatives.

USDA lending guidelines include:

No minimum credit score (although many lenders look for 640 or higher)

No down payment

Debt-to-income ratio up to 44%

Upfront guarantee fee of 1%

Annual guarantee fee of 0.35%

VA Loans

If you’re an active-duty servicemember or honorably discharged veteran, you may be eligible for a zero-money-down VA loan backed by the Department of Veterans Affairs. Commonly the mortgage of choice for borrowers who qualify, VA loans have no ongoing fees and generally come with interest rates lower than conventional products.

VA lending guidelines require:

No minimum credit score (although most lenders require at least 580 to 640)

No down payment

No fixed debt-to-income ratio (lender limits can range from 40% to 50% or even higher)

Upfront funding fee ranging from 1.25% to 3.3% (waived for borrowers with a VA disability rating of 10% or higher)

No ongoing annual fee

Co-Borrowers and Cosigners

If your income level isn’t enough for a $300k home, adding a co-borrower or cosigner to your mortgage application may help you qualify.

That's because lenders will also consider their income, which can give you the boost you need to be approved for the loan you're applying for. Keep in mind, however, that any ongoing debt obligations they have will also be added and can similarly impact your combined DTI ratio.

Gift Funds

Conventional lending guidelines allow family members, spouses, and partners to provide gift funds for your purchase without being co-borrowers or cosigners on the loan. While these funds may not help increase your income or lower your DTI, they can reduce the loan size thereby decreasing the income requirement.

Determining the Income Needed for a $300k Home

It's a common misconception that mortgage companies examine your income and use that figure to assign you a maximum loan amount. In reality, they use your income to determine the size of the monthly payments you can afford and then extrapolate that number into how much they're willing to lend.

Calculating home affordability involves numerous variables that all directly impact the size of your mortgage payments and the overall price point at which you can plan to buy.

The 28/36 Rule

Experts have traditionally recommended that homebuyers abide by the 28/36 rule when deciding how much home they can afford: your housing expenses should be no more than 28% of your income, and your total debt payments – including your mortgage – should be no more than 36%.

While this is a responsible debt-to-income (DTI) target to aim for, rising interest rates and home costs mean it is no longer realistic for all buyers.

As such, most lenders allow for a higher level of debt, which can expand your purchasing power and enable you to afford more home at your current income level.

For example, conventional lenders typically look for a total DTI of 43%, with applicants able to be approved up to 50% in certain scenarios. Other types of mortgages have different limits, with some qualifying borrowers as high as 56.9%.

Other Things to Keep In Mind

While the information provided here should give you some insight into the income needed for a $300k home, there are still some other things that you will want to consider.

Closing Costs

We’ve shown how the size of your down payment affects home affordability, but keep in mind that you’ll also be responsible for paying closing costs. For most borrowers, conventional closing costs will run between 2% and 5% of the price of their home.

For a $300k property, you will likely be looking at an extra $6,000 to $15,000 due in cash at closing. In some cases, such as when purchasing lender discount points to bring down your interest rate, these costs can be even higher.

Failing to properly budget for closing costs can cut into your down payment and increase the income needed for a $300k home.

Cash Reserves

Cash reserves refer to the funds you'll have available after closing once you've made your down payment and paid your closing costs. It's not only wise to ensure you'll have money left over for unexpected expenses; many mortgage companies even require it.

Not all buyers will need cash reserves when purchasing a single-family primary residence. However, some borrowers approved through manual underwriting will need either two or six months of their total housing expenses (PITIA).

If you're purchasing a multifamily property intending to live in one unit and rent out the others, you will need at least six months of cash reserves to qualify for a conventional loan.

Note: FHA loans generally do not require reserves. However, buyers purchasing a triplex or fourplex will need at least three months' worth of housing expenses available after closing.

Future Debt

Although it can be tempting to purchase as much home as you can qualify for, consider your future debt needs before locking yourself into a monthly payment that is too large.

Common future debt considerations should include:

How old is your vehicle, and how soon will you need another one?

Do you plan to finance other purchases, such as furniture for your new home?

Will you be paying college tuition for yourself or a family member in the next few years?

Ways to Save On Your Mortgage Payment

If your income isn’t quite where it needs to be for a $300k home — or if you simply want a little extra leeway in your budget — reducing your monthly mortgage payment can help.

Here are some practical ways that you can save on your mortgage costs to increase affordability or enhance your personal cash flow:

Improve Your Credit Score: Your credit score impacts the interest rate you qualify for. Sometimes, even a minor increase can lower your rate and cut your monthly payments. Depending on your credit report, you may be able to raise your score by 100 points.

Apply for Down Payment Assistance: State-based Housing Finance Agencies, county and municipal governments, and localized non-profit organizations commonly offer down payment assistance programs. These funds can reduce the amount you need to borrow, shrinking your principal and interest payments and lowering your interest rate by improving your loan-to-value ratio.

Purchase Lender Discount Points: Most lenders will allow you to lower your interest rate by purchasing lender discount points at closing. Each point costs 1% of your mortgage and reduces your rate by roughly 0.25%.

Eliminate Mortgage Insurance ASAP: Conventional lenders require private mortgage insurance on all purchases with less than 20% down. Unlike FHA and USDA loans, however, this ongoing premium doesn’t last forever: you can cancel your PMI once you reach 20% equity. If you plan to make improvements to your new home, you may even be able to raise its appraised value enough to remove PMI right away.

Where Is a $300K Home Realistic?

With the rapid rise of property values in recent years, purchasing a home for $300k is not always practical in every market. In some extremely high-cost areas such as San Francisco, New York City, Seattle, or Boston, you simply won't be able to find a single-family home in this price range.

Even in locales such as Denver or Miami, options are typically limited to less sought-after properties needing substantial work (which can be difficult to finance through most lenders).

So, where is the budget for a $300k home a realistic option? According to the National Association of Realtors, some areas with a 2024 median sales price of $300,000 or lower include:

Lincoln, Nebraska ($296k)

New Orleans, Louisiana ($286.6k)

Memphis, Tennessee ($283.7k)

Reading, Pennsylvania ($280.7k)

Louisville, Kentucky ($277.4k)

What about where a $300k budget will get you a property well above average? Some of the cities with much lower median sales prices are:

Mobile, Alabama ($224.4k)

Little Rock, Arkansas ($214.9k)

Topeka, Kansas ($205.8k)

Toledo, Ohio ($186.4k)

Erie, Pennsylvania ($184.7k)

See more affordable cities for first-time buyers.

Taking the Next Step

The income you need to qualify for a $300k home will depend on your down payment, interest rate, existing debts, and various other factors. For most buyers, an income of $95,000 should be sufficient, while well-qualified borrowers may be able to get approved earning $75,000 or even less.

Ready to take the next step? Check to see what interest rates you may qualify for and talk with an experienced lender who can help you determine just how much home you can afford.