How Long Do Home Appraisals Last?

Home appraisals last between 90 and 180 days depending on the lender and loan type, but up to 1 year with an update.

Whether you plan to purchase a home or refinance it, you’re probably going to need a professional home appraisal. Getting one is also a smart idea if you plan to sell your property. But what if you’ve had an appraisal conducted relatively recently: Is a new one still required? For that matter, how long does a house appraisal last? More specifically, how long is a conventional appraisal good for? Or how long is an FHA appraisal good for, or an appraisal for a VA or USDA loan?

While appraisals don’t technically have a set expiration date, a good estimate is about 120 days, although this will depend on multiple factors, including the loan type, lender, and market conditions.

Key Takeaways

The validity of an appraisal depends on various factors, including market fluctuations, property conditions, lender requirements, and loan type, with expiration timelines varying across different mortgage programs.

If an appraisal expires before closing, lenders may request an update or extension to confirm the property's value remains accurate, while a reconsideration of value (ROV) allows for a review if discrepancies or new data arise.

Staying proactive by monitoring appraisal timelines, understanding lender policies, and requesting updates or extensions when necessary can help prevent delays and ensure a smoother financing process.

Factors That Impact Appraisal Shelf-Life

Several different factors can affect how long an appraisal remains valid, the experts explain.

“Market fluctuations matter here. If home prices in your area are jumping up or down quickly, lenders might not trust an older appraisal,” says Steven Glick, director of mortgage sales for HomeAbroad. “Another influence is the property’s condition. It could alter its value. Also, some lenders – especially private or non-qualified mortgage lenders – could have their own rules about how recent an appraisal must be.”

Other elements that can determine the shelf-life of a completed appraisal include economic indicators, seasonal changes, and major events like a natural disaster in the area.

Appraisal Shelf Life by Loan Type

In addition, the type of mortgage loan you choose can also dictate how long a previous appraisal is good for. Let’s take a closer look at the typical appraisal expiration date based on loan type:

Type of Loan | How Long the Appraisal Lasts* |

Conventional loan | 120 days for existing homes, 12 months for new construction homes |

FHA loan | 180 days (can be extended to 12 months with an update) |

VA loan | 180 days (after your loan closes, the appraisal is invalid and can’t be reused) |

USDA loan | 150 days (can be extended to 240 days with an update) |

Jumbo loan | 90-120 days |

*On average, from the effective date of the appraisal report, depending on the lender

Conventional Loan Appraisals

Expect a conventional loan appraisal to remain fresh for up to 120 days (four months), on average. For conventional mortgages purchased by Fannie Mae or Freddie Mac, appraisals can be extended to 365 days (12 months) if an appraisal update is performed after 120 days.

“Conventional loan appraisals, like all appraisals, have an expiration date because they are a snapshot of a property’s value at a specific point in time and must reflect the prevalent market conditions – which can change quickly,” says Dennis Shirshikov, a professor of economics and finance at City University of New York/Queens College. “Because economic factors, local market dynamics, or the conditions of a property can change, an appraisal might become stale, raising concerns about a lender’s risk assessment.”

Conventional loan appraisals, like all appraisals, have an expiration date because they are a snapshot of a property’s value at a specific point in time and must reflect the prevalent market conditions – which can change quickly.

FHA Loan Appraisals

Home loans backed by the Federal Housing Administration, on the other hand, last a bit longer: up to 180 days and up to 12 months with an update after 180 days. Originally, the FHA had lower time limits: 120 days and 240 days (with an update), but chose to extend these appraisal expiration dates three years ago. These extensions bring FHA appraisal timelines in line with industry standards, helping lenders manage appraisals more efficiently. These changes are also aimed at lowering appraisal costs for mortgage lenders and, in turn, making the process more affordable for borrowers applying for FHA-insured home loans.

VA Loan Appraisals

Count on your VA loan appraisal lasting for up to 180 days. After that date, and once your loan closes or your file is terminated, the appraisal is no longer valid, and you cannot update/extend or reuse a VA loan appraisal. The VA sets a 180-day limit on appraisal validity to help safeguard both veteran borrowers and lenders from potential financial risks caused by outdated or inaccurate property valuations.

USDA Loan Appraisals

Another government-backed mortgage, the USDA home loan, isn’t quite as generous with its appraisal expiration timeline. Expect a USDA loan appraisal to remain valid for up to 150 days, although this date can be extended to 240 days with an update. Participating lenders set this time limit to confirm that the property's value matches the loan amount. Their concern? If an appraisal is more than 150 days old, it may not accurately represent the property's current market value, increasing the lender's financial risk.

Jumbo Loan Appraisals

Need a mortgage that exceeds conforming loan limits? If so, your jumbo loan appraisal should last 90 to 120 days, depending on the lender’s rules. However, the lender may need to take extra steps to minimize risk and ensure the property’s value justifies the loan amount. This means the appraisal process can be more thorough than for other types of mortgage loans, often requiring specialized appraisers with experience in high-value properties. In some cases—such as with 95% loan-to-value mortgages, VA jumbo loans over $1 million, or jumbo loans of $1.5 million or more—lenders may even require two separate appraisals for added assurance.

Why Don’t Home Appraisals Last Forever?

Time limits are set on home appraisals for good reasons, the pros concur.

“Real estate markets are constantly evolving, and home values fluctuate over time. Appraisals reflect a home’s estimated value as of a specific date – known as the effective date. Because market conditions can change, an appraisal’s value may no longer be reliable after a certain period,” says Luke Tomaszewski, CEO of ProxyPics, Inc., which provides home valuation and inspection services.

Real estate markets are constantly evolving, and home values fluctuate over time. Appraisals reflect a home’s estimated value as of a specific date – known as the effective date. Because market conditions can change, an appraisal’s value may no longer be reliable after a certain period,

Glick echoes those thoughts.

“Lenders need the most up-to-date value to make sure they’re not lending more than your home is worth. That’s why appraisals expire – not because they’re useless but because real estate prices can change quickly,” he adds.

Keep in mind that if your property's condition changes after the appraisal is conducted, the original appraisal could be revoked, even if it's still valid. This can occur if substantial alterations impact the home, such as if unknown defects are discovered, repairs need to be made, or building or zoning regulations change that influence the status of the property.

Appraisal Updates and Extensions

The good news is that if an appraisal expires prior to your closing date, you may be allowed to update or extend the existing appraisal instead of paying for a whole new appraisal.

An appraisal update involves a brief review of market conditions and, in some cases, a limited property inspection to confirm that your home's value hasn't dropped since your last appraisal. The original appraiser can confirm if your home’s value remains accurate by checking recent home sales in your area. However, an appraisal update does not actually establish a new property value. Instead, the appraiser assesses current market conditions and verifies that the home's value remains consistent with the original appraisal date.

An appraisal extension, meanwhile, lengthens the validity of your existing appraisal without requiring a new evaluation, often used when a closing is delayed and no significant market or property changes.

“To qualify for an appraisal update or extension, your lender will need to ensure that home values in your area haven’t dropped and that your property hasn’t changed significantly,” continues Glick.

Note that you cannot request an appraisal update; the lender must initiate it. Your lender will ask the original appraiser to review market conditions and complete the necessary paperwork to confirm that the property's value has not decreased.

Reconsideration of Value (ROV)

A reconsideration of value (ROV) is different from an appraisal update or extension. It’s a formal request by you or your lender to review your original appraisal when there are concerns about its accuracy or new evidence has emerged.

“During an ROV, you, your agent, or your lender can submit new data to the appraiser. These can include corrected property details that fix, for example, inaccurate square footage or an incorrect room count. The new data can also include additional comparable sales in your area from the last six months that may better reflect your property’s market value,” Tomaszewski explains. “The appraiser then reviews the provided data and either adjusts your home’s valuation if warranted or explains why no changes are necessary.”

Be aware that an ROV request won’t automatically extend your existing appraisal’s expiration date. But it could result in an update or trigger the need for a new appraisal.

Related: Low Appraisal On Your Refinance? What to Do Next

What to do if Your Appraisal Expires

If your appraisal expires, you have options.

“Contact your lender immediately and ask if you’re eligible for an update or extension,” Glick recommends. “To qualify, lenders usually require confirmation from the original appraiser that your home’s value remains accurate, no major changes to your home’s condition have happened, and no significant shifts in your local real estate market have occurred.”

Prepare to document any enhancements to your property, and evidence that conditions in your surrounding area have not changed significantly.

“You can gather recent comparative home sale reports from your agent, or you can request a supplemental home inspection to prove that the current appraisal remains valid,” suggests Shirshikov.

Note that some lenders charge an extra fee to update or extend an existing appraisal.

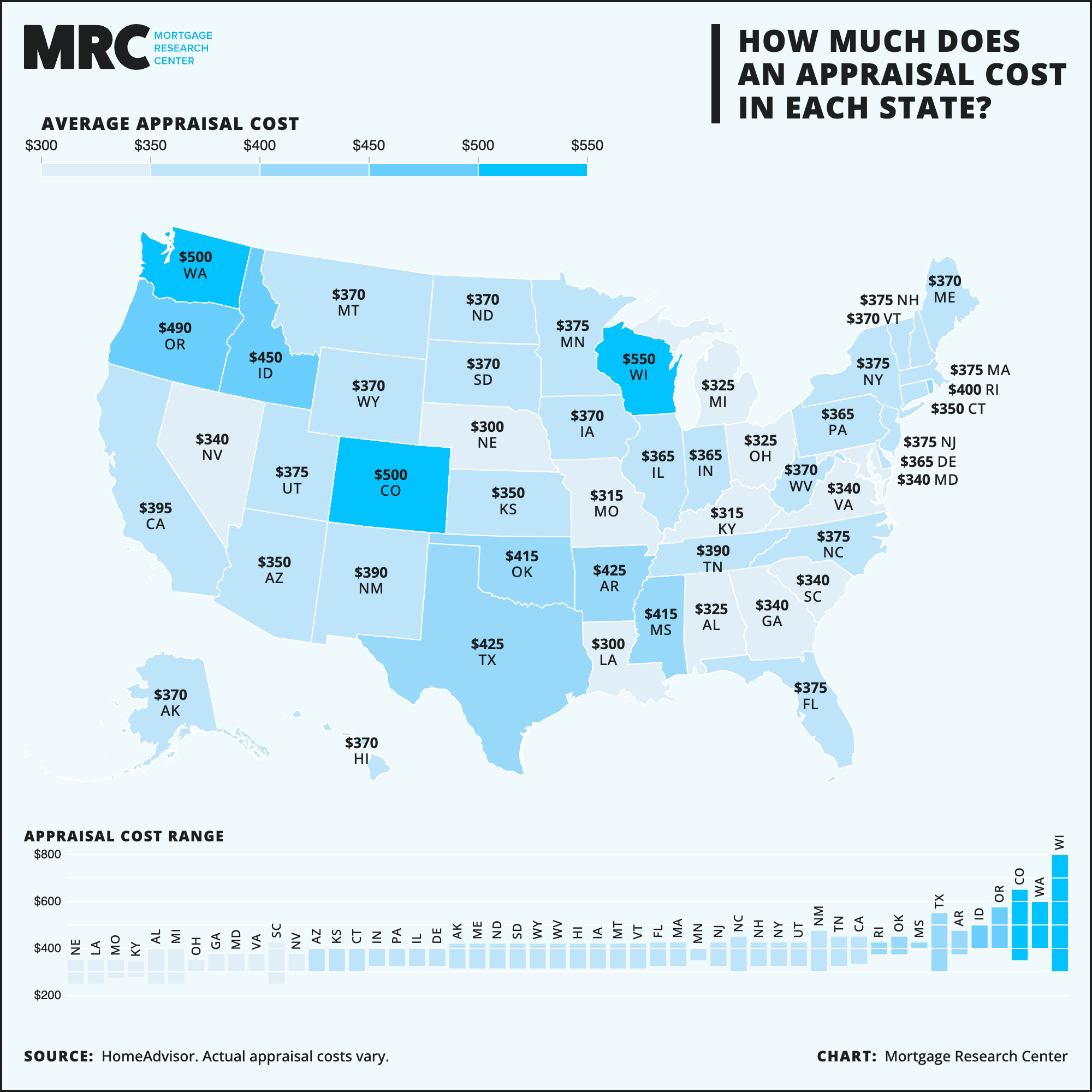

If an update or extension is not an option, or if your existing appraisal has been revoked, prepare to pay for a new appraisal that your lender will order; appraisals typically cost between $300 to $600 but can sometimes run higher, even over $1,000. The upside to getting a new appraisal is that, if you are in a hot market where prices are climbing, the home will appraise for a higher value. That increases your chances of loan approval and lowers your loan-to-value (LTV) ratio, which can help you secure more favorable mortgage rates and decrease the need for private mortgage insurance (PMI).

With a new appraisal, your original appraiser or a new professional will need to inspect your property again; after the appraisal is completed, you can expect the appraisal report within one to three weeks, on average.

“Many home buyers don’t realize they are entitled to a copy of the appraisal report once it is completed,” Glick says. “Reviewing it immediately can help you spot any errors before the original or new appraisal expires, which could prevent costly re-appraisals or delays later.”

Tomaszewski points out that changes are expected to hit the market by next year that could improve the appraisal and valuation process.

“Modernization efforts and updates to the Uniform Appraisal Dataset (UAD) – which professional appraisers use when preparing appraisals for conventional loans – are coming in late 2026 that will bring more standardization and efficiency to the process,” he says.

The bottom line? It’s important to remain vigilant and in regular contact with your lender regarding your appraisal timeframe and market conditions.

“Knowing the details of what makes an appraisal valid and understanding the rules for requesting an update, extension, or reconsideration of value can save time and keep the overall financing process on track while also reflecting current market conditions and property information,” says Shirshikov.