Low Down Payment? Appreciation Will Help You Build Equity and Cancel PMI Faster

Homes in the United States have historically appreciated over time. This appreciation can help new homeowners build equity faster.

Buying a home got you into the game. You’ve stopped paying rent, and you stopped chasing those rising home prices. As a homeowner, you’ll now benefit when home prices go up.

But when will those benefits begin? If you made a small down payment on a 30-year mortgage, your lender owns most of the home. You may have noticed the mortgage balance isn’t exactly spiraling downward. In fact, it’s hardly budged.

At this rate, it’ll take years of consistent payments to lower the mortgage balance and build enough equity to cancel PMI or tap into equity.

Your home’s appreciation can speed up this process.

First, a Quick Refresher on Equity

Equity is the part of your home’s value you’ve already paid off. If you could pay off the entire mortgage balance today, you’d have 100 percent equity. The home would be completely yours. You could sell tomorrow and keep all the profit.

Very few new homeowners find themselves in this position. Buyers who paid nothing down with a VA or USDA loan begin homeownership with no equity. Conventional loan borrowers who paid the minimum 3 percent down start with 3 percent equity.

The lender owns the rest of the home’s value. With each payment, you’re buying back a tiny slice of equity from the lender.

At first, these slices are miniscule; most of the payment goes to interest instead of to the loan’s principal balance. But each monthly payment directs a little more onto the loan’s principal, adding more equity.

The 20 Percent Home Equity Threshold

Once you reach 20 percent equity, you’ve established a solid position from the lender’s point of view. Since the lender no longer holds an excessive amount of risk, you can cancel your conventional loan’s private mortgage insurance (PMI) policy. Canceling PMI could save hundreds every month.

If you used a government-insured loan program, like FHA, to finance the home, reaching 20 percent equity means you can refinance into a conventional loan and stop paying the FHA’s mortgage insurance.

Why Is Home Equity So Important

Building home equity is like charging your phone battery. With every mortgage payment, you’re adding a little more juice to your financial future.

This is what people mean when they describe a home as an investment. Every mortgage payment invests money into your asset: equity in your home.

When you’ve charged up enough home equity wealth, you can start using it for things like:

Retirement Planning

Home equity can help fuel a retirement plan. A paid-off home is a big asset. Retirees can sell their homes to cash out this asset. With profits from the sale, they could buy a smaller home and use or reinvest the rest of the cash in other places.

Retirees who want to cash out home equity without selling their home can get a reverse mortgage. Reverse loans turn equity back into cash, and they don’t require monthly payments. They do charge interest. At some point, reverse loans and their accrued interest must be repaid, either by the homeowner or their survivors.

Homeowners should work with a retirement planner to create a plan that’s specific to their needs. Avoiding a reverse mortgage will make the home a stronger asset for surviving family members.

Improve the Home, Building Even More Equity

Homeowners can leverage their equity to borrow more money with a home equity loan or HELOC. Home equity loans and lines of credit, in essence, exchange equity for cash.

Borrowers can use the cash for any purpose, but using the cash to improve the home is especially smart. This method reinvests equity into the home, using equity to build more equity.

Updating kitchens and baths — or adding on an extra bathroom, bedroom, den, or office — can supercharge a home’s value and grow equity faster. Plus, homeowners can write off the interest paid on their home equity loans if the loan pays for home improvements.

After taking out a home equity loan, the homeowner makes monthly payments on the loan’s balance, slowly restoring the equity again. When the equity has been restored, it can be used again.

Buy More Real Estate

Homeowners can spend cash from a home equity-backed loan to buy another real estate property. In this way, equity can help pay for a vacation home or an investment home that can generate passive income from rent.

Since equity secures the loan, lenders charge lower interest rates on home equity loans compared to rates for unsecured personal loans. Some homeowners use home equity loans to make the down payment on a second home.

Provide Inheritance for Heirs

Like any asset, home equity can be passed onto future generations. Your heirs could live in the home, rent it out for income, or sell it to build more financial stability for themselves.

Be sure to work with an estate planner to make sure your heirs get the most benefit from all of your assets.

How Home Appreciation Works

Paying down the mortgage isn’t the only way to build home equity. The home’s gradual increase in value also builds equity. Like any investment, the value of your home isn’t guaranteed to grow, but historically, real estate tends to appreciate.

As the graph below shows, appreciation isn’t a steady, consistent climb. Housing prices might stagnate or even decrease for a few years at a time. But, in the big picture, almost all real estate is more valuable now than it was a generation ago.

People who treat their homes like a long-term investment usually benefit from growth in house prices.

And unlike the equity you built by paying down the mortgage, equity built through appreciation never belonged to the lender to start with. So equity gains from appreciation aren’t diluted by interest and fees. This can make appreciation a faster path to building wealth.

It’s Not Just Principal That’s Going Towards Your Equity

To recap, making regular payments slowly chips away at the mortgage balance, growing home equity. At the same time, home appreciation adds value to the home, also growing equity.

To see the power of appreciation at work, let’s look at a $300,000 home.

If you’ve paid the $300,000 loan balance down to $280,000, you’ve earned $20,000 in equity

If the $300,000 home you bought is now worth $340,000, you’ve earned another $40,000 in equity

That’s $60,000 in equity, even though the loan balance has decreased by only $20,000.

More Specific Examples

The following examples show how appreciation can supercharge equity building for a $300,000 home, helping homeowners reach the 20 percent equity target sooner.

Down payment | Time to build 20% equity by paying down loan balance | Time to build 20% equity with 4% yearly appreciation |

3% ($9K) | 11 years, 8 months | 3 years, 10 months |

5% ($15K) | 10 years, 10 months | 3 years, 5 months |

7% ($21K) | 9 years, 11 months | 3 years, 0 months |

10% ($30K) | 9 years, 5 months | 2 years, 5 months |

In the example above, the homeowner makes the same monthly payment. Appreciation amplifies the power of each payment.

The graph below shows how home appreciation of 4% can speed up equity growth for a homeowner who put 3 percent down on a $300,000 30-year loan at 7 percent interest.

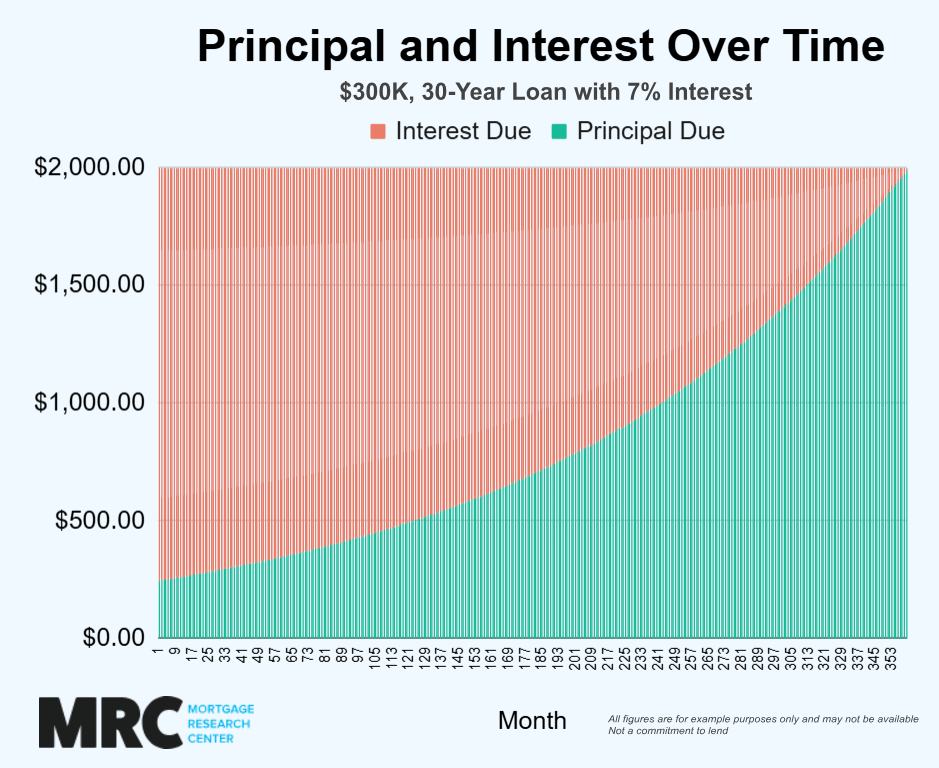

One reason for appreciation’s potential to speed up equity building: Equity built through making payments happens so slowly. During the first few years of a 30-year term, monthly payments have a small impact on the loan’s principal balance. Most of the payments go to the loan’s interest. Let's take a look at how one's monthly mortgage payments may look if they put 3% down ($9,000) on a $300,000 home, with 7% interest and a 30-year term:

| Month | Principal Due | Interest | Loan Balance |

| 0 | $0.00 | $0.00 | $291,000.00 |

| 1 | $238.53 | $1,697.50 | $290,761.47 |

| 2 | $239.92 | $1,696.11 | $290,521.55 |

| 3 | $241.32 | $1,694.71 | $290,280.23 |

| 4 | $242.73 | $1,693.30 | $290,037.50 |

| 5 | $244.14 | $1,691.89 | $289,793.35 |

| 6 | $245.57 | $1,690.46 | $289,547.78 |

| 7 | $247.00 | $1,689.03 | $289,300.78 |

| 8 | $248.44 | $1,687.59 | $289,052.34 |

| 9 | $249.89 | $1,686.14 | $288,802.45 |

| 10 | $251.35 | $1,684.68 | $288,551.10 |

| 11 | $252.82 | $1,683.21 | $288,298.28 |

| 12 | $254.29 | $1,681.74 | $288,043.99 |

All figures are for example purposes only.

Each monthly payment will send slightly more to principal and less to interest. By the end of the term, almost all of each payment goes to principal.

Eventually, a decade or so into the 30-year term, the buyer starts to build momentum toward paying down the principal, as the curve above shows. Someone who sells the home within a few years of buying may be disappointed in how little the mortgage balance has decreased.

That said, buyers can bypass this schedule and improve their equity position faster by making extra payments directly onto the loan’s principal, along with making the regular payments needed to keep the loan current.

And, of course, appreciation can help drive up the home’s value, especially in hot housing markets.

Appreciation Makes 20% a Moving Target

Before buying a home, back when you were saving money for a down payment, you were chasing a moving target. Because of inflation, the $10,000 saved for a down payment one year was worth only $9,600 a year later. A year after that, it was worth only $9,160.

This is true in markets where homes appreciate at the average rate of 4 percent a year. Savers have to plan for this and save even more than they’d need this year.

But after buying a home, this same home appreciation benefits homeowners.

A home worth $300,000 this year could be worth $312,000 next year, and worth $324,480 the year after that, based on that same 4 percent appreciation rate.

At this appreciation rate — when combined with making regular payments on the home — the homeowner can hit the 20 percent equity threshold faster. They reach it faster because the 20 percent mark changes as the home’s value changes while the amount borrowed does not change.

Appreciation Isn’t Guaranteed, but It’s Likely

Homes don’t always appreciate. Like any investment, homes could even decrease in value. Despite this financial reality, most homeowners who wait long enough will enjoy an increase in their home’s value.

Some homeowners will need more patience than others. Someone who bought a home in 2010, for example, in the midst of the Great Recession, may have seen little to no home appreciation for three or four years. Then, as the housing market eventually started to recover, the home likely started to inch up gradually.

Finally, during the Covid-19 pandemic when mortgage rates hit historic lows, this homeowner may have seen the home value skyrocket. By 2022, 12 years after buying, the home may have doubled in value. This fast growth between 2016 and 2022 helped compensate for the slow growth between 2010 and 2016.

Over time, these ups and downs tend to average out, landing on an appreciation rate of about 4 percent per year.

Home buyers can’t control their local housing markets’ appreciation rates, but maintaining their homes can help them appreciate more, within the context of local market conditions.

When It’s Time to Contact Your Lender

How can you know when you have 20 percent equity and can ask your lender to cancel private mortgage insurance?

The most reliable way to measure value is to order a new home appraisal. An appraiser will study your local housing market, visit your home to see its size and condition, and then assign an official home value. An appraisal will usually cost $500 to $1,000.

But this type of formal appraisal may not be required. You can also use an automated valuation model (AVM) like the ones you see in action on real estate websites. AVMs let algorithms do the work. Not all lenders will accept an AVM, especially if you’re close to the 20 percent threshold.

Whether you use an AVM or a formal appraisal, ditching PMI a few years early by requesting a cancellation can save more than the cost of the appraisal. If an AVM says your home value is about 25 percent higher than your current mortgage balance, it’s worth asking your lender to cancel PMI, even if the lender insists on ordering a formal appraisal.