Gift of Equity: What It Is and How to Use It to Buy a Home from a Relative

A gift of equity allows family members to sell a home to relatives while providing funds that may help with the down payment, closing costs, or both, depending on lender guidelines. This can reduce upfront costs and, in some cases, eliminate mortgage insurance.

If coming up with a down payment has been a challenge, purchasing from a relative could offer a unique advantage. Many lenders allow a family member to provide a gift of equity, which can help cover your down payment, closing costs, or both—potentially making homeownership more within reach.

What Is a Gift of Equity?

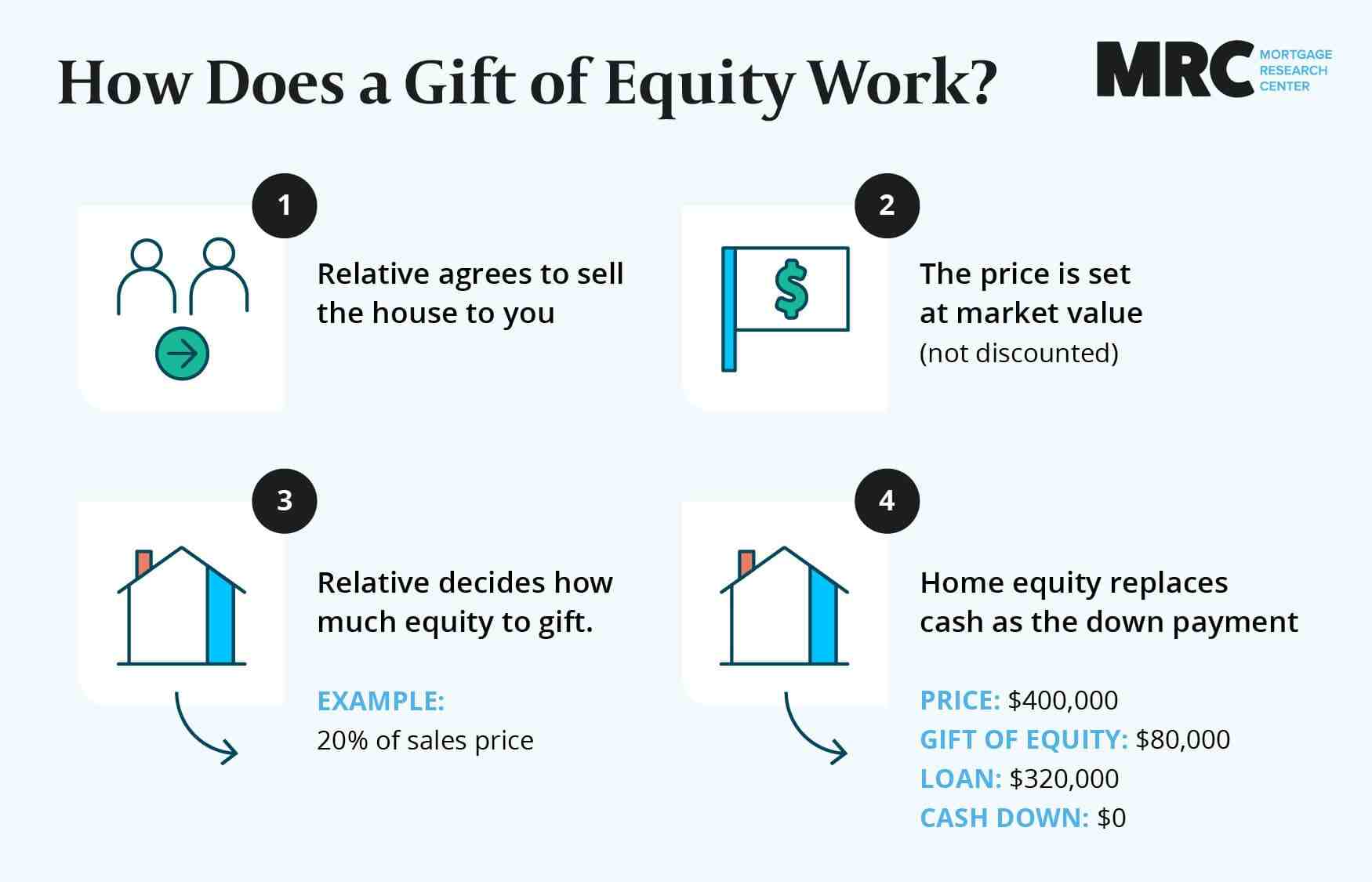

A gift of equity is when one family member sells a home to another at market price while gifting a portion of that price to the buyer to cover the down payment, closing costs, or both.

While it’s not technically the same as a discounted sales price, it functions in a similar way. Instead of lowering the home’s sale price on paper, the seller offers part of their equity as a financial gift. The buyer gets credit for that amount, and the lender treats it as if the buyer brought those funds to the table—even though no actual cash is exchanged.

How Does a Gift of Equity Work?

This gift of equity is documented on the final settlement statement, also called the Closing Disclosure or CD. The escrow company adds the gift to the document. On paper, it is considered the same as the buyer's own funds. It can cover down payment and closing costs, even though no actual cash changes hands.

For Example: If your grandparents want to downsize and are willing to sell you their house worth $350,000. They offer a $80,000 gift of equity, which covers 20% down ($70,000) plus $10,000 for closing costs.

Their net proceeds from the sale are reduced by $80,000 and these funds are considered your down payment and closing costs. You end up with a loan of $280,000 with no down payment or closing costs on a home worth $350,000.

Here’s what the sale would look like for the seller with a gift of equity and without:

Gift of equity | No gift of equity | |

Sale price | $350,000 | $350,000 |

Gift of equity | $80,000 | $0 |

Other seller costs | $15,000 | $15,000 |

Seller’s existing mortgage | $100,000 | $100,000 |

Net proceeds to seller | $155,000 | $235,000 |

See how the gift of equity functions similarly to a reduced sales price? On paper, the home sells for the full market value, but the proceeds are reduced. In this way, a seller is able to offer a down payment gift to their relative without exchanging actual cash.

Here’s how this might look for a buyer. Without the gift of equity, they’d need to bring at least 3% down plus closing costs to the table:

Gift of equity | No gift of equity | |

Sale price | $350,000 | $350,000 |

Gift of equity | $80,000 | $0 |

Minimum down | $0 | $10,500 |

Closing costs | $0 | $10,000 |

Total due at closing | $0 | $20,500 |

Resulting loan amount | $280,000 | $339,500 |

What’s more, the buyer would be responsible for private mortgage insurance without the gift of equity., That could mean an added bill of hundreds of dollars per month tacked onto their mortgage payment.

How Do You Determine Where the Funds Go?

The lender typically decides how the gift of equity is applied based on the loan program and what’s needed to qualify. Most often, the funds are first applied to meet the minimum down payment requirement. If there’s extra equity beyond that, it can go toward closing costs. Your lender will review the loan details and let you know exactly how the gift is allocated on the Closing Disclosure.

When Can You Use a Gift of Equity?

A gift of equity can only be used when one family member sells a home to another family member. In addition, most lenders restrict gifts of equity to your primary or secondary residence. However, some non-conforming loans might allow you to receive a gift of equity on an investment property.

You may use a gift of equity with all standard loan types. This means you can still qualify for conventional loans and mortgages backed by the FHA, VA, and USDA.

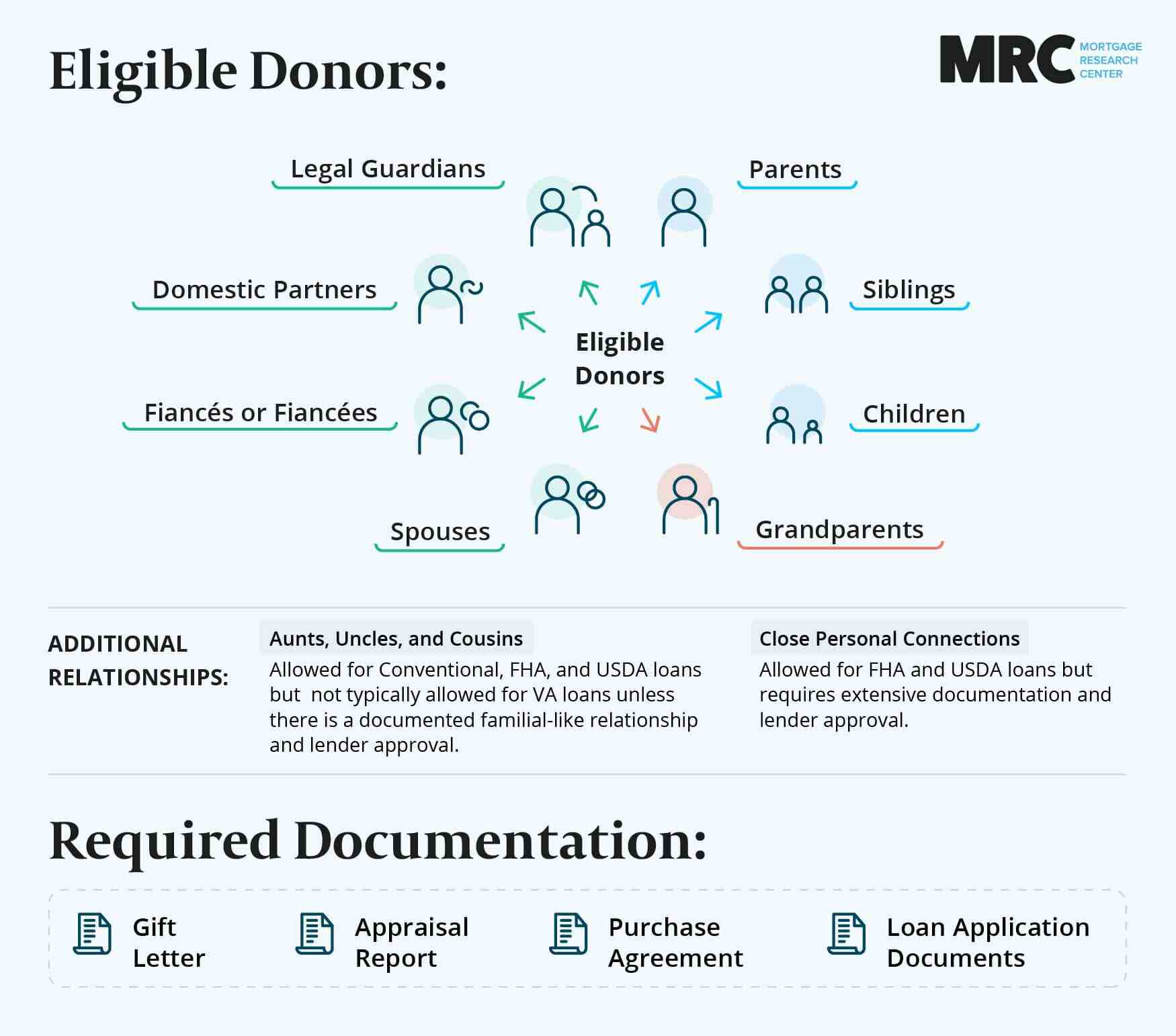

Eligible Gift of Equity Donors

Most of the time, gifts of equity occur between parents and children or grandparents and grandchildren. But conventional lenders specify a number of other eligible gift of equity donors, including:

Spouses, domestic partners, and fiancées or fiancés

Legal guardians of the borrower or someone whom the borrower is the legal guardian of

Anyone else related to the borrower by blood, marriage, adoption, or legal guardianship

Some lenders have an even more generous list of eligible donors. Fannie Mae and Freddie Mac, the two government-sponsored enterprises that set guidelines for conventional loans, each carve out a couple of other donor options:

Fannie Mae: Lending guidelines explicitly allow borrowers to receive a gift of equity from former relatives, relatives of a domestic partner, godparents, or even an estate or trust established by an acceptable donor.

Freddie Mac: Lending guidelines explicitly allow borrowers to receive a gift of equity from unrelated individuals with “close, family-like ties.”

Like Fannie Mae, Freddie Mac allows gifts of equity from a relative's trust or estate.

Note: Not all conventional lenders work with both Fannie Mae and Freddie Mac. If your gift of equity purchase involves one of the more uncommon familial situations and your lender isn’t able to originate your loan, the best thing you can do is to apply with another lending professional with access to different loan products.

Pros and Cons of Using a Gift of Equity

A gift of equity can make homeownership more accessible when buying from a family member, but it’s worth considering both the advantages and potential tradeoffs.

Pros

Reduces or eliminates the need for a down payment, and in some cases, covers closing costs

Makes it easier to qualify for a mortgage if you're short on savings or have limited income

May help you avoid private mortgage insurance (PMI) if the gift equals at least 20% of the home’s value

Keeps the home in the family, often without needing to list it on the open market

Available with most major loan types, including conventional, FHA, VA, and USDA loans

Cons

The seller receives less cash from the sale compared to a traditional transaction

Can only be used between family members (or individuals with close, family-like ties, depending on loan type)

May have tax reporting requirements for the seller if the gift exceeds annual IRS limits

A professional appraisal is still required and could impact the loan if the value comes in low

Rules vary by loan type, and some restrictions may apply—such as how the gift can be used or minimum required gift amounts

Documentation Needed for a Gift of Equity

If you're purchasing a home with a gift of equity, you only need slightly more documentation than for a standard loan. The steps required with a gift of equity include the following:

The seller will need to have a professional appraisal completed to establish the property's current value.

Your escrow company will use this appraisal and the sales price to calculate your gift of equity and add it to the final settlement statement.

The seller must provide a signed gift letter that includes their contact information, relationship to you (the borrower), the actual or maximum dollar amount of the gift, and a statement that the gift of equity does not require repayment.

Otherwise, you’ll just need the usual documentation required for most mortgages, including:

The last two years of tax returns

Your two most recent pay stubs

Bank account statements

The last two years of W-2 form

Gift of Equity by Loan Type

You can use a gift of equity with most lenders, but each mortgage product will have slightly different rules depending on the guidelines that the lender follows. Here are some of the gift of equity specifics that can vary by loan type:

Fannie Mae (Conventional): Fannie Mae allows gifts of equity to fund some or all of the down payment and closing costs. Unlike cash gifts, a gift of equity cannot be counted toward financial reserves – extra funds required after closing. For some high-LTV loans on second homes or multi-unit properties, you may need to contribute 5% down from your personal funds.

Freddie Mac (Conventional): Freddie Mac's guidelines are similar to Fannie Mae, although they have no stated rule against using a gift of equity for a borrower’s financial reserves. You may also receive a gift of equity from a relative’s trust or estate.

FHA: FHA guidelines specify that if a family member sells their investment property to another family member as a primary residence, they must give at least a 15% gift of equity. Lenders may waive this requirement if the buyer has been a tenant in the home for at least six months.

VA: Gifts of equity can be used toward a down payment on VA loans. However, they are not allowed to be applied to closing costs.

USDA: All gifts of equity must be reflected as a sales price reduction for USDA loans, and the borrower cannot receive cash back at closing. The USDA allows gift funds for closing costs and prepaid expenses.

Gift of Equity Tax Implications

For most people, there won't be any immediate tax implications when giving or receiving a gift of equity. IRS guidelines for 2025 allow for an annual tax-free gift exclusion of $19,000 per recipient. A married couple giving a gift of equity could provide $38,000 without the assistance needing to be reported.

Gifts of equity over the annual gift exclusion must be reported to the IRS through Form 709, although most individuals are still unlikely to face any additional tax burden.

That's because the amount above the annual limit counts toward the donor's lifetime exclusion limit, which is $13.99 million in 2025. Once the donor exceeds this lifetime limit, taxes are only charged on gifts of equity.

Note: Everyone's situation is different, and donors should talk with their tax professional or financial advisor to understand the tax implications they may encounter when giving a gift of equity.

Buyers aren't responsible for gift taxes related to gifts of equity. And because they technically purchased the home at market value, they shouldn’t experience higher capital gains than they normally would. However, buyers should consult their tax professional before selling a home they purchased with a gift of equity to make sure there are no “gotchas” in the tax code regarding equity gifts.

Frequently Asked Questions About Gifts of Equity

Still trying to figure out how gifts of equity work? Here are some answers to the most frequently asked questions from borrowers:

Who can give a gift of equity?

A gift of equity must be given from one family member to another. This is typically between parents and their children or grandparents and their grandchildren but can apply to a variety of other familial relations, including but not limited to:

Siblings

Godparents

Former relatives

Domestic partners

Do you have to pay taxes on a gift of equity?

Most people will not have to pay taxes on a gift of equity. Contributions above the annual gift exclusion ($19,000 per person in 2025) are counted towards the donor’s lifetime gift tax exclusion ($13.99 million in 2025). Gifts of equity that are in excess of the donor’s lifetime gift tax exclusion may incur taxes, but most individuals will never reach that limit. Always consult a tax professional before filing.

How does a gift of equity affect the seller?

Giving a gift of equity is an excellent way for a seller to keep a home within the family while providing their relative the down payment assistance. But even though most sellers won't encounter any gift tax implications, they need to understand they are giving away equity that could otherwise be cashed out if they sold the home to a non-relative.

Another seller benefit of giving a gift of equity is that it’s generally done off-market, without the help of a real estate agent. While there will still be closing costs, avoiding broker commissions can save 5-6% of the home's market value.

Can you get a gift of equity on an investment property?

Unfortunately, conforming loans (conventional loans and those backed by governmental agencies like the FHA, VA, and USDA) do not allow you to use a gift of equity on an investment property. Second homes are alright, but you can't purchase the residence to rent it out.

Can a gift of equity eliminate the mortgage insurance requirement?

Yes! One of the most valuable advantages of using a gift of equity with a conventional loan is avoiding private mortgage insurance requirements. All that’s needed is a gift of equity (or a combination of a down payment and gift of equity) of at least 20% of the property's value.

A Gift of Equity Can Make You a Homeowner

If you're having trouble saving for a down payment or can't qualify for a mortgage at current market prices, a gift of equity can make you a homeowner. If you have a relative willing to give you a gift of equity, apply with a lending professional today to discuss the details of your situation to find a loan suited to your specific needs.