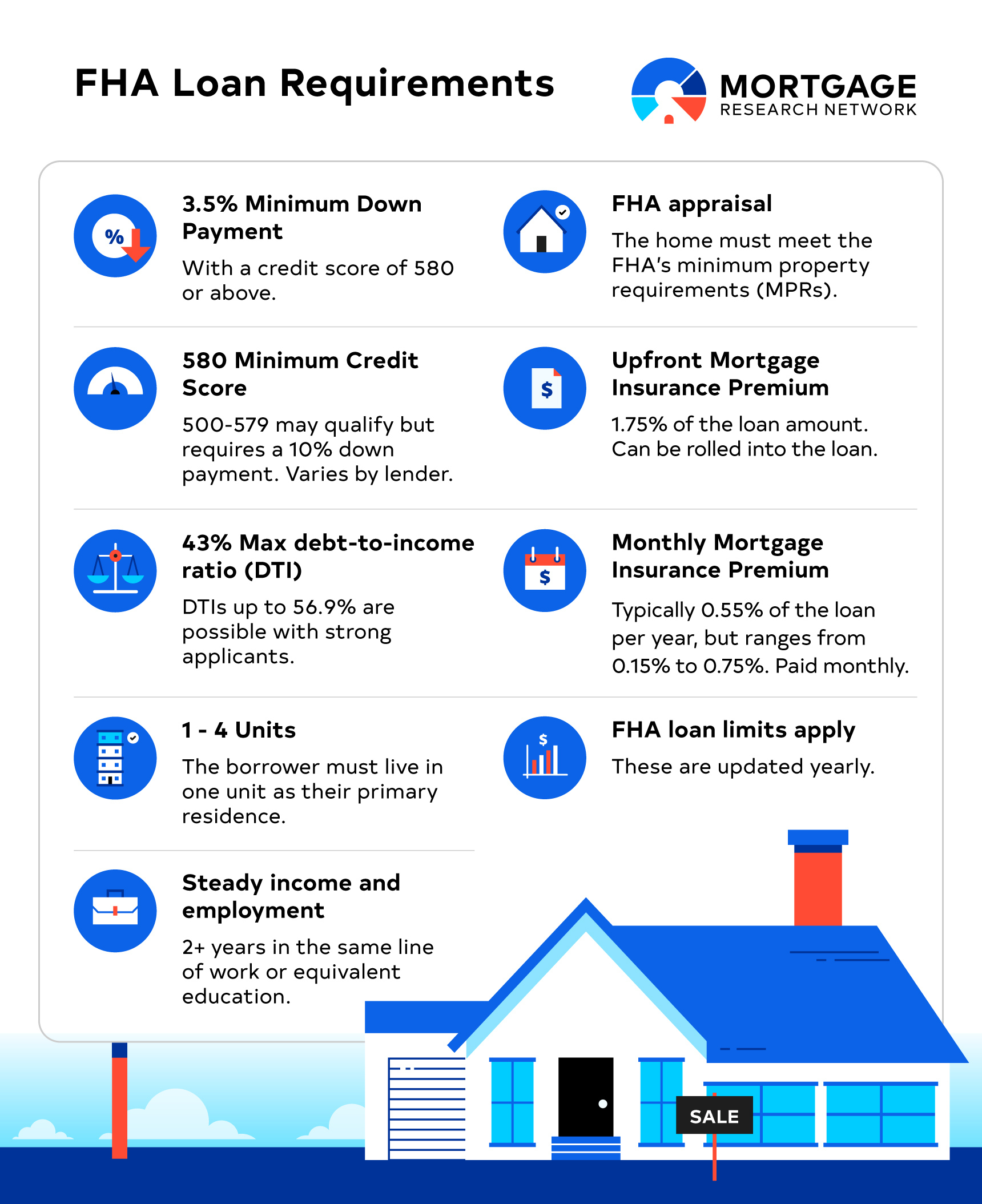

While it’s a generous loan option, FHA loans come with several key requirements prospective borrowers will need to meet or exceed, including minimum credit score, minimum down payment, and maximum debt-to-income ratio.

FHA loans more easily open the door to homeownership for many buyers who would otherwise not be able to afford or qualify for a conventional mortgage loan. But even though this form of financing is less restrictive, it’s important to be aware of FHA loan requirements that you must meet.

FHA Loans: What’s Changed For 2026

The eligibility requirements for FHA loans this year have largely remained consistent with previous years.

“But borrowers should keep an eye on loan limits, which are updated annually to reflect changes in home prices,” says Carl Holman with A&D Mortgage. “In 2026, FHA borrowing limits have increased in many areas to account for rising housing costs, making it easier for buyers to access homes in high-cost regions.”

See up-to-date loan limits here.

“Also, there have been ongoing discussions about lowering FHA mortgage insurance costs, although nothing has changed yet,” says Martin Boonzayer CEO of The Trusted Home Buyer.

Minimum Credit Score: 500

You’ll need a minimum credit score of 500 to be eligible for an FHA loan.

“This is incredibly low compared to other loan types. The reasoning is that FHA loans are designed to help first-time and lower-income buyers get into a home – even if their credit isn’t perfect,” personal finance expert Andrew Lokenauth explains. “In contrast, the minimum credit score needed for a conventional loan is usually around 620 to 640.”

Keep in mind that lenders set their own credit score requirements.

“Every lender that provides FHA loans has its own risk threshold. While 500 may be the stated guideline minimum, most lenders want a credit score of 580 or more,” explains Matt Schwartz, founder of VA Loan Network. “I have underwritten a few FHA loans for borrowers with credit scores in the 550s, but these are rare.”

Note that your credit score will impact the minimum down payment you’ll need to make, discussed next.

Minimum Down Payment: 3.5%

FHA loans are not quite as generous as VA or USDA government loans, which have no down payment requirement. But an FHA loan can still be had for as little as 3.5% down – although you’ll need a credit score of 580 or higher for that privilege. If your credit score ranges between 500 and 579, you must put down at least 10%. That’s still more favorable than the minimum down payment needed for most conventional loans: at least 20%.

But remember that the higher your down payment, the less you’ll need to borrow and the greater your equity position will be at closing (the amount of the property you will own outright). You can make a down payment of greater than 10% if you choose, although you’ll still have to pay mortgage insurance regardless.

Mortgage Insurance

As with conventional loans for which you put down less than 20%, you’ll have to pay for mortgage insurance on an FHA loan, no matter your down payment amount. Mortgage insurance is required to protect the lender from the risk of default in case you cannot or will not pay your mortgage debt.

You’ll be charged a one-time upfront mortgage insurance fee paid at closing, which equates to 1.75% of your loan amount, as well as monthly mortgage insurance premiums that equate to anywhere from 0.40% to 0.75% of your FHA loan amount.

The most common figure is 0.55% per year, or about $46 per month per $100,000 in loan amount.

“The size of your down payment directly impacts mortgage insurance premiums for FHA loans. Borrowers who put down less than 10% will have to pay monthly mortgage insurance premiums for the life of the loan unless they refinance to a new loan. And those who put down 10% or more can have mortgage insurance removed automatically after 11 years.”

Fortunately, if you refinance your FHA loan to a new FHA mortgage, you may qualify for a refund of your one-time upfront mortgage insurance fee.

Maximum DTI

The maximum DTI for FHA loans is technically 56.9%, but you have to have a very strong scenario in all other aspects of the loan. A more realistic DTI for most borrowers is around 50%.

Your debt-to-income (DTI) ratio is an important metric the lender will look closely at that compares your monthly debt payments to your monthly income. To calculate your DTI ratio, sum up all your monthly debt payments, such as credit cards, student loans, auto loans. Then add your full expected housing payment including principal and interest, property taxes, homeowner’s insurance, and HOA dues, if any. Then, divide the total by your gross monthly income and express the result as a percentage.

A low DTI suggests you have more disposable income and are less likely to default on your debt, while a high DTI may indicate difficulty in managing monthly payments.

Holman states that FHA has more lenient DTI guidelines than conventional loans’ 43% typical maximum. “This flexibility is designed to help borrowers with higher debt loads, such as those with student loans or medical bills, achieve homeownership. However, lenders may still evaluate compensating factors, such as a strong credit history or significant cash reserves, before approving higher DTI levels.”

Employment: 2+ Years

Be prepared to demonstrate a stable income history if you want the green light on an FHA mortgage.

“You must have a consistent two-year work history, which does not have to be two consecutive years at the same employer,” says Schwartz. If you are off of work, you must be back to work for six months before you can use that income. Things like overtime, commissions, and bonuses require a verifiable two-year history of receipts.”

Gaps in your employment history will require an explanation to the lender.

“Lenders look for reliability and a steady ability to meet financial obligations, making the two-year history an important factor in approval decisions,” Holman points out.

For freelancers or other self-employed individuals, you’ll need to furnish extra documentation, like tax returns, to substantiate your earnings.

FHA Appraisal

Another hurdle you’ll have to clear is getting an FHA appraisal.

“This appraisal isn’t the same as a professional home inspection. While the latter looks for things like electrical issues or plumbing problems, the appraisal is more focused on the home’s value and condition,” says Boonzayer. “The FHA-approved appraiser will make sure the home meets certain safety standards, such as having no structural issues or health hazards like mold. It’s more about ensuring the home is safe and livable.”

Unlike a standard appraisal required for conventional loans, FHA appraisers are obligated to check for things like the integrity of the roof and HVAC system as well as basic habitability.

“Aside from the appraisal, buyers should also separately hire a professional home inspector to evaluate the property in detail, which is not required but strongly recommended,” suggests Holman.

Related: Free Home Inspection Checklist

Property Types & Occupancy Requirements

When it comes to an FHA loan, the type of home you want to purchase and how you will use it also matters a great deal.

“FHA loans are only approved if you plan to live in the home as your primary residence,” says Boonzayer. “You could purchase a single-family home, an approved condo, a duplex, a triplex, a fourplex, a manufactured home, or a fixer-upper – provided you live in one of the units. And while you can technically have multiple FHA loans at a time, you can only do so under specific circumstances, such as if you are relocating for work. The bottom line is that FHA loans are designed to help you secure a primary residence, not an investment property.”

Note that you must occupy the FHA-financed property within 60 days of closing.

“Additionally, your job must be a reasonable commute from the house. If you are working remotely, that works as well, as long as it can be verified through human resources that you actually telecommute and that relocation would not change your employment with the company,” Schwartz explains.

Want to buy a property with an existing accessory dwelling unit (ADU) you intend to rent out, or yearn to build a new ADU on your FHA-financed property? The good news is that FHA financing is now also available for both new construction of ADUs and via the FHA 203(k) rehabilitation loan program, with rental income calculated based on either the fair market rent or lease agreement.

You can now use a portion of the rental income from an existing ADU to qualify for an FHA mortgage, with up to 75% of the estimated income counted, while new ADUs allow for up to 50%. Rules and restrictions apply, so consult closely with your FHA lender.

More information on FHA loans and ADUs:

Can you use an FHA loan on a property with two ADUs?

FHA Loans and Multifamily Homes with an ADU

Loan Limits

FHA loan limits may increase each year if national housing prices rise. Limits for 2026 are as follows.

| Units | Standard FHA Limits 2026 | FHA High-Cost Limits 2026 |

|---|---|---|

| 1 | $541,287 | $1,249,125 |

| 2 | $693,050 | $1,599,375 |

| 3 | $837,700 | $1,933,200 |

| 4 | $1,041,125 | $2,402,625 |

Standard FHA loan limits are typically lower than those for conventional loans, but the two programs may have matching limits in high-cost areas. Check your local loan limits on HUD’s website, then compare those numbers with conventional loan limits at Fannie Mae’s map tool.

Compare these maxes to the new 2026 loan limits for conventional conforming loans, which have risen to $832,750 in most parts of the country, up from $806,500 in 2025. In high-cost areas, the limit increased from $1,209,750 to $1,249,125.

“FHA loans can be more beneficial for buyers in expensive areas, especially if you are a first-time purchaser,” Boonzayer says.

Documentation

Prepare to gather the necessary paperwork to qualify for an FHA loan, including:

Driver’s license

Social Security card

W-2 and 1099 forms from the past two years

Pay stubs for the last two months

Tax returns for the last two years

Self-employed tax returns and year-to-date profit & loss statements for the past two years (for self-employed applicants)

Complete bank statements for all accounts for the past three months

Recent statements for retirement and investment accounts

Recent billing statements showing account numbers and minimum payments

Recent utility bills and other payment history if no credit score

Bankruptcy discharge documents (if applicable)

“Expect a lengthier application process for an FHA loan, with more documentation required around income, assets, and credit in particular,” Lokeanuth cautions.

Foreclosure & Bankruptcy Waiting Periods

If you’ve experienced a foreclosure, you’ll likely need to wait three years before you can apply for an FHA loan, which is actually much shorter than the seven years a conventional loan requires you to sit on the sidelines.

“If you’ve gone through bankruptcy, the waiting period is two years after a Chapter 7 discharge versus one year of consistent payments, with court approval, under a Chapter 13 plan – which is shorter than conventional loan requirements,” says Holman.

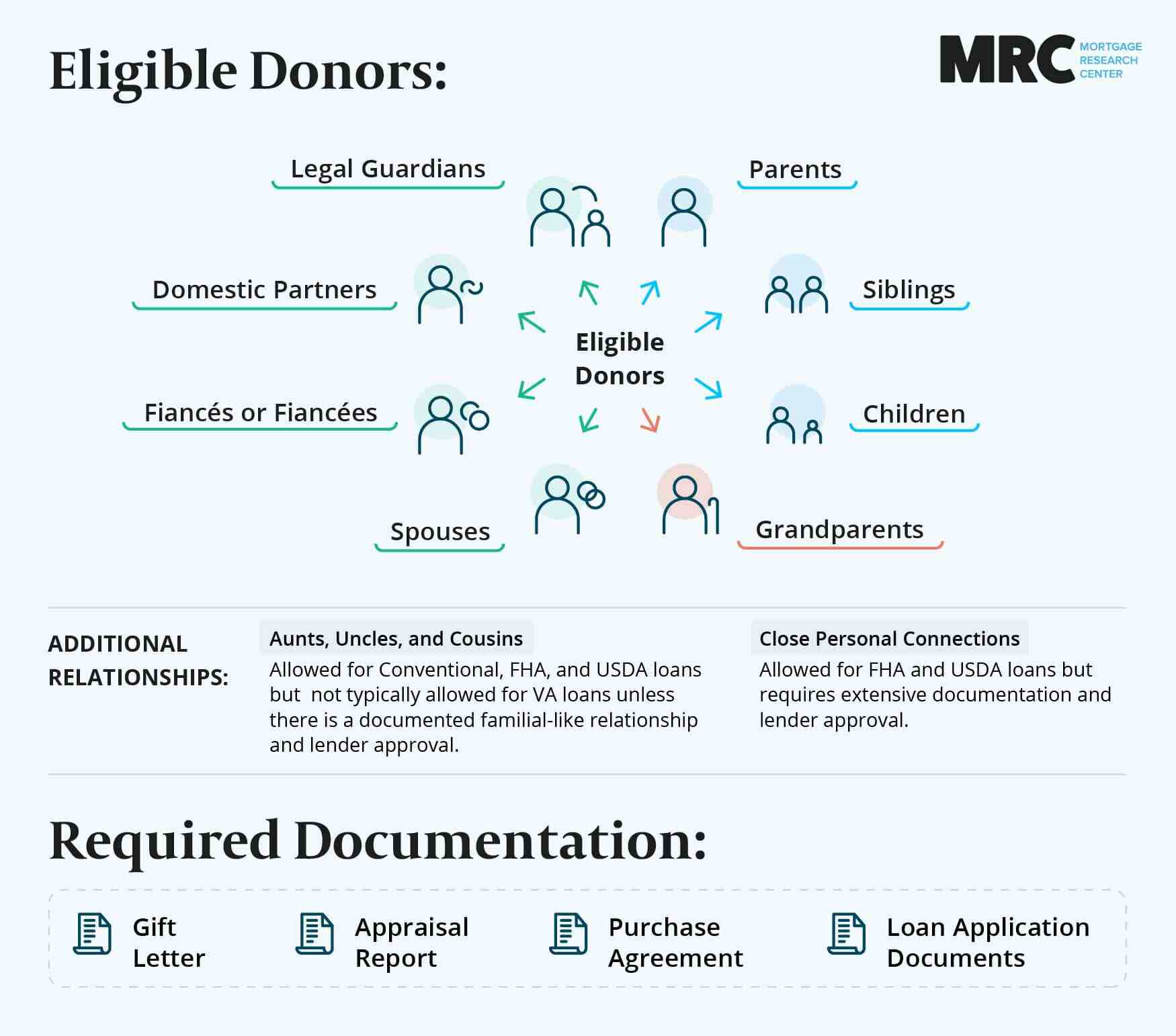

Gift Funds & Gifts of Equity

FHA financing permits you to use gift funds to cover your down payment or closing costs.

“The monetary gift can come from family, friends, charitable organizations, or even an employer. But you will need a letter from the donor explaining that it’s a gift and not a loan,” adds Boonzayer.

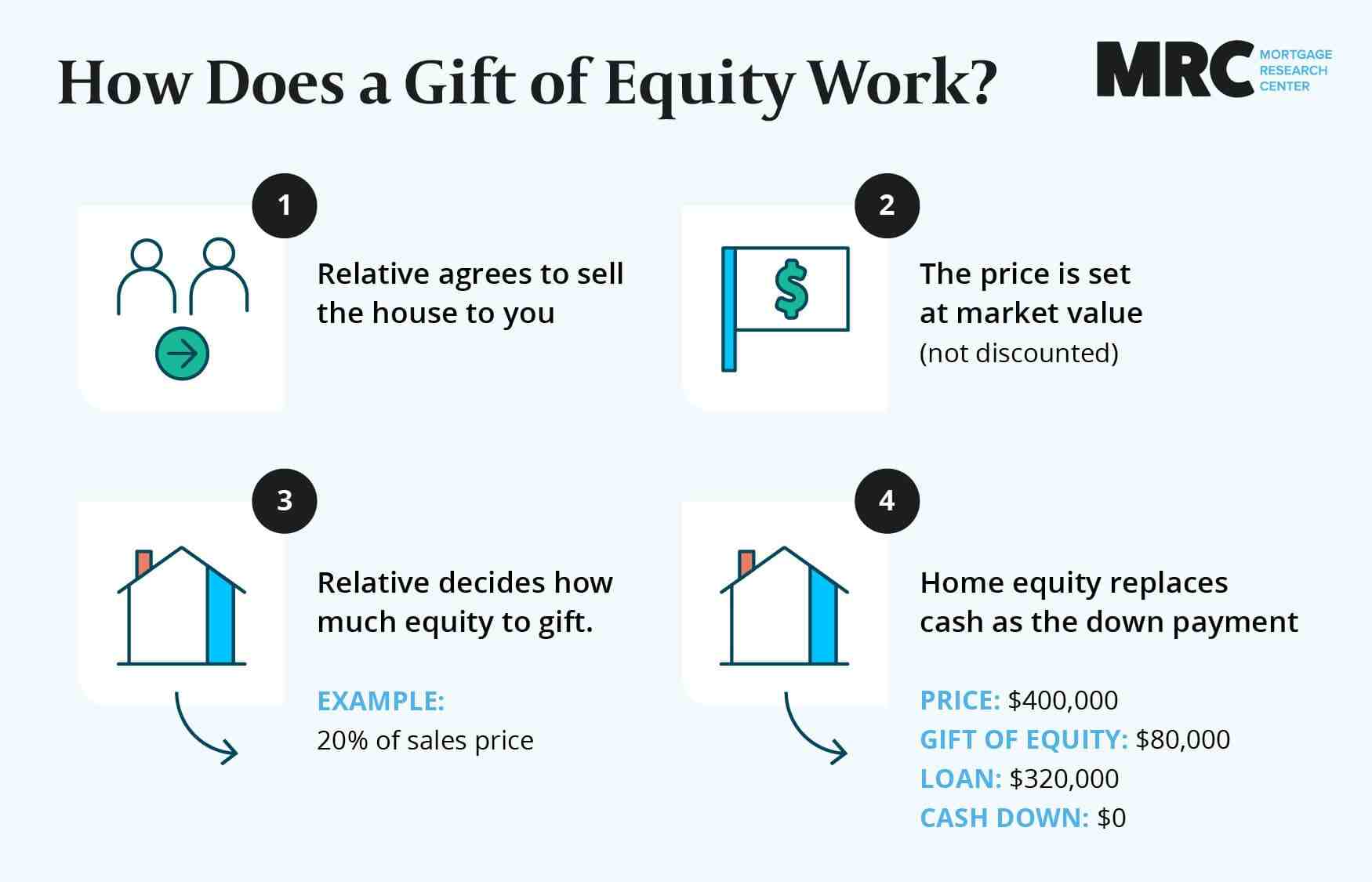

FHA loans also allow gifts of equity, where the seller contributes equity instead of cash – but the same rules apply and the equity must be documented via an appraisal.

Projected Rental Income for Multifamily Homes

If you seek to purchase a two- to four-unit multifamily property using an FHA loan, you can use the projected rental income from the other units to help qualify for the mortgage, so long as you occupy one of the units as your primary residence. This is a smart way to generate income and assist with your monthly mortgage payments.

“However, the income must be verified through an appraisal, which includes a rental schedule, and only 75% of the projected rent is typically counted toward qualifying income,” Boonzayer notes.

FHA Loans: Making Homeownership Possible

Truth is, FHA loan requirements are often more relaxed than the rules around conventional mortgage financing, making this loan a valuable and preferable option, especially if you wouldn’t otherwise qualify for a conventional loan.

“Overall, the FHA program is an excellent choice for first-time and low- to moderate-income buyers who may not be eligible for other financing types,” Lokenauth says. “The flexible credit, down payment, and DTI requirements in particular make FHA loans highly accessible. Just be prepared for the additional paperwork and mortgage insurance requirements.”

Boonzayer agrees, but notes that, while FHA loans remain a great option for many borrower candidates, it’s worth considering alternative choices, too. Case in point: If you are a veteran, active duty military member, or surviving spouse, you may qualify for a VA loan that requires no down payment or mortgage insurance; or if you don’t mind living in a designated rural area, you may be eligible for a USDA loan for which no down payment is needed.

“If you don’t qualify for those loans, or if you can afford a larger down payment or have a higher credit score, a conventional loan might offer you a better interest rate and help you avoid the mortgage insurance requirement,” Boonzayer says. “Trusted mortgage professional to find the best fit for your situation.”