FHA Loan for Mobile Home: How It Works and How to Qualify

If you’re looking for an affordable option beyond a traditional site-built home, an FHA loan on a manufactured home could be the key to achieving your homeownership dreams.

Purchasing a mobile home can be an affordable path to homeownership, but finding financing can sometimes be challenging.

Fortunately, an FHA loan for mobile homes provides an option with low down payments and flexible credit requirements. However, financing a mobile home differs from purchasing a traditional house, and understanding these differences is crucial.

Can You Get an FHA Loan for a Mobile Home?

The short answer is yes, but there are specific conditions.

“FHA can be used to purchase a mobile home, but the criteria for the home is more restrictive.”

FHA loans can finance not only the mobile home itself, but also the land it sits on. There are two primary FHA loan programs that apply to mobile homes: the FHA Title I Loan and the FHA Title II Loan.

FHA Title I Loan is designed for purchasing a mobile home without buying the land. This loan is ideal for those planning to place their home in a mobile home park, on leased land, or on land you already own.

FHA Title II Loan covers both the mobile home and the land it sits on, making it suitable for buyers who want to own the home and land together. This option requires the home to be placed on a permanent foundation.

These loan programs provide more opportunities for homebuyers who may not qualify for conventional financing.

FHA Mobile Home Loan Requirements

To qualify for an FHA loan, mortgage borrowers must meet specific criteria.

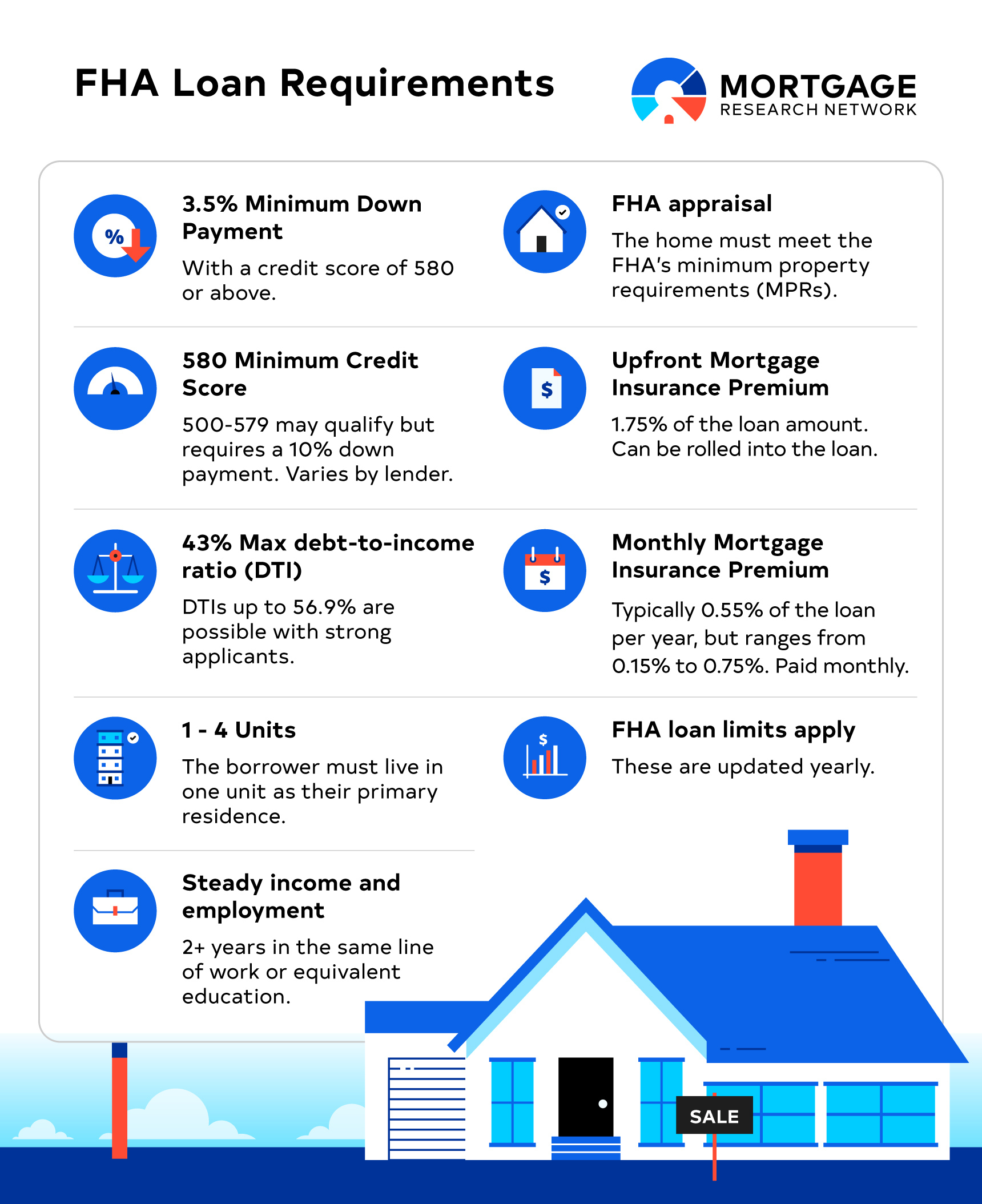

Credit score: The minimum credit score required for an FHA loan is 500. However, if your credit score falls between 500 to 579, you’ll need a 10% down payment. If your score is 580 or higher, the down payment required is just 3.5% down.

Occupancy requirements: You must plan to use the home as a primary residence.

Property requirements: Mobile homes must also be built after June 15, 1976, as homes manufactured before that date do not qualify for FHA financing. Additionally, the property must meet the Federal Manufactured Home Construction and Safety Standards (HUD Code).

Vehicle title elimination: For FHA loans covering the home and land (Title II), the home’s vehicle title must be eliminated and the home must be classified as real estate.

Foundation requirements: For Title II loans, being placed on a permanent foundation.

Site requirements: The site must have adequate water supply and sewage disposal facilities, and must meet all local zoning and land use requirements.

Home size: The manufactured home must be at least 400 square feet.

HUD tag: The home must have the HUD Certification Label (HUD tag) visible on the exterior.

Data plate: An information sheet found on the interior of the home detailing the serial number, model, date of manufacture, and thermal zone maps.

FHA loans also require an annual Mortgage Insurance Premium (MIP) ranging from 0.15% to 0.75% of the loan amount. This cost is divided into 12 monthly installments and added to the borrower’s mortgage payment. The exact MIP rate depends on the down payment and loan terms—for example, a 3.5% down FHA loan typically has a 0.55% MIP rate.

Manufactured vs Mobile home: Is There a Difference?

HUD acknowledges that manufactured homes are often called mobile homes, and while the terms are used interchangeably, “manufactured home” is the more modern and accurate term.

Additionally, to qualify for an FHA loan, the home must meet HUD’s definition of manufactured housing. This requires compliance with the Manufactured Home Construction and Safety Standards (MHCSS) and a red certification label confirming its HUD-approved status.

FHA Loan Limits for Mobile Homes

FHA loan limits depend on whether the loan covers only the mobile home or both the home and land. These limits are adjusted yearly and vary by location based on market trends.

FHA Title I Loan Limits (2025)

Single-wide mobile home: Up to $105,532

Double-wide mobile home: Up to $193,719

Single-wide mobile home with land: Up to $148,909

Double-wide mobile home with land: Up to $237,096

Lot-only financing: Up to $43,377

FHA Title II Loan Limits (2025)

Home and land combined: Up to $524,225 (varies by county)

FHA Title I vs. Title II Loans: Key Differences

Feature | FHA Title I Loan | FHA Title II Loan |

Includes | Mobile home only (no land) | Mobile home + land |

Down Payment | Typically 5% or more | 3.5% (580+ credit score) |

Foundation Requirement | Not required | Must be on a permanent foundation |

Loan Term | 20 years (single-wide), 25 years (double-wide) | 30-year fixed options |

Interest Rates | Higher than Title II loans | Lower, similar to traditional home loans |

Pros and Cons of FHA Loans for Mobile Homes

While FHA loans make mobile homeownership more accessible, they come with both advantages and limitations.

Pros:

Low down payment requirement, sometimes as little as 3.5%, making them ideal for first-time buyers.

Lenient credit requirements, providing opportunities for those who might not qualify for a conventional loan.

These loans are government-backed; lenders are more willing to approve applicants.

Cons:

FHA loan limits may not be sufficient for expensive mobile homes or those located in high-cost areas.

Property must meet strict HUD safety standards and, in the case of Title II loans, be placed on a permanent foundation, limiting flexibility.

FHA loans require mortgage insurance, increasing monthly costs for mortgage borrowers.

How to Apply for an FHA Loan for a Mobile Home

If you’re thinking about buying a manufactured home with an FHA loan, here are the steps involved:

Check your credit: Review your credit score and financial situation to ensure you meet the lender's requirements.

Determine your loan type: Decide whether you need a Title I loan (for the home only) or a Title II loan (for both the home and land).

Find an FHA-approved lender: Not all lenders offer FHA loans for mobile homes, so research and compare options.

Get pre-approved: This will give you an estimate of how much you can borrow and help you shop with confidence.

Choose a HUD-approved mobile home: Ensure the home meets FHA eligibility criteria, including the HUD certification tag.

Submit your loan application: Provide financial documents, employment history, and property details to your lender.

Close on your loan: Once fully approved, finalize the process and take ownership of your new home.

Financing a Manufactured Home on Leased Land

FHA allows financing for homes on leased land, for instance, within a mobile home park.

The borrower must supply documentation proving:

The lease term is three years or longer.

The lease is renewable for a minimum of one-year terms.

The site owner must supply the lessee with notice of termination at least 180 days prior to non-renewal of the lease due to closure of the community.

FHA vs. Other Mobile Home Loan Options

Loan Type | FHA Loan | Chattel Loan | VA Loan (for Veterans) | USDA Loan |

Down Payment | 3.5%-10% | 5%-20% | 0% | 0% |

Credit Score | 500+ | 600+ | 580+ | 640+ |

Covers Land? | Title II only | No | Yes | Yes |

Loan Term | 20-30 years | 10-20 years | 30 years | 30 years |

Best For | First-time buyers | Buyers with bad credit | Veterans & active military | Rural homebuyers |

Common Myths About FHA Mobile Home Loans

There are many misconceptions about FHA loans. This is even more so when it comes to using FHA financing to purchase a mobile home.

Some believe that FHA loans are only for traditional houses. However, FHA loans are also a great option for financing mobile homes.

Others think you need a perfect credit score. The reality is that FHA loans accept scores as low as 500.

Some assume mobile homes don’t qualify for government-backed loans. But, FHA, VA, and USDA loans all provide financing options for mobile homes.

Related: Buying a manufactured home with a USDA loan

Should You Use an FHA Loan to Buy a Mobile Home?

FHA loans are an excellent choice for buyers with limited down payment savings and lower credit scores who want the security of a government-backed mortgage.

However, they may not be ideal for those who want to place their home on non-permanent land or avoid mortgage insurance costs.

The Bottom Line on FHA Loans for Manufactured Homes

FHA loans provide an accessible pathway to mobile homeownership, but navigating the requirements and loan options can be complex. Whether you're looking for financing that’s just for the home, or both the home and land, speaking to a lender can cut out a lot of confusion.

A knowledgeable professional can help guide you through the application process, clarify any concerns, and help you secure the best loan terms for your mobile home financing needs.