FHA High-Balance ‘Jumbo’ Loans

Technically, FHA Jumbo Loans don’t exist, but some buyers can still finance high-value homes with FHA loans. For buyers living in cities where home prices have skyrocketed, FHA high-balance loans can serve the purpose of an FHA Jumbo loan.

Homebuyers in low- and medium-cost areas may never need to borrow the maximum FHA loan, which now exceeds $500,000.

Other buyers aren’t so lucky. For example, in larger cities, especially coastal metro areas, buyers can’t find any homes to buy under half a million dollars. Their area's median home price easily outpaces the FHA’s standard loan limit.

This could render FHA loans useless in these places, taking a powerful borrowing tool off the table.

To solve this problem, the FHA allows high-balance loans – also known as “FHA jumbo loans” – which raise the loan program’s borrowing ceiling to reflect local market conditions.

Is There Such Thing as an FHA Jumbo Loan?

Some people call FHA high-balance loans “FHA Jumbo Loans” since they resemble the Jumbo alternatives to conventional loans. Technically, though, FHA Jumbo loans don’t exist. Buyers who need one should ask about an FHA high-balance loan instead.

For example, a buyer in Seattle who wants to use the FHA loan program — which can allow low down payments despite average credit scores and higher debt ratios — would likely need an FHA high-balance loan.

Seattle's median prices have topped $750,000, exceeding the standard FHA loan limit by more than $200,000. In response, the FHA has raised its borrowing limit to over $1 million, reopening the loan program to average shoppers.

How FHA High-Balance Loans Compare to Jumbo Loans

Like FHA loans, conventional loans, regulated by Fannie Mae and Freddie Mac, have loan limits. In 2025, the maximum loan size for most conventional borrowers is $806,500 versus $524,225 for FHA.

Conventional borrowers who need to exceed their area’s loan limit can apply for Jumbo loans.

“Jumbo loans are a lot more flexible than FHA high-balance loans which have a very specific limit per county,” said Adam Spigelman, senior vice president at Planet Home Lending.

But this flexibility can cost more. Compared to FHA high-balance loans, Jumbo loans rely more on the home buyer’s financial stability for approval, making Jumbo loan approval more difficult.

For example, Jumbo loan borrowers need to put down more money — maybe even 20 percent — down on their home.

Also, borrowers may need enough money in savings to make the loan’s payment for six months, or a year, if necessary. Credit score and debt-to-income ratio (DTI) thresholds may be higher, too.

Typical borrowers have higher approval odds with FHA high-balance loans.

FHA Loan Size & County Loan Limits

How high can a high-balance FHA lender go? It depends on the county and the type of residence being financed.

Most people buy single-family, or 1-unit, properties, but the FHA allows 2-, 3-, and 4-unit properties if the buyer plans to live in one of the units. Loan limits go higher on multi-unit properties.

The FHA bases its maximum loan sizes on median home prices. Here are some of the FHA’s loan limits in 2025:

Single-family home | 2-unit | 3-unit | 4-unit | |

Standard limit (floor) | $524,225 | $671,200 | $811,275 | $1,008,300 |

Raleigh, N.C. | $530,150 | $678,700 | $820,350 | $1,019,550 |

Atlanta | $688,850 | $881,850 | $1,065,950 | $1,324,750 |

Denver | $833,750 | $1,067,350 | $1,290,200 | $1,603,400 |

Boston | $914,250 | $1,170,400 | $1,414,750 | $1,758,200 |

Seattle | $1,037,300 | $1,327,950 | $1,605,200 | $1,994,850 |

New York City and Los Angeles | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

Highest limit (ceiling)* | $1,814,625 | $2,323,450 | $2,808.325 | $3,490,300 |

*Highest limit available only in Alaska, Hawaii, Guam, and the U.S. Virgin Islands.

Search the FHA’s database to find your county’s loan limit.

What If You Need a Loan Larger Than FHA Allows?

Borrowers who need more than their local FHA loan limit allows should check other loan types, especially conventional loans. Standard conventional loan sizes go higher than standard FHA loan limits.

In 2025, standard-sized loans can reach:

$524,225 for single-family FHA loans

$806,500 for single-family conventional loans

That said, in higher value areas, limits for FHA and conventional loans tend to line up. For example, in places like Boston, Seattle, New York, and Los Angeles, the limits for both loan types are the same.

Because of this, conventional borrowers in these areas would need a Jumbo loan to exceed the borrowing power of an FHA high-balance loan.

FHA High-Balance Loan Requirements

Here are some benchmarks for FHA high-balance loan eligibility:

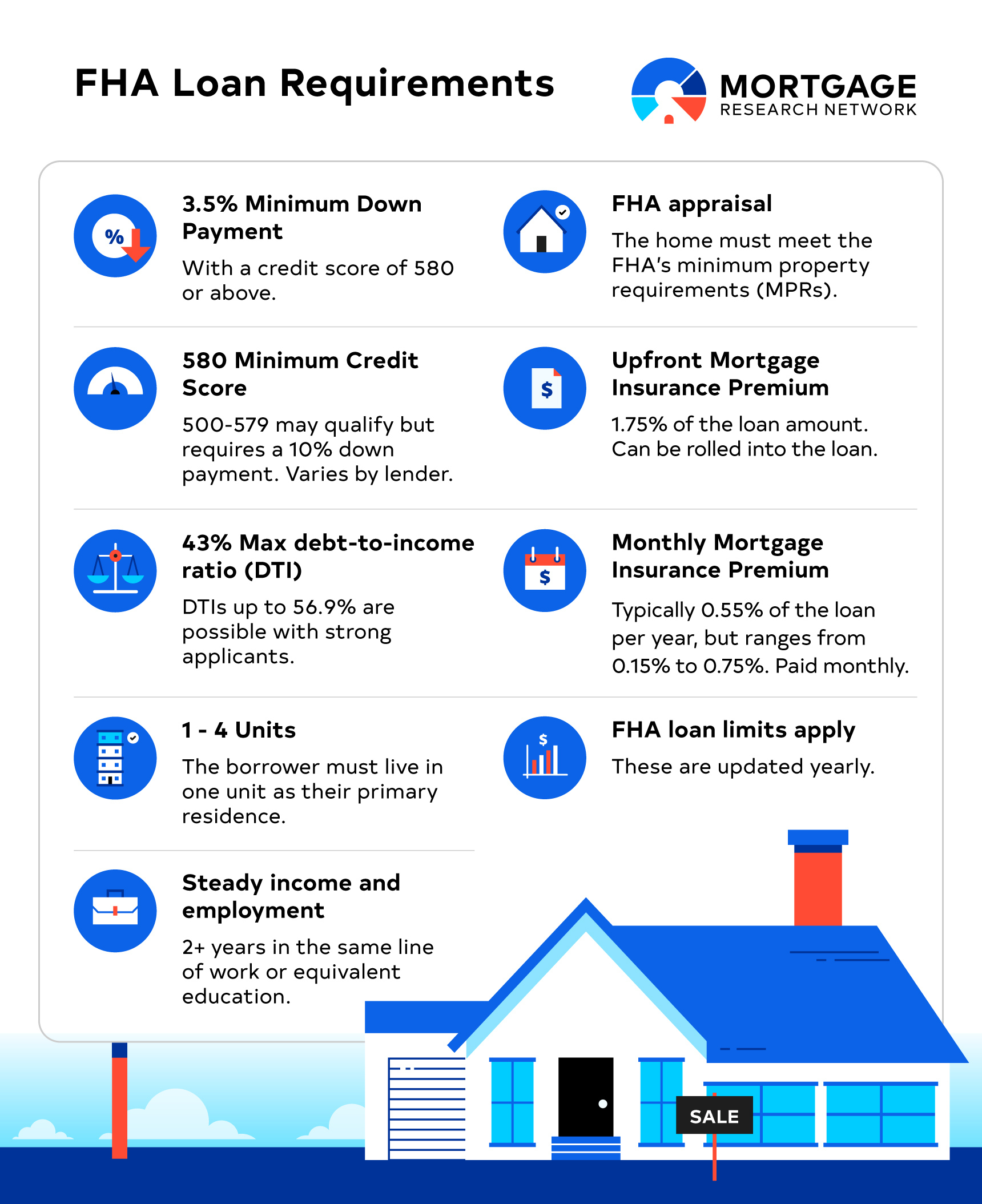

Down payment: Borrowers must put at least 3.5 percent down. For a $800,000 home, 3.5 percent equals $28,000 down

Credit score: To get a 3.5 percent down loan, borrowers need a FICO score of at least 580. Borrowers with scores between 500 and 579 may still get approved by some lenders but with 10 percent down ($80,000 on a $800,000 home)

DTI: Debt-to-income ratio, or DTI, should not exceed 45 percent. This ratio measures how much the buyer can afford to pay for housing based on how much the buyer owes on other debts. Lenders might accept higher DTIs when the borrower shows other strengths, like a large savings account balance, for example

Living in the home: FHA loans, including high-balance loans, finance only primary residences and not investment properties or vacation homes. Multi-unit homes are OK if the borrower plans to live in one of the units

Additionally, FHA borrowers must pay the FHA’s mortgage insurance fees which help sustain this loan program. Borrowers pay these fees in two ways:

Upfront MIP: The FHA’s upfront mortgage insurance premium adds 1.75 percent to the loan amount for most 30-year borrowers. For a $800,000 loan, that’s $14,000 extra tacked on

Annual MIP: This insurance premium varies in size based on the loan’s down payment amount and the loan’s term. Borrowers who put the minimum 3.5 percent down on a 30-year loan usually pay 0.55 percent extra a year, divided into 12 monthly installments. This fee decreases as the loan balance decreases

Loans with higher balances generate higher MIP fees. Still, FHA loans can still save money for borrowers who need their relaxed qualifying rules.

Check out our full guide to FHA loan requirements to learn more.

How These Compare to Conventional Loans

FHA loans include insurance for lenders, protecting them from losing money if the borrower were to stop making payments.

Conventional lenders depend more on the borrower for this security. That’s one reason conventional loans require a higher credit score, generally 620 or higher, and a lower debt ratio of 36 percent or so.

Even when they meet these minimum requirements, conventional borrowers may need to put down more money — 5 to 10 percent, for example — to get a mortgage rate that competes with the same borrower’s rate on an FHA loan and its 3.5 percent down payment.

Conventional borrowers who pay less than 20 percent down will also need to buy aprivate mortgage insurance (PMI) policy to insure the lender. Higher-balance conventional loans may need larger PMI premiums, which can reach 1.5 percent of the loan amount per year.

How FHA High-Balance Loans Compare to Jumbo Loans

Standard jumbo loans require near-perfect finances for approval. These loans exceed Fannie Mae and Freddie Mac’s loan limits, so lenders shoulder a Jumbo loan’s risk alone.

These loans come from private banks which create their own, often strict rules for approval.

Jumbo loan borrowers may need to show they have enough money saved to make the loan’s payment for a year or two and make large payments, maybe up to 25 percent.

Compared to an FHA high-balance loan, with its built-in protections for the lender, Jumbo loans are tough to qualify for and too expensive for many borrowers.

Should You Get an FHA High-Balance Loan?

Buyers in higher value areas should check out their area’s FHA loan limit before applying for a conventional or Jumbo loan.

For some borrowers, especially buyers who have average credit and limited money for a down payment, an FHA loan’s mortgage insurance fee can pay for itself in the form of a lower rate.

The best way to find out for sure: Get Loan Estimates from lenders to compare costs side by side. Or do your own calculations with anFHA loan calculator.