FHA Gift Funds: Guidelines and Eligible Donors

You can receive FHA gift funds from family, and, in some cases, close friends for whom you can document a long-time relationship.

Can a friend or family member help make your FHA loan’s down payment? Yes, the FHA will allow this.

But FHA lenders will follow the FHA’s gift fund guidelines. Understanding these rules before you apply for a mortgage could help avoid delays and keep your home purchase on track.

Eligibility Criteria for FHA Gift Funds

FHA-insured loans require at least 3.5 percent down for most buyers. That means for every $100,000 in the home’s purchase price, $3,500 must be paid upfront. For example, a $300,000 home would require $10,500 down.

This entire down payment can come from money someone gave you if the donation adheres to the FHA’s rules and comes from an acceptable donor.

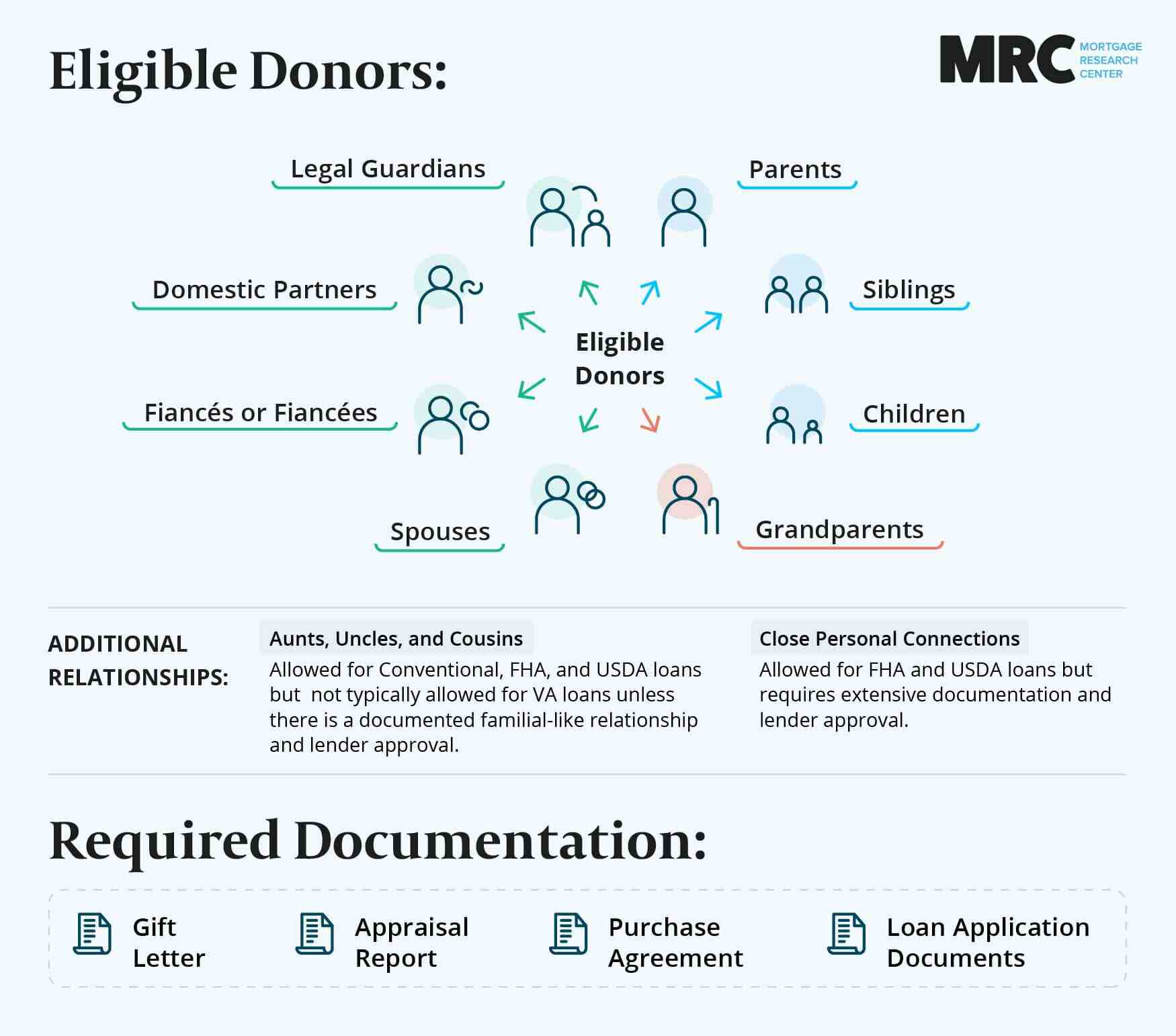

Acceptable Donors for Gift Funds

The FHA defines an “acceptable donors” as:

Members of the borrower’s family

The borrower’s employer or labor union

A close friend who can document their long-standing relationship with the borrower

A non-profit or charitable organization

A government agency that provides down payment assistance

Large gifts from someone who doesn’t fit one of these categories won’t qualify under FHA gift fund guidelines.

Differences Between Gift Funds and Loans

From the lender’s point of view, down payment loans and down payment gifts are not the same thing.

Down payment loans add to the borrower’s debt, and debt affects mortgage eligibility. For example, $300 a month to repay a down payment loan increases your debt-to-income ratio, or DTI. FHA imposes certain DTI caps, so all debts must be accounted for.

A down payment loan could mean getting approved for a smaller mortgage. And for some borrowers, a smaller mortgage could put the house they’d planned to buy out of reach.

Down Payment Loans Are Good, But Gifts Are Better

This doesn’t mean FHA loans never allow down payment loans. Secondary loans are allowed in the form of FHA down payment assistance. They just need to know the true source of the down payment funds.

When a borrower uses a down payment loan — a personal loan, or a loan provided by a local down payment assistance program, for example — the lender will need to factor that loan’s payment into the borrower’s overall mortgage eligibility.

Yes, loans can limit borrowing power, but at the same time, the loan is allowing home buying to begin with. So it’s still a win. A true gift can make home buying possible without cutting into borrowing power.

Some down payment assistance loans offer a compromise: They require no payment as long as the buyer stays in the home for a set amount of time: Five years, for example. This type of forgivable loan can have a smaller impact on mortgage eligibility.

Required Documentation for FHA Gift Funds

Down payment gifts can be loans in disguise, so lenders will need documents to show the money comes from a gift and not a loan.

This means the donor will need to submit some paperwork, specifically a “gift letter” and a way to show how the money traveled from the donor’s bank account to the home buyer’s bank account.

Gift Letters Explained

In a gift letter, written from the donor to the lender, the donor must state that the down payment gift comes with no requirement of repayment either now or in the future. A donor should also state the gift in no way entitles the donor to partial ownership of the home.

The FHA gift letter should also include:

The donor’s name and relationship to the borrower

The amount of the gift

The source of the funds, including the account number

The purpose of the gift (down payment or closing costs, for example)

The address of the home the borrower is buying (assuming there is already a purchase contract in place)

A gift that’s been in the borrower’s bank account for more than 60 days may not require a gift letter. Since FHA lenders usually check the borrower’s bank statements for two months, the money could already be “seasoned.”

Proof of Funds

Along with the gift letter, the lender will need to know how the money got from the donor’s account to the borrower’s account. This can be accomplished by submitting a canceled check and deposit slip. The check shows how the money left the donor’s account; the deposit slip shows how the same money arrived in the borrower’s account.

Proof of wire transfer between the two accounts can also work, as can transfer confirmation directly from the donor to the escrow company. In fact, the latter method can save some paperwork since it skips your bank account altogether.

Lenders may also ask for copies of the donor’s bank statement to make sure the donor can afford to provide the down payment gift.

Conditions for Using Gift Funds

FHA gift funds can go toward the loan’s down payment or toward the loan’s closing costs.

Down Payment Applications

Borrowers with credit scores of 580 or higher must put at least 3.5 percent down.

The entire down payment can come from gifted funds, or the borrower can apply part of the gift to the down payment and part to closing costs.

Closing Cost Applications

Typical buyers pay most of a home’s closing costs. Closing costs pay legal fees, lending fees, the FHA’s upfront mortgage insurance premium (MIP), and other professional services required to finalize the loan and register the sale.

In total, closing costs usually range between 3 and 6 percent of a home’s purchase price. For a $300,000 home that’s $9,000 to $18,000. Approved FHA gift funds can cover some, or all, of these costs.

No Down Payment Gift Limits

The donor can’t be a party to the transaction, like a seller or builder. Because the donor does not have a financial interest in the sale, there are no limits to the amount they can give.

3 Common Mistakes to Avoid

Avoid these common mistakes with your gifted down payment:

1. Using Ineligible Donors

Not everyone you know can contribute to your FHA down payment. Ineligible donors include:

The home’s current owner (the seller)

The home’s builder (with new construction)

Your real estate agent or the seller’s agent

The closing agent or closing attorney

Friends who can’t document their connection

In short, a person or business that profits from your loan can’t provide down payment money. The lender will veto this gift source. Acquaintances or co-workers can’t provide down payment money because these types of gifts are more likely to be loans in disguise.

Interested parties such as the seller, builder, agents, and others, can give a maximum of 6% of the purchase price when using an FHA loan, and these funds can only be used for closing costs, not the down payment.

2. Providing Incomplete Documentation

Improper documentation often happens by accident. For example, the gift letter may inadvertently omit the gift amount or state an amount that doesn’t match the actual gift amount. This will need to be fixed.

Using Venmo, CashApp, Zelle, or other similar apps to transfer money can prevent proper sourcing of the funds. Unless the lender says otherwise, ask your donor for an old-fashioned check, electronic funds transfer (EFT), or wire transfer.

3. Forgetting to Tell the Lender About the Gift

Be sure to tell the lender that the gifted money will help you make the down payment or pay closing costs. Surprising the lender with this information in the middle of the underwriting process could delay loan approval.

Telling the lender about the gift can also make documentation easier. For example, the lender may provide a template that makes the letter easier to write.

Strategies for Effectively Using FHA Gift Funds

FHA gift funds will go farther when:

The Buyer Has a FICO Score of 580 or Higher

A FICO of 580 or higher lets the buyer put only 3.5 percent down on an FHA loan. If a relative agreed to give $20,000 toward a $300,000 home, the buyer could put $10,500 of the money down, leaving the other $9,500 for closing costs.

With a score between 500 and 579, FHA would require 10 percent down, or $30,000, down. The same $20,000 gift wouldn’t cover this down payment, leaving the buyer to seek other sources of money or to buy a less expensive home.

Working to prepare your credit score for home buying could pay off a lot.

The Buyer Combines Gifted Money With Other Sources

In most communities, local government programs and not-for-profit agencies can help buyers make down payments. Some employers provide matching funds for down payments, too.

Combining one of these sources with gifted money from a friend or family member helps borrowers stretch funds further. For example, a gift from a relative could cover the down payment while a grant from a non-profit could cover closing costs.

This could require some planning. Some grant programs, for example, might require borrowers to contribute at least some money from their own savings to qualify for the grant.

The Gift Doesn’t Artificially Inflate the Buyer’s Price Range

Ordinarily, the underwriting process protects borrowers from buying a home they can’t afford, but the process isn’t foolproof. It’s possible for a large monetary gift to open the door to a house payment that will strain your monthly budget, creating more financial strain in the future.

The best gifts relieve financial pressure instead of creating more strain. Be sure to review the Loan Estimate to make sure the loan’s required monthly payment remains in your comfort zone.

Exploring Related FHA Loan Requirements

Here are some important FHA loan requirements to keep in mind.

Credit Score Standards

To approve an FHA loan, lenders typically require a FICO score of 580 and a debt-to-income ratio below 50 percent. Borrowers with credit scores between 500 and 579 can still qualify with some lenders, but these borrowers pay at least 10 percent down.

The FHA loan program exists to lower home buying barriers for borrowers who struggle to afford a conventional loan. But borrowers who have excellent credit — think 720 or higher — may find more savings with a conventional loan, especially if their gift funds help them put 20 percent down.

Property Requirements

FHA loans finance only primary residences. They won’t finance vacation homes or investment properties, although FHA borrowers can finance a duplex — or even a 3- or 4-unit complex — as long as they live in one of the units.

Residences must also pass the FHA’s inspection for safety and accessibility.

FHA Loan Limits

Check local FHA loan limits prior to making an offer on a home. The FHA allows bigger loans in markets with higher home values, including major urban areas or coastal resort areas.

Gift Funds Can Speed Up Home Buying

Saving up the down payment can delay home buying, sometimes by years, making it seem like you’ll ever escape paying rent. And while you’re trying to save, house prices (and rents) may keep rising.

An FHA-approved down payment gift could short circuit this cycle. Combined with the FHA’s low down payment minimum, a down payment gift can become an investment in your financial stability.