The Fed Cuts 0.25% But Mortgage Rates Rise Anyway

The Federal Reserve cut its key interest rate by 0.25% to a range of 4.25%-4.5%. The move was highly expected by the market.

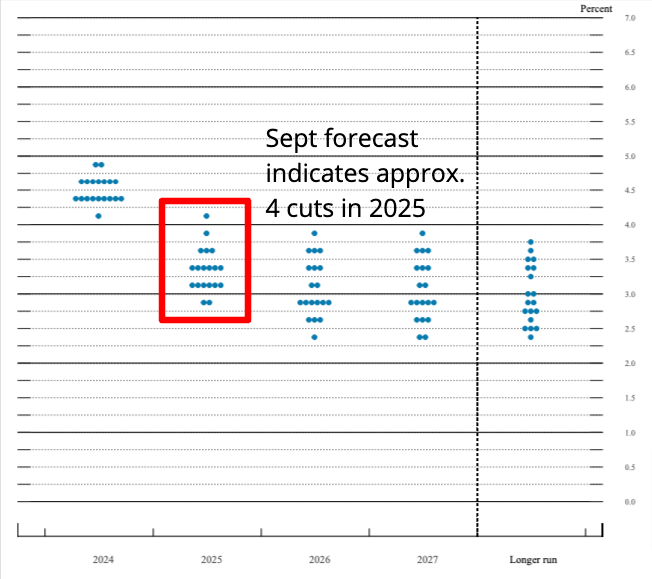

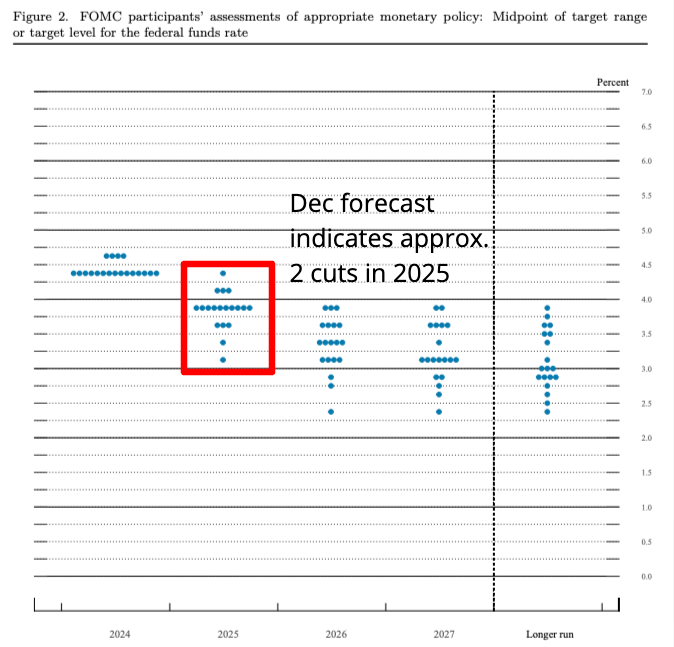

What wasn’t expected was that the Fed forecasted only two additional cuts in 2025, down from four predicted in September.

Mortgage rates took a beating shortly after the announcement and are now at the highest levels since early November, says Mortgage News Daily.

Before that, you have to go back to July to find a higher 30-year fixed rate. What's going on?

The Fed’s Big 2025 Shift

But the main event was the Fed’s forecast published today.

The document showed a severe departure from the September forecast, which indicated four 0.25% rate cuts in 2025 in addition to today's cut. Now it predicts just two cuts next year.

The CME FedWatch tool predicts no cut at the Fed’s January meeting and a roughly 50/50 chance of a 0.25% cut in March, but those odds could worsen.

What It Means for Mortgage Rates and Housing

Mortgage rates are on the rise despite today’s rate cut.

Markets already expected today’s cut. It was "baked into" rates. Now, markets are adjusting to the new reality of two more cuts in all of 2025 rather than four.

In large part, four Fed cuts in 2025 were priced into mortgage rates prior to today. Now, investors must backtrack and remove two cuts from their expectations.

Mortgage News Daily says today's fallout equates to a 30-year fixed mortgage rate that is 0.21% higher in one day. It estimates the average lender will issue a rate of about 7.13% after today's rout.

This is adding insult to injury, as rates have been on an upward climb since early October.

According to Freddie Mac, the average 30-year fixed mortgage rate fell to 6.08% in September.

The improvement was based on stellar inflation readings, which spurred hope for continued Fed rate cuts. Remember that falling inflation is necessary for easier Fed policy and low mortgage rates.

The Personal Consumption Expenditures is the Fed’s favorite inflation tracking measure. The core reading, which excludes food and energy, showed inflation ticking up just 2.6% to 2.7% per year from May to September, down from 3% at the start of the year.

The Fed’s target for inflation is 2% annually.

In October, inflation rose 0.6% in a single month, and annual inflation ticked up to 2.8%, signaling possible lost ground in the inflation fight.

This no doubt played a hand in today's Fed forecast.

Trump Trade

As if inflation worries weren’t enough, the Trump Trade began in October, as chances rose for a second term. “Trump Trade” is a term denoting markets’ tendency to expect stronger economic results and inflationary factors under his administration.

Donald Trump, while promising low rates during his presidency, embraces policies that may induce inflation, and therefore higher mortgage rates.

A few examples are

Tariffs, which drive up consumer prices

Immigration reform, which could drive up the cost of labor

Tax cuts that could lead to more hiring and higher wages, and therefore rising prices for goods and services

After the election, mortgage rates peaked again, but have since started to fall, now at a 6.6% average, says Freddie Mac.

It’s hard to say how much Trump’s election affected the 2025 forecast. But with Trump in office, the Fed will be in an even trickier spot: can it continue to cut in 2025 at all if inflationary policy begins in earnest?

What Home Shoppers and Refinancers Should Do Now

It’s likely not the best day to lock a rate, since mortgage rates react immediately to bad news.

Mortgage applicants, though, should get pre-approved as rates potentially drift downward after an initial bump.

It always pays to be prepared in case there’s a short, unexpected window for lower rates.