Family Builds Barndominium For 1/3 the Cost of Stick-Built Home, Says Others Can Do It Too

Above: A digital rendering of the Grahams' eventual Florida barndominium, currently under construction.

When Scott Graham and his family sold their house in Australia and decided to move across the globe to Florida in November, they quickly had sticker shock.

“Real estate here in Florida, just an average three-bedroom house in a good area, you're going to pay $650,000 to $950,000,” Graham says, adding that much of the homes and neighborhoods they saw felt too crowded and overpriced for the space for him, his wife and their three children.

Instead of buying an existing home or a cookie-cutter new build, the Grahams are raising the roof (literally) on a new barndominium. The Grahams bought 20 acres in the middle of a lush, secluded pine forest for about $116,000 in Altha, Florida, about 40 minutes north of Panama City. Construction of their 3,000-square-foot barndo is currently underway.

Unlike stick-built homes, steel-frame barndominiums, or “barndos” for short, are much cheaper, quicker and easier to build. Barndo enthusiasts love the buildings for their raised ceilings, open floor plans, flexible spaces and durability.

Graham says his family’s home costs about $80 per square foot to build with higher-end appliances and finishes. Meanwhile, the average cost to build a new stick home in Florida runs about $150 to $280 per square foot, according to HomeGuide.com.

“These homes are extremely safe,” Graham says. “They're highly energy-efficient; you've got about double the insulation rating that a typical stick frame home would have. It’s very simple to install solar on the roofs of these homes.”

For cost-conscious homebuyers looking for more space to spread out without breaking the bank, barndos offer the best of both worlds, says Graham, adding that he hopes his home will be done in time for Christmas.

Graham has become such a fan of barndominiums that he helped co-found a barndo development firm, Kiva Communities, in Panama City to help bring barndo living to more people who seek alternative housing.

“A [big] reason why we made this decision is for our own family’s security,” says Graham. “Living in the country gives you quite a bit more freedom.”

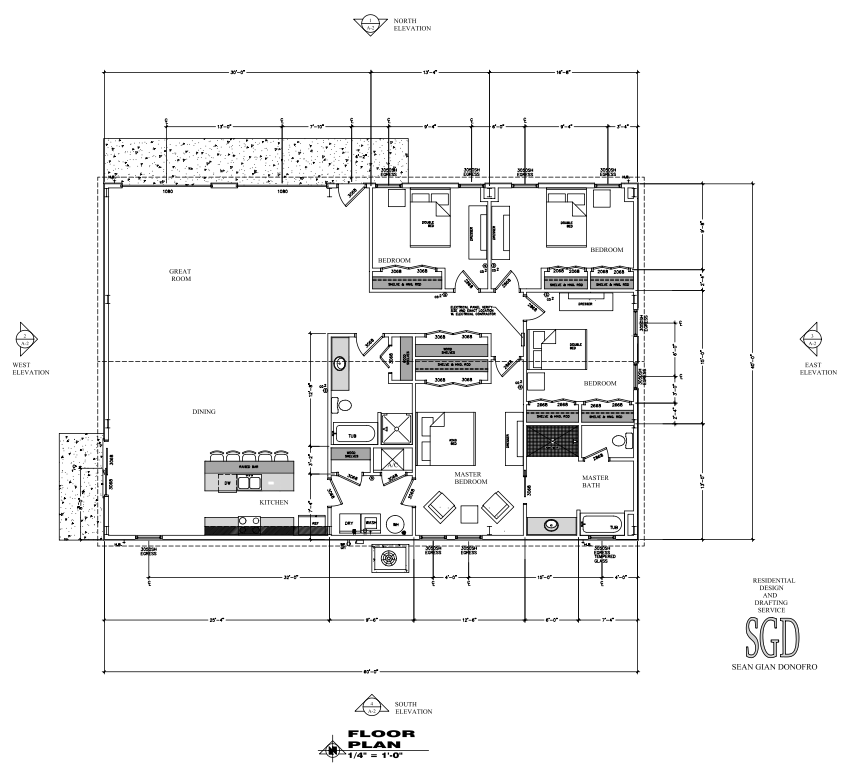

The Graham family barndominium floorplan.

6 Tips On Building A Barndominium

Homebuilders are hopping on the barndo trend, but it’s a relatively small slice of the housing pie. In February, just 7% of single-family builders in the U.S. reported they had built barndominiums in the past year, according to a survey from the National Association of Home Builders.

To ensure your barndo build goes smoothly, here are some tips to consider.

1. Find Reputable Contractors

The most difficult part about building a barndominium is finding experienced, trustworthy contractors, says Graham, adding that he initially dealt with shady contractors who took his money and ran. Start your search online for a reputable barndo builder, including Instagram where there’s a prolific barndo community. Local real estate agents and loan officers might be able to recommend some barndo builders, and you might even find developers building barndo communities in your area.

Other trades you’ll need to involve include an architect or interior designer, a concrete company, an electrician and a plumber. For some loan types, such as VA and FHA loans, you might also be required to get a home inspection during and after construction.

2. Stake Out Your Land

Before raising a single pole, you need the right plot of land. The cost will vary depending on acreage, location and land features. Make sure the land is zoned appropriately to build your barndo, if it’s in a homeowners association that requires prior approval and what permits you’ll need. Also, consider if the land is near utilities (or if you have to install them) and if you need to install septic on the property, which will add to your construction costs.

3. Find a Mortgage Lender Who Understands Barndos

If you’re not paying cash, you’ll need to work with a reputable mortgage lender who understands how barndo construction loans work and how to underwrite them, says Darren Stroud, SVP and branch manager with Go Mortgage in Spartanburg, South Carolina.

Barndominiums aren’t quite mainstream yet, making it hard to find a lender who’s knowledgeable about this home type. That means you might have to shop around.

4. Shop for Homeowners Insurance

A well-built and well-insulated steel barndo is typically wind-rated for up to 165 mph winds, Graham says. Not only does this mean the structures can withstand tough weather conditions, it also makes it more likely to find affordable homeowners insurance. However, you might need to shop around for insurers who offer coverage for barndos. Your mortgage lender might have some suggestions to share.

5. Plan Out Your Space

Barndominiums offer a lot of flexibility in how you set up and use the open space. Consider working with a barndominium architect or designer who can advise you on the best way to orient your living areas and incorporate must-have spaces, such as a home office, an attached garage/storage space or a recreational/play area. Starting with a well-designed floor plan that maximizes your space is crucial, Graham says.

6. Understand the Construction Process, Timeline

Once your land is ready for building, the longest part of the construction process is typically laying the concrete foundation for your barndo, Graham says. After that’s done, next comes framing the shell of your barndo, which is relatively quick, he adds. That’s followed by wiring, plumbing and installing an HVAC system.

One of the final steps is insulation; Graham is using spray foam insulation for his property, which is a popular choice. Finally, you’ll put the finishing touches on your new barndo, including drywall, paint, flooring and installing appliances and cabinetry. Depending on how detailed and big your floor plan is, a barndo can take as little as a few months or up to one year to complete.

How To Finance Your Barndo

Once you find the right lender, it’s not complicated to get approved for a conventional or government-backed mortgage to build or buy an existing barndo—so long as there are one or two comparable homes in your area, Stroud says.

“They're new on the scene so a lot of people are hesitant,” Stroud says, noting that he has had to look for barndo cash deals through local barndo builders to find comparable homes, or “comps,” for the appraisal.

“There's nothing unique about them; we can finance the construction portion of these even with FHA, VA or conventional,” Stroud says. “If the borrower owns the land that can be their down payment.”

Barndos are a “new, sexy product” the younger generation is flocking to in Stroud’s area as a solution to a lack of affordable housing, he says. “This is not a fad that's here today gone tomorrow; this is here to stay,” he adds.

Barndo Financing Options

Here’s a look at some of the mortgage options you have to build a barndominium.

Construction loans

Construction loans are used to finance the home-building process, usually with a line of credit that the borrower draws on as construction progresses. There are two main types of construction loans: construction-only loans and construction-to-permanent loans.

A construction-only loan is a short-term loan, usually for one year, that covers the construction period only. However, because of the higher risk that construction may not be completed on time, fewer lenders offer this loan option and charge higher interest rates to account for the risk. Plus, once construction is complete, you’ll need a traditional mortgage to pay it off, meaning you’ll pay a second set of closing costs on an entirely new loan. Make sure you and the home can qualify for permanent post-construction financing prior to getting a construction loan.

Construction-to-permanent loan

A construction-to-permanent loan is a one-time-close loan that finances the building of a home before converting into a permanent mortgage. While your home is built, you’ll make interest-only payments before the loan converts into a traditional mortgage. In some cases, you can use the construction-to-permanent loan to also purchase the land you’ll build your barndo on, too.

Construction loans are available through conventional lenders who typically require a higher credit score (620 or above) and a minimum down payment of 3% to 5%. You can also use FHA and VA loans to build a barndo, Stroud says. You can put as little as 3.5% down with an FHA loan and zero down on a VA loan (if you’re a military borrower) or a USDA loan if you purchase in an eligible rural area. Income limits apply to USDA loans.

Even with all these option, it might still be tough to find financing in areas with few barndos. Before you get serious about your project, call lenders and secure your financing.