Everything You Should Know About Down Payment Gift Rules

Gift money can come from relatives and even friends in some cases. It can cover your down payment and/or closing costs, reducing or eliminating the cash you need to close the home purchase.

Money from a friend or family member could make all the difference. The gift could push you over the top when you’re struggling to save a down payment, making a new home possible.

But the unusually large sum of money in your bank account could also complicate mortgage approval. Before planning to use gift funds as a homebuying strategy, here’s what to know.

What Are Down Payment Gift Rules?

“Gift funds are a great way to meet the minimum down payment requirements of a mortgage,” said Josh Jampedro, a mortgage loan originator at Home Loan Advisers.

“But there are a few general rules as to what would qualify as gift funds, who can donate the money, and how it applies to each loan program,” he said.

Down payment gift rules vary by loan type and lender, but generally:

Lenders will require donors to write a letter stating they do not expect the gift to be repaid. The letter should also include the donor’s name, address, contact information, and the amount of the gift.

Lenders will need a copy of the donor’s check or proof of the wire transfer. They may also want to check bank statements for proof the funds were deposited.

Lenders may also ask borrowers to document their connection to the donor.

The purpose of these rules: To make sure the down payment gift has no strings attached.

A donor who expects repayment (or an ownership stake in the home) becomes a creditor. This changes the mortgage borrower’s credit profile. It could jeopardize mortgage eligibility.

Types of Gifts for Home Down Payments

Down payment gifts can come from:

A family member: Grandparents, parents, or other close family members can make large down payment gifts to help their relatives get established in a home of their own. Some relatives prefer this type of early inheritance as a form of estate planning.

An employer: In some professions, employers offer down payment matching funds or forgivable loans to help their employees get more established in the local community.

A community organization: Some nonprofit organizations help homebuyers make down payments. Typically, these grants work only in certain neighborhoods or for borrowers of lower income levels.

A group of friends, family, and co-workers: Borrowers who are graduating or getting married can ask for down payment cash instead of graduation or wedding gifts.

Local down payment assistance (DPA) programs can also help homebuyers meet their minimum down payments. Many DPAs provide funding through a loan, and lenders don’t consider this gifted money. However, they still need to know in advance when borrowers plan to use a DPA program.

Down Payment Gift Rules by Loan Type

Most mortgages — including conventional loans and government-insured loans — allow borrowers to use down payment gifts, Jampedro said.

For all loan types, gifts must:

Be freely given: Donors must submit a signed letter stating they do not expect repayment and will not put a lien on the property. Gifts cannot come from the Realtor, loan officer, seller, builder, title company, or anyone else who will benefit from the transaction.

Be sourced: Borrowers will need to document a copy of the check or wire transfer receipt showing how the money moved from the donor to the recipient.

Be available at closing: The money can be sent to the buyer prior to closing or directly to the closing agent or title company. But money can’t still be in transit or on hold in an account on closing day.

Beyond those general guidelines, gift rules vary by loan type

Conventional Loan Down Payment Gift Rules

Most homebuyers use conventional loans. Steven Parangi, a loan originator with Alpine Mortgage Services, LLC, said conventional loan borrowers can use gifted down payment money as long as they’re buying a primary residence or a second home.

Who can give: Family members or romantic partners

How much can they give: The entire down payment can come from gifted funds if the borrower is buying a primary residence. But there are limits to how much gifted money can be put toward second homes, Parangi said.

“For second homes with less than 20 percent down, burrowers must use at least 5 percent of their own funds,” he said.

On a $500,000 second home, for example, at least $25,000 of the down payment money must come from the borrower’s own funds — unless the borrower has enough cash to put $100,000 down.

Why this rule? Because second-home loans with smaller down payments are riskier for lenders. This minimum contribution from the buyer reduces the risk the borrower will foreclose.

Investment property loans cannot use gifted funds.

FHA Loan Down Payment Gift Rules

FHA loans offer an alternative for borrowers who don’t qualify for an affordable conventional loan. Since the Federal Housing Administration insures FHA loans, lenders can look past lower credit scores and smaller down payments, conditions that might tank a conventional loan application.

FHA borrowers with FICO scores of at least 580 can get approved with only 3.5 percent down. For a $300,000 home, 3.5 percent equals $10,500.

Who can give: “Gifts can come from family members, close friends with documented relationships, employers, charitable organizations, or government agencies,” Parangi said.

How much can they give: This entire down payment amount can come from gifted money, Jampedro and Parangi confirmed.

VA Loan Down Payment Gift Rules

VA loans, backed by the federal Department of Veterans Affairs, help qualifying veterans and active duty service members buy homes. Some spouses of military members who died in the line of duty can also use this program.

Most VA loans do not require a down payment, but VA borrowers can still benefit from using gifted money. The money can help pay closing costs. Or, the borrower might improve their credit profile and equity position by making an optional down payment.

Who can give: The VA’s rules for using gifts resemble the FHA’s, Parangi said. Family members, close friends, employers, charitable organizations, and government agencies can give.

USDA Loan Down Payment Gift Rules

Like VA loans, USDA loans require no money down. They’re backed by the U.S. Department of Agriculture, and they finance homes only in rural and suburban areas, as defined by the USDA. Also, borrowers must earn 115 percent or less of their area’s median income each year to qualify.

Despite requiring no money down, USDA loans still allow gift funds, which can be used toward closing costs or to make an optional down payment. Paying money down can lower the home’s monthly payment and begin the loan term with equity.

Who can give: USDA loans also resemble FHA and VA gift rules.

Required Documentation for Down Payment Gifts

Regardless of loan type, down payment gifts must be properly documented. Documents show:

The relationship: The connection between donor and recipient must be included in the gift letter. Some lenders may ask for additional documents to show the relationship to the donor

The money trail: If the donor writes a check, the lender will ask for a copy or digital image of the check and proof it was deposited into the borrower’s account. For electronic transfers, the lender will need to check the receipt. If the money hasn’t been transferred yet, the lender may ask for bank statements from the donor to make sure the funds are available

The donor’s intent: The gift letter must state the money is given with no expectation of repayment in the future

Borrowers should inform the lender immediately about plans to use gifted funds so the lender can outline its specific documentation rules.

Eligibility Criteria for Gift Givers

Exactly who can give down payment funds varies by loan type.

Typically, FHA loans can be more lenient about the sources of down payment gifts than conventional loans. FHA loans can allow gifts from community organizations, close friends, employers, or other government agencies.

FHA lenders may ask for more information about gifts from close friends. For example, the lender may ask how and when the friendship started. The lender needs to make sure the gift is not a loan in disguise.

Conventional loans regulated by Fannie Mae and Freddie Mac do not allow down payment gifts from friends. Gift money can come from the borrower’s spouse, parent, or any other person who is related by blood, marriage, adoption, or legal guardianship.

But some non-relatives can provide down payment gifts for conventional loans. These include domestic partners, fiances, former relatives, or godparents.

Alternatives to Cash Gifts for Down Payments

Not everyone has a family with deep pockets. Home buyers who need down payment help can also use:

Down payment assistance grants and loans

Nonprofit organizations and local governments operate down payment assistance programs in most housing markets. Some programs offer grants which never have to be repaid. Others provide forgivable loans or loans designed to complement the primary mortgage.

Some programs have income or geographical limits. To see programs in your area search “down payment assistance near me.”

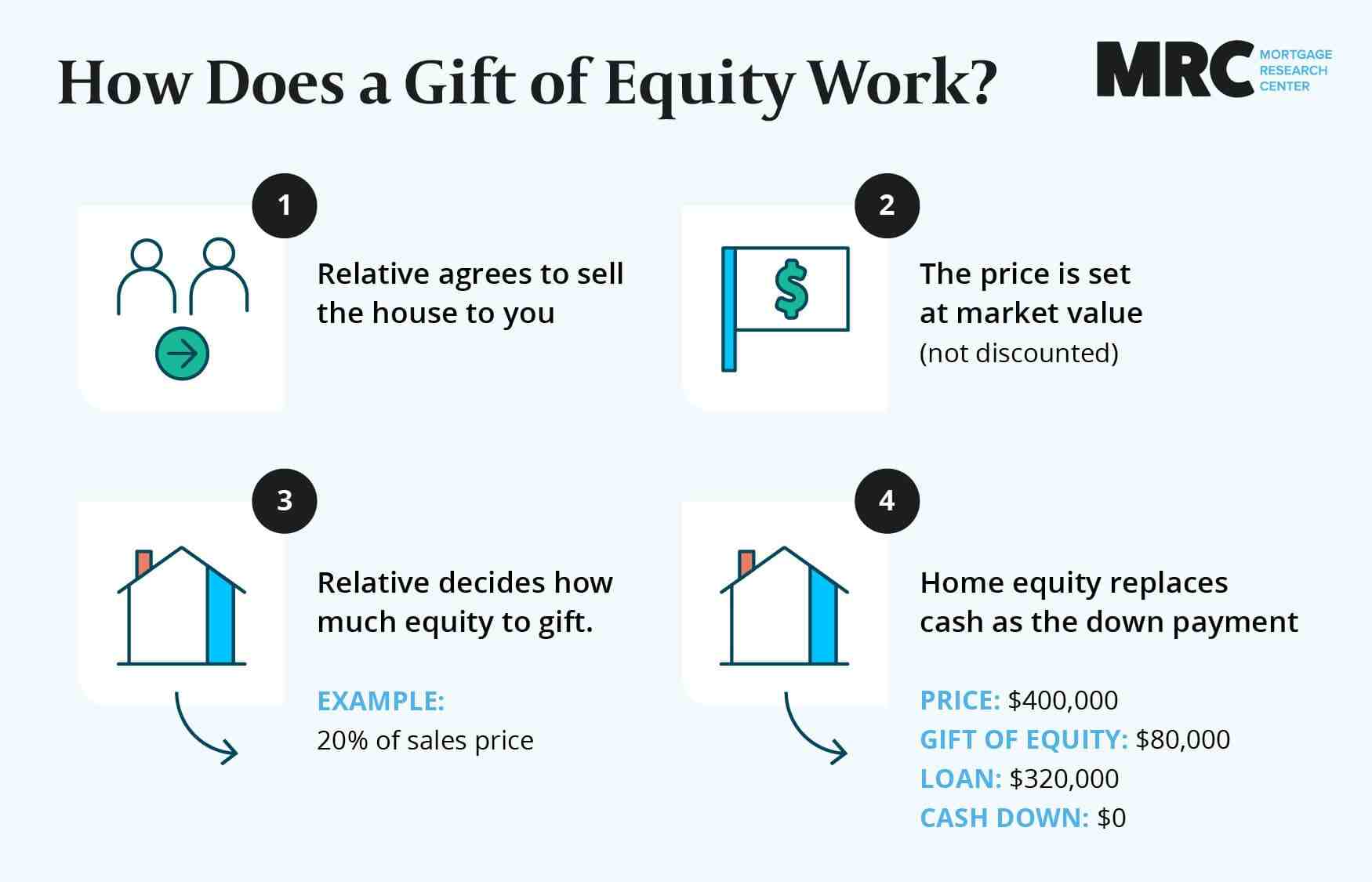

Equity as a gift (conventional loan)

Conventional loans allow gifts of equity. For this to work, the seller (your relative) agrees to sell the house at market value and then gifts you part of the proceeds as your down payment. No actual money changes hands. The transfer simply appears on the closing paperwork.

For example, let’s say you’re buying a home from your grandparents. The home appraised for $360,000, which is also the sales price. Your grandparents gift $60,000 in equity at closing, which serves as your down payment. If there’s any equity left over, they get that as cash at closing.

Employee match programs

Some employers help their employees buy a new home and get established in the local community either by matching the employee’s own funds or by providing forgivable loans. Employers who operate these programs will often forgive the loans if the employee stays at the job long enough.

Ask your human resources department about employer-assisted housing resources.

Rent to Own

Renting to own offers a foot-in-the-door approach to homebuying. In this scenario, the buyer would move into the new home and pay rent. The landlord/owner would save part of the rent to be used as a down payment on the home later.

These agreements can be risky. You’d be trusting the owner/landlord to honor the agreement. Renters should work with a financial advisor or attorney to understand their rights and obligations before entering the agreement.

Also, the gift will be considered an interested-party contribution, which has limits and may only be used for closing costs, not the down payment itself. The seller may only be able to apply 3-6% of the home’s price toward your cost to close.

Check USDA/VA eligibility

USDA and VA loans require no down payment, but not everyone can apply.

VA loans are a benefit for active duty service members, veterans, and some surviving spouses of service members.

USDA Guaranteed loans work only for homes in rural areas. The USDA’s definition of rural often includes suburbs within driving distance of major cities. Borrowers must also earn less than 115 percent of their area’s median income

For military-affiliated buyers who don’t have a down payment saved, a VA loan is almost always the best path to homeownership.

With Down Payment Gifts, Timing Matters

While it’s always a good time to receive the gift of money, the timing can affect the underwriting process, Parangi said.

“Borrowers should start gathering documentation as early as possible in the loan process, ideally before pre-approval,” he said.

“And lenders prefer gifted funds to be ‘seasoned,’ meaning they’ve been in the borrower’s account for at least one month before applying for a mortgage,” he continued. “This reduces underwriting scrutiny and simplifies documentation requirements.”