What Is a Conventional Loan? And Should You Get One?

Conventional loans are not government-backed, so are slightly more difficult to qualify for. But in return they offer better mortgage insurance rules and more flexibility in the type of home you can buy.

A conventional loan is any residential mortgage that’s not insured or guaranteed by a government agency. You’ll often hear them simply referred to as standard or traditional mortgages.

But what is a conventional loan, exactly? We’ll cover the ins and outs of conventional mortgages and whether they may be the right choice for you.

Key Takeaways

Conventional loans are residential mortgages not insured by a government agency.

Over 68% of purchase loans originate from conventional lenders.

Conforming loans are the most common type of conventional mortgage and follow the lending guidelines set by Fannie Mae and Freddie Mac.

Conventional loans are more difficult to qualify for but generally have fewer restrictions and fees than government-backed alternatives.

Conventional Loans: The Basics

Conventional loan refers to any type of residential mortgage not backed by the federal government. These home loans are funded through mortgage providers such as banks, credit unions, and private lenders.

More than 68% of buyers taking out a mortgage choose to go with a conventional loan, according to the CFPB. In fact, unless you’re specifically applying for a non-conventional mortgage, you’re likely applying for a conventional loan.

Non-conventional mortgages include those guaranteed through the FHA, VA, or USDA home loan programs. These programs can be easier to qualify for but have more restrictions than when using conventional financing.

Conventional loans tend to have slightly higher interest rates than their government-backed alternatives. However, program-specific fees can often make non-conventional mortgages more costly both monthly and over the long term.

Conventional vs Conforming Loans

You’ll commonly hear the words conventional and conforming used interchangeably, but there is a distinct difference.

Conventional Loans: All residential mortgages without government backing or guarantee

Conforming Loans: Conventional loans which conform to the lending guidelines established by Fannie Mae and Freddie Mac

This means that all conforming loans are conventional, but not all conventional loans are conforming. Most frequently, though, when you hear someone mention a conventional loan, they’re actually talking about a conforming loan.

Types of Conventional Loans

Conventional loans come in all shapes and sizes, with lenders often willing to customize a mortgage to fit the needs of their borrowers.

Some of the flexible features available with a conventional loan include:

Term Length: Most buyers opt for a 30-year mortgage, but alternatives, including 10, 15, and 20-year loans, are available and can save you on interest costs.

Fixed Rate vs Adjustable Rate: Fixed-rate mortgages have an interest rate that stays consistent for the life of your loan. Your monthly principal and interest payments will not change. Adjustable-rate mortgages (ARMs) will have a set interest rate for their introductory period, with the rate typically adjusting to current market trends on an annual basis afterward.

Property Types: Conventional loans are available when purchasing your primary residence, a second or vacation home, and even for investment properties. You can also use them to buy multifamily properties with up to four individual units. In most cases, government-backed loans are only available for your primary residence and sometimes only for single-family properties.

Different Uses: In addition to purchasing and refinancing, you can also use conventional loans to construct a brand-new home or renovate an existing property that you plan to purchase or already own.

Check out our guide to The Types of Conventional Loans and Their Uses to learn more.

Different Conventional Loan Programs

Conventional loans are not a single type of residential mortgage – there are numerous conventional loan programs designed to fit the needs of varying buyers and homeowners. We'll go over some of the most popular.

Conventional 97 Loans

Conventional 97 loans are available with as little as 3% down for buyers who qualify as first-time homeowners or who earn no more than 80% of their area median income.

These programs include:

Fannie Mae 97% LTV Standard (first-time homebuyer)

Freddie Mac HomeOne (first-time homebuyer)

Fannie Mae HomeReady (low-to-moderate income)

Freddie Mac Home Possible (low-to-moderate income)

Keep in mind that borrowers can qualify as first-time homeowners if they have not owned a primary residence within the past three years.

5%-Down Conventional Loans

Repeat buyers, or those who make more than income limits for 3% down loans, may still qualify for a 5%-down conventional loan. This standard conforming mortgage is available to all borrowers who meet Fannie Mae and Freddie Mac qualification guidelines.

Note: Fannie Mae recently updated their guidelines to allow buyers to use 5%-down conventional loans to purchase multifamily properties with up to four units so long as they occupy one of the units as their primary residence. In the past, this would require a down payment ranging from 15% to 25%.

Conventional Construction Loans

Conventional construction loans are available to fund the building of a brand-new home. This can include purchasing land or building on property you already own.

You can get a conventional construction loan that converts to a permanent fixed loan once construction is complete.

Conventional Rehab Loans

You can use a conventional rehab loan to renovate or repair a property and include the cost of improvements in with your loan. You can apply for a rehab mortgage to purchase a home or to refinance and renovate one that you already own.

Conventional rehab programs include Fannie Mae’s HomeStyle Renovation and Freddie Mac’s CHOICERenovation.

Unlike other mortgages, rehab loans are based on your home's after-improved value, meaning that you may be able to borrow more than with non-renovation financing.

Jumbo Loans

Jumbo loans refer to any mortgage above the local mortgage limits set annually by the Federal Housing Finance Agency (FHFA). It's common to find jumbo lenders offering loans of $2 million to $3 million or more.

Unlike the other conventional loan options we’ve covered so far, jumbo loans are non-conforming since Fannie Mae and Freddie Mac guidelines require lenders to abide by FHFA loan limits.

Other Types of Conventional Loans

We've gone over some of the most popular conventional mortgage programs. Still, as we stated before, conventional loans come in all shapes and sizes. You will find mortgage companies offering countless varieties of non-conforming conventional loans, from doctor mortgages to subprime financing and more.

Conventional Loan Eligibility Requirements

You will need to meet conventional loan eligibility requirements to qualify for a mortgage. While requirements can vary based on the lender you choose, there are some set standards that all conforming loans must follow.

Note: Individual mortgage providers often establish their own more restrictive lending guidelines. If you meet these minimums but can't get approved due to restrictive lender overlays, apply again with another company.

Credit Score

Lending guidelines require a credit score of at least 620 for all conforming loans. This is a common baseline requirement for all conventional lenders, except those explicitly catering to lower-credit borrowers with high-interest, non-conforming loans.

Debt-to-Income (DTI) Ratio

Your debt-to-income ratio is the percentage of your qualifying income used to cover installment and revolving debt obligations. This includes the mortgage you’re applying for and things like auto financing and student loans. Most conventional lenders look for a DTI of 43% or lower, although borrowers can get approved with a DTI as high as 50%.

Loan Limits

Most conventional loans are subject to lending limits. These can vary by location. Check your local loan limits on Fannie Mae’s map tool.

Private Mortgage Insurance (PMI)

Conventional loans with less than 20% down (or 20% equity when refinancing) require private mortgage insurance, or PMI. PMI is more expensive for borrowers with lower credit scores. Conventional mortgage insurance is cancellable once you reach 20% equity in your property.

Employment History

Lenders prefer two years of steady and stable employment history. This doesn’t necessarily need to be with the same employer and can include seasonal and part-time work. You may even be able to qualify if you have had a recent employment gap.

Credit History

You cannot have any recent significant adverse credit events. To get a conventional loan, you typically need to wait 2 to 4 years after bankruptcy, 4 years after a short sale, and 7 years after foreclosure. However, if your past financial issues resulted from extenuating circumstances, you may be able to shorten the timeframe.

How Conventional Loans Compare to Government-Backed Mortgages

Conventional loans have fewer restrictions than government-backed mortgages but typically have slightly stricter eligibility requirements. Here's a chart reviewing each program's basics, including any required fees.

Credit Score | DTI | Down Payment | Fees | |

Conventional | 620 | 50% | 3% to 5% | Risk-based PMI under 20% equity |

FHA | 580 (500 with 10% down) | 56.9% | 3.5% | 1.75% UFMIP & ~0.55% annual MIP |

VA | 580 to 620 | 40% to 50% | 0% | VA funding fee up to 3.3% |

USDA | 580 to 640 | 44% | 0% | 1% upfront and 0.35% annually |

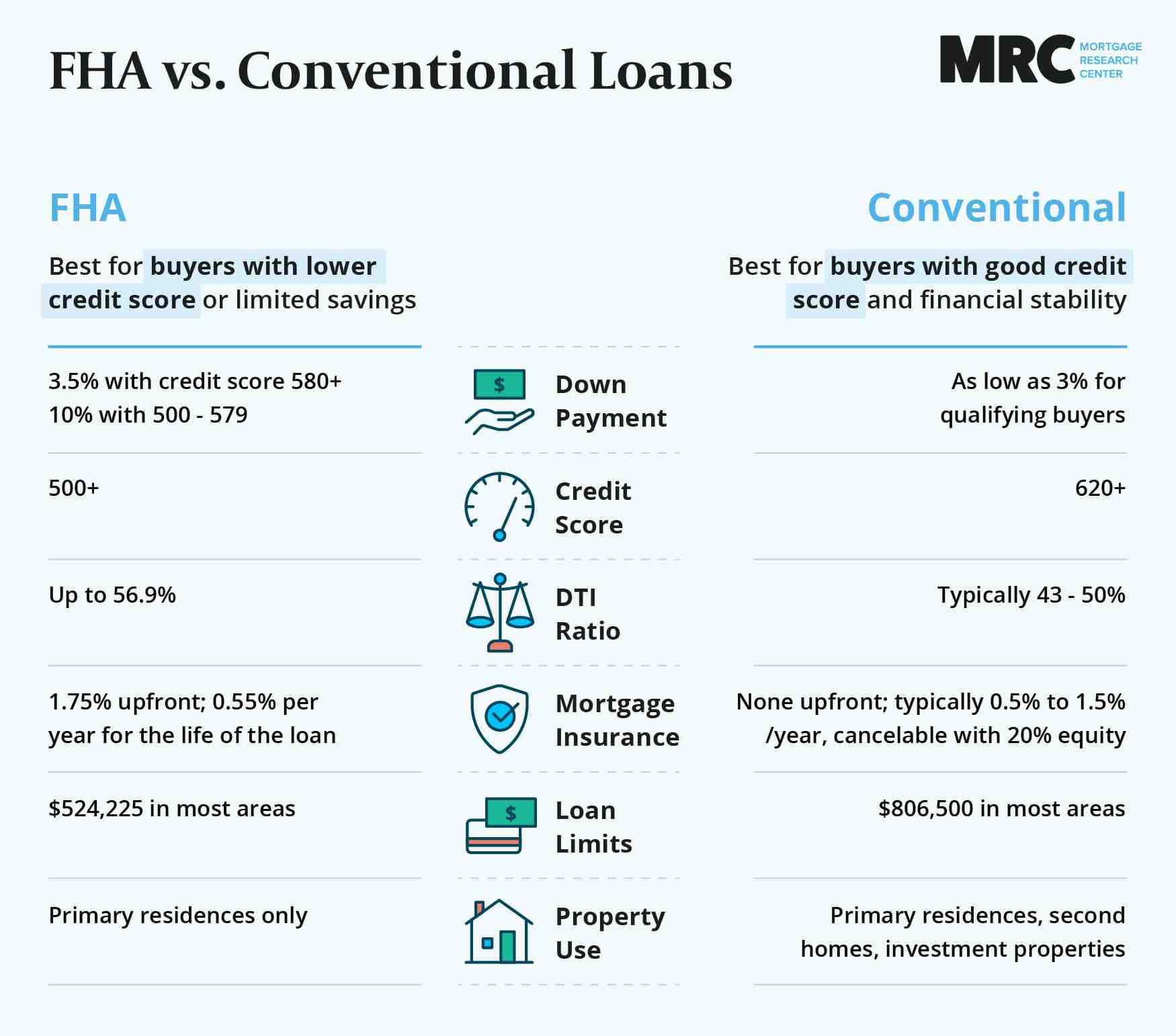

Conventional Loans vs FHA Loans

FHA loans are the most common type of government-backed mortgage. The Federal Housing Administration insures them with the aim of enhancing homeownership among borrowers who may not qualify through conventional lenders.

You can get an FHA loan with a 3.5% down payment and a credit score of 580. Select mortgage companies may be willing to approve loans with a score as low as 500 if you have 10% down. FHA lenders also allow for more debt, with a max DTI of up to 56.9%.

Compared to conventional loans, FHA-backed mortgages generally have lower loan limits, which you can see here.

While conventional loans require risk-based PMI on loans with less than 20% down, the FHA adds a mortgage insurance premium (MIP) to all loans, regardless of equity. This includes a 1.75% upfront premium and an ongoing MIP ranging from 0.15% to 0.75%, with most borrowers paying 0.55% for the life of their loan.

Check out our guide to FHA loans vs. conventional loans for more information.

Conventional Loans vs VA Loans

VA loans are backed by the US Department of Veterans Affairs. They are only available to veterans, active-duty service members, and some surviving spouses. VA loans are often an excellent deal for those who qualify.

Due to their government backing, VA mortgages generally come with some of the lowest interest rates. You can also use them to finance 100% of your purchase price, meaning you won't need to make a down payment.

The VA leaves discretion on credit scores and DTI ratios up to individual lenders, with most setting minimum scores ranging from 580 to 620. Maximum debt-to-income figures with VA lenders commonly range from 40% to 50%.

VA loans have no maximum limit, with loan size only restricted by your ability to borrow. They also don’t require mortgage insurance, even with 0% down. They do, however, have an upfront VA funding fee of either 2.15% or 3.3% for most buyers.

Check out our guide to when to choose a conventional loan over a VA loan here.

Conventional Loans vs USDA Loans

Insured by the US Department of Agriculture, USDA loans assist low-to-moderate-income buyers in purchasing property in agency-designated rural communities. These rural development loans require no money down and have lower fees than other types of government-backed mortgages.

You’ll need to meet USDA income limits, which include the earnings of all adults in your household, not just those applying for the loan.

The USDA has no fixed minimum credit score, although many lenders look for a score of 640. These loans also have a 1% upfront guarantee fee and an ongoing fee of 0.35% per year for the life of the loan.

Why Choose Conventional Over Government-Backed?

Government-backed loans often have lower interest rates than comparable conventional mortgages and are typically easier to qualify for.

So why would a borrower choose to go with a conventional loan instead? This typically boils down to conventional loans having fewer restrictions and no upfront or lifetime fees.

Fewer Restrictions

While they may have stricter eligibility criteria, conventional loans have far fewer lending restrictions than non-conforming government-backed alternatives.

For example, you can use a conventional loan to:

Buy a second home or investment property

Purchase a fixer-upper that doesn’t meet other agencies’ standards

Make a smaller down payment than through the FHA for first-time and lower-income buyers

Take out a loan larger than FHA or USDA limits allow

Shop without worrying about geographical limitations

No Upfront or Lifetime Fees

Conventional loans have no upfront fees and only require private mortgage insurance until you reach 20% equity in your home. Since it is risk-based, PMI may be cheaper for borrowers with higher credit scores than the FHA mortgage insurance premium, which persists for the life of most purchase loans.

Government-backed borrowers pay an upfront fee of 1.75% for FHA loans, 1% for USDA loans, and 2.15% to 3.3% for most VA purchase loans.

Pros and Cons of Conventional Loans

Most buyers choose conventional loans to fund their home purchases. But while there are plenty of good reasons to go conventional, there are also some downsides worth considering.

Advantages of Conventional Loans

Borrowers with excellent credit often qualify for lower interest rates and monthly payments.

Making a 20% down payment allows you to avoid all mortgage insurance costs.

You can purchase fixer-uppers and other homes that don’t meet government-backed minimum property requirements.

You can finance vacation homes and investment properties.

Loan limits are generally higher than federally insured options.

Disadvantages of Conventional Loans

Credit requirements are higher than government-backed mortgages, particularly for borrowers with a sizeable down payment.

Must meet first-time or lower-income buyer requirements to qualify for a 3% down conventional loan.

Interest rates are higher than government-backed programs, although program fees often make them more costly overall.

Lower DTI limit than FHA loans, which allows ratios as high as 56.9%, means less purchasing power.

They take longer to qualify for following a bankruptcy, short sale, or foreclosure.

What You’ll Need to Get a Conventional Loan

Does it sound like you fit the criteria for a conventional loan? The next step is to get in touch with a lending professional who can help you establish precisely how much of a mortgage you can qualify for.

During the loan approval process, you’ll likely be asked to provide:

Proof of income, including paystubs, W-2s, and two years of filed and accepted income tax returns

Two months of bank statements, as well as statements for investment and retirement accounts

Permission to run a credit report to assess your score, debts, and overall financial history

Gift letters for any contributions from family or friends certifying that the funds are indeed a gift and not a loan of any kind

Documentation of alternative credit sources for applicants with little or no credit history

However, an increasing number of mortgage companies are beginning to use direct verification to greatly reduce the amount of paperwork you're required to submit.

Should You Get a Conventional Loan?

Ultimately, the decision to get a conventional loan will largely depend on your unique financial situation. For borrowers who are eligible, however, conventional loans can end up being the most straightforward and cheapest option in the long run.

To find out if you qualify for a conventional loan, as well as any other residential mortgage programs you may be eligible for, get in contact with a reputable local lender who can go over your personalized financing options.