What Is the Average Down Payment On A House?

The average down payment for first-time homebuyers is just 9%, thanks to a variety of programs that don't require the traditional 20% down.

Your down payment plays a big role in your home purchase. It directly affects your monthly payment, your interest rate, and how quickly you can pay off your loan, and it can even impact your ability to get approved for a mortgage altogether.

But down payment amounts vary widely and are based on many factors — loan program, location, and more. While 20% has long been a rumored goalpost for homebuyers, the data shows that nowadays, most buyers offer less than this.

“Many still believe the minimum down payment requirement is 20%,” says Rose Krieger, senior home loan specialist at Churchill Mortgage. “It isn't, but if you can afford to put 20% down, there are many advantages. You will be setting yourself up for a lower payment, possibly have no mortgage insurance, obtain a better rate, and have instant equity in your home.”

Still, Krieger says, “If you don’t have 20% available, that is absolutely fine.” How much exactly should you prepare to put down, though? Learn more about average down payment amounts below and use that info to guide your own homebuying decisions.

Highlights

In 2024, the median down payment is 18%; first-time buyers average 9%, repeat buyers 23%.

Many loans allow 0%-3% down, though 20% avoids PMI and lowers costs.

Balance your budget, loan costs, and market competitiveness when choosing a down payment.

What is the Average Down Payment on a House?

The median down payment on a house in 2024 is 18%, according to the National Association of Realtor’s Profile of Buyers and Sellers report. This is slightly less than the oft-talked-about 20% down payment and is likely due to the wide variety of low-down loan programs and down payment assistance programs that are now available.

First-time buyers tend to pay less than experienced homeowners — those who are selling a home and buying another. According to the National Association of Realtors (NAR), first-time buyers had a median down payment of 9% this year, compared to 23% for repeat buyers.

“We’ve seen such rapid price appreciation and property values, so anybody that owned a home or purchased a home within the past five years has benefitted from all this equity,” says Dana Bull, a Massachusetts-based real estate consultant. “Now, they have these funds available to put down for their next home.”

Average Down Payment Trend in 2024

The average down payment on a house may be below that magic 20% threshold, but it’s actually on the rise. In fact, first-time buyer down payments are at their highest point since 1997, per NAR’s data, and repeat buyer down payments are at their highest since 2003.

There are many factors that play into this, experts say. Rising home values give repeat buyers more cash, for one. And for first-time buyers, there’s an influx of gift funds thanks to older generations.

There’s a “transfer of wealth” going on with Millennials and Gen Z . “Many of my clients receive gift funds to help with the down payment,” Bull says.

Finally, there are a lot more cash offers than in recent years. Per NAR’s data, a whopping 26% of buyers bought homes in all cash in 2024 — up from just 20% in 2023. This forces mortgaged buyers to up the ante in order to stay competitive.

“Most of the buyers are highly financially qualified,” Bull says. “They’re striking their appraisals or coming to the table with straight cash. In order to really be competitive, these first-time buyers are oftentimes having to scrounge up more money.”

Breakdown by State

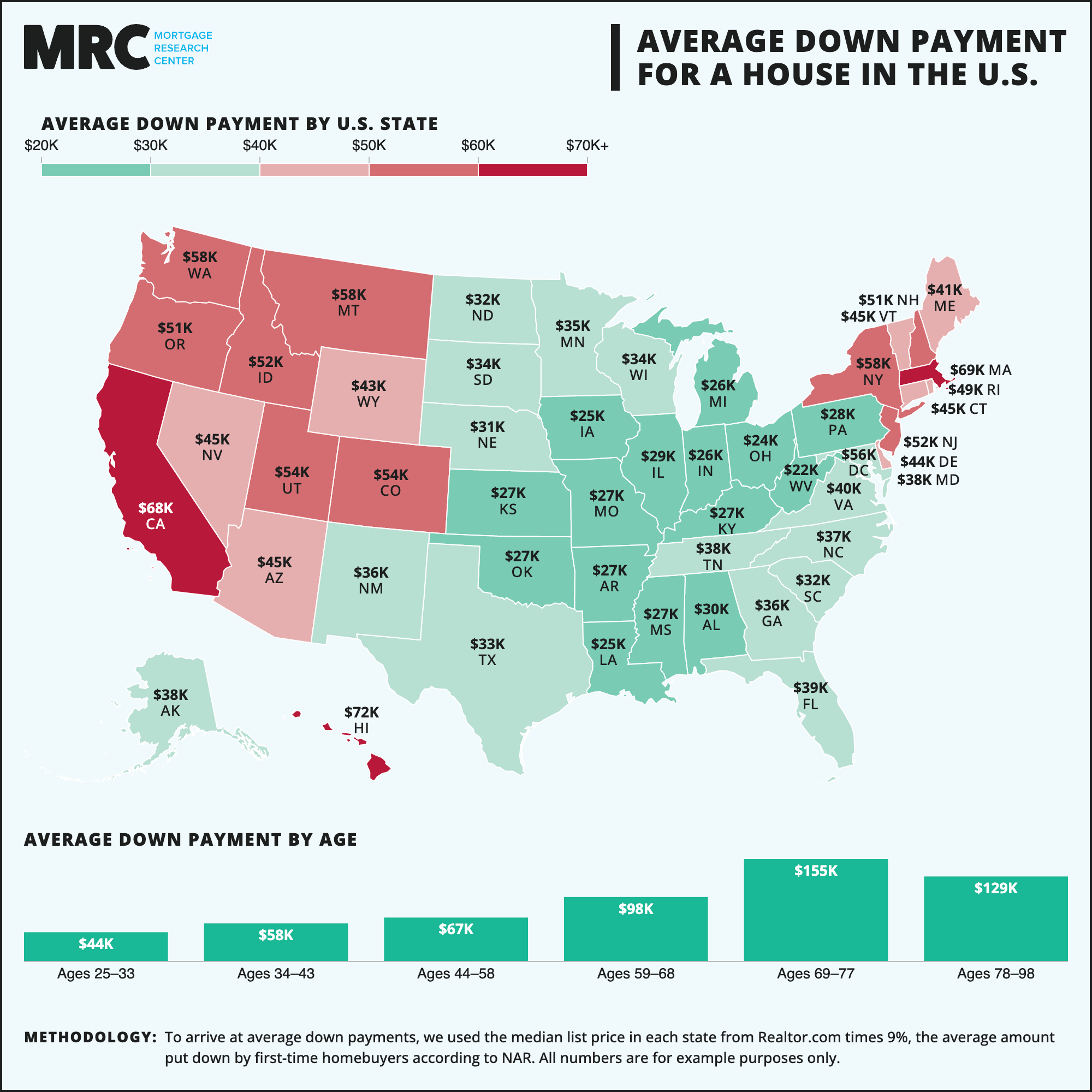

In the above infographic, we assumed the first-time homebuyer average of 9% times the average list price per state according to Realtor.com.

Down payments vary quite a bit by location, however. First, home prices — and therefore down payments as a share of those prices — can be wildly different from one state (even one city) to the next.

Differing income trends, property taxes, and housing market conditions, which dictate how competitive an offer needs to be, diverge widely from place to place, too. In New Hampshire, for instance, buyers are putting down nearly 21% on average, according to Realtor.com, and in New Jersey, it’s 18%.

In Alaska, though, buyers are averaging a down payment of just over 10%, and average down payments are actually falling in Montana, Wyoming, Oklahoma, South Carolina, Utah, Florida, and Delaware.

Breakdown by Age

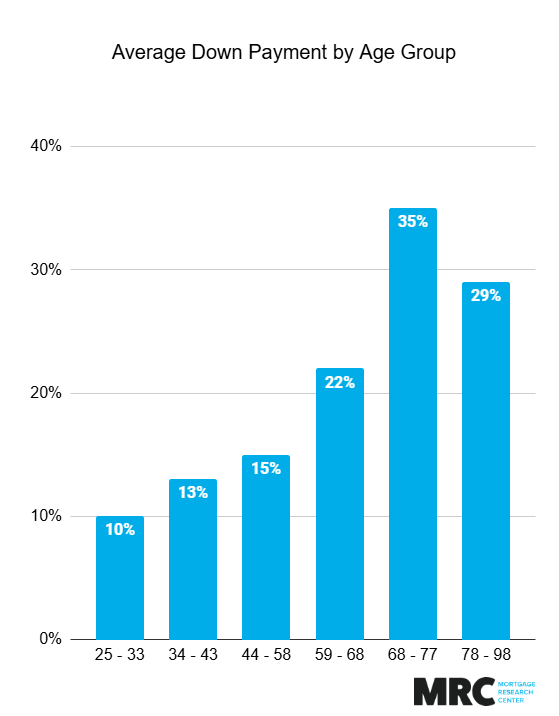

Average down payment amounts tend to rise as a buyer’s age does. Case in point: According to NAR’s 2024 Home Buyers and Sellers Generational Trends report, the typical 25 to 33-year-old buyer puts down just 10%, while the typically 69 to 77-year-old buyer opts for a 35% down payment.

“People between 69 to 77 years old most likely have owned their home for quite some time and have built up equity they can use on a new home,” Krieger says. “Most homeowners in that age range are also looking to downsize while cashing in on their equity for supplemental income. The primary advantage here is time.”

See the full breakdown of down payments across age groups below:

Age | Down payment amount |

25-33 | 10% |

34-43 | 13% |

44-58 | 15% |

59-68 | 22% |

69-77 | 35% |

78-98 | 29% |

Other factors play in, too. Younger buyers, for example, are more likely dealing with student loans, and recent inflation has made it harder for them to save, too. There are also income disparities between those just starting in the workforce and those more experienced in their careers.

“There are some advantages that older borrowers do have,” says Christopher Mediate, president at Mediate Financial Services. “They have longer credit histories and possibly more resources.”

Finally, younger buyers tend to be more knowledgeable about low-down programs and down payment assistance than older ones.

“Most buyers know that there are opportunities where you can do a low down payment,” Bull says. “I think it’s more about a generational perspective. Most of our parents and grandparents didn’t have the option to do a low down payment, so they aren’t really aware of it.”

Is a 20% Down Payment Required?

The 20% down payment has been talked about for decades, and it likely boils down to how private mortgage insurance works. On conventional loans, if you put down less than 20%, you typically need to pay for private mortgage insurance, or PMI, which adds to your monthly payment.

This insurance protects the lender if you fail to make your payments, and it takes some of the risk out of lending money to borrowers with less financial skin in the game (i.e., smaller down payments).

“I think there is a sticking point around the 20%, because if you’re putting down 20%, you probably won’t have to pay PMI,” Bull says.

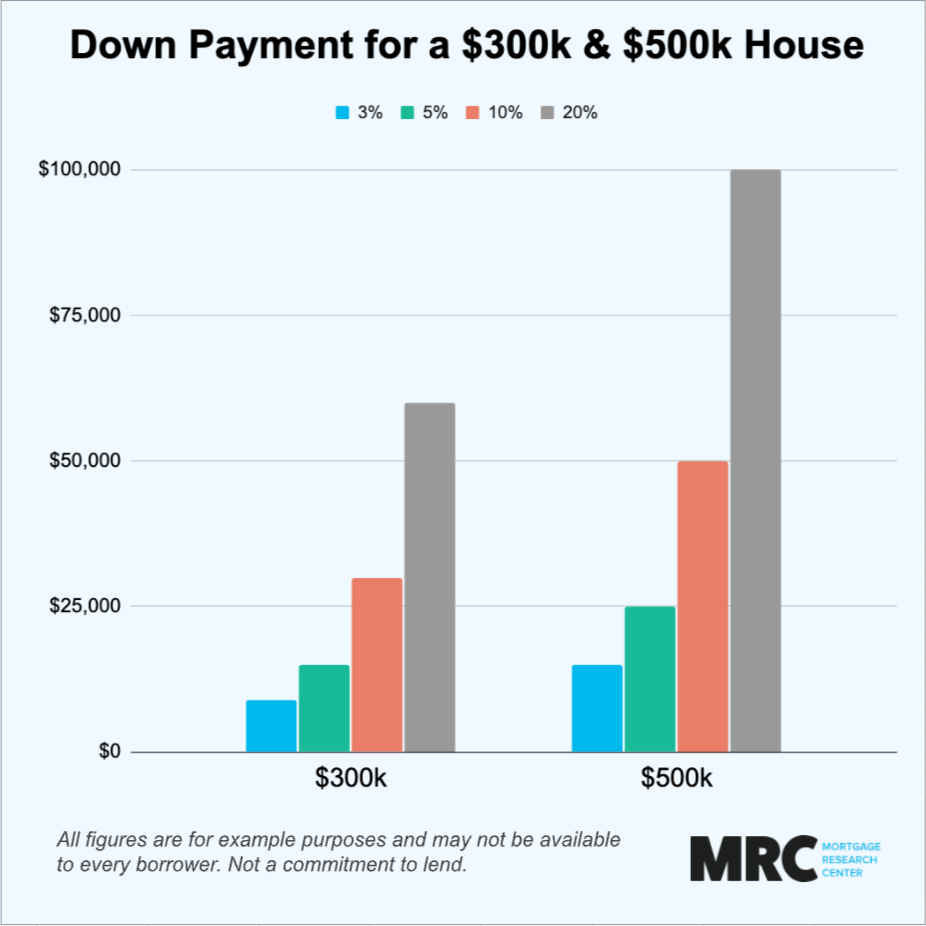

Few mortgage programs outright require 20% down. In fact, many require just 3% or less (and some require zero down payment at all).

Could 20% help you avoid PMI? You bet. Are there times when a 20% down payment might be smart otherwise? “Absolutely,” Bull says, but it depends on where you’re located and your unique buying situation.

“I think just to be competitive in certain markets, there’s sort of a baseline that having 20% down is really going to help your case,” Bull says.

What is a Good Down Payment?

The right down payment depends on lots of factors, including the loan program you’re using, the housing market conditions where you’re buying, your financial situation, and more.

To determine what down payment you should make, you’ll want to think about:

Its impact on your monthly payment and interest rate: The bigger your down payment, the lower your monthly mortgage will be. It will also likely result in a lower interest rate, which can reduce the long-term costs of your loan.

Its impact on your finances: You don’t want to drain your savings dry to cover your down payment. Make sure you have plenty of money left over to cover an emergency, as well as regular home maintenance and repairs.

PMI: PMI isn’t always a bad thing, but typically, putting down at least 20% will help you avoid it. Talk to your loan officer about what PMI would mean for your loan — and how much you’d need to put down to avoid it.

Your financial profile: How are your finances otherwise? Do you have good credit and a low debt-to-income ratio? These are factors that your lender will consider when assessing your application. If you have any risks they’re worried about, offering a higher down payment can help offset those.

You should also ask yourself, “How is your down payment going to be perceived when you’re actually submitting offers?” Bull says. “If it’s very likely that we are going to be up against cash buyers or financially sound buyers who are waiving financing contingencies, then a low down payment may not be competitive.”

Down Payment Based on Loan Type

The type of mortgage you use is going to determine the minimum down payment you’ll need to put down (though you can always put down more). Here’s a look at how down payment requirements break down by loan option.

Conventional Loan

Conventional loans require a 3% minimum down payment or, if you want to avoid PMI, 20%, with most lenders. If you have a lower credit score or debt-to-income ratio, or you have other risk factors on your application, a lender could require you to put down more.

Keep in mind that while a small down payment will mean less out-of-pocket at closing, it will also equate to a higher monthly mortgage, a higher interest rate, and more long-term loan costs. You will also have to pay for PMI.

Check out our guide to the Conventional 97 (3% down) and the Conventional 95 (5% down) loans to learn more.

FHA Loan

FHA loans — mortgages that are guaranteed by the Federal Housing Administration — are designed for low-to-moderate-income buyers and allow for low down payments, too (though the exact amount depends on your credit score.) If your score is 580 or above, you can make a down payment of just 3.5%. If it’s 500 to 579, you’ll need at least 10%.

These are just the minimums set by FHA, though, so individual lenders can set higher thresholds if they’d prefer. FHA loans also come with mortgage insurance (called a Mortgage Insurance Premium) both upfront and as part of your monthly payment. You’ll owe this no matter what your down payment amount is and, most likely, pay it for the remainder of your loan term.

Despite this extra cost, FHA loans can often be a smart option for first-time buyers, as they have less stringent qualifying requirements than conventional loans.

VA Loan

The VA loan program is backed by the Department of Veterans Affairs and offers loans to veterans, military members, and their spouses. Some National Guard and Reserves members are eligible as well.

With VA loans, borrowers need no down payment whatsoever. They also come with low interest rates and have no mortgage insurance requirement (though there is a guarantee fee you’ll need to pay, which helps keep the VA loan program afloat).

There may be some cases in which you’d need to make a down payment, but only if you borrow a very large amount.

USDA Loan

If you’re interested in buying a home that’s in a more rural part of the country, you can use a USDA loan, which is backed by the Department of Agriculture. Like VA loans, these also require no down payment and come with low interest rates. You will also need to fall under a certain income threshold to qualify.

Only homes in certain areas are eligible for USDA loans, so make sure to view the USDA’s eligibility map before considering this type of mortgage.

What's the Right Down Payment for You?

Your down payment is a personal decision based on your budget, goals, and loan options. While larger down payments can lower costs, smaller ones can help you get into a home sooner.

Use our mortgage calculator to explore how different down payment amounts impact your monthly payment and overall loan costs. It’s a quick and easy way to see what works best for your situation—and take the next step toward homeownership with confidence.