Attorney opinion letters are often less expensive than title insurance, and are allowed by major lending agencies in some cases. But the risks may outweigh the reward for some homebuyers.

You purchase your first home, settle in, and have your first Christmas and child’s first birthday there.

Then, someone knocks on the door and says, “I actually own this home. Leave.”

What do you do?

In this rare but possible scenario, title insurance would kick in. It would pay for legal fees to fight such a claim and reimburse you for the home if you lose it in a court of law.

That’s why a revised rule for conventional loans allowing Attorney Opinion Letters (AOLs) in lieu of title insurance is gaining attention. Are AOLs safe?

What Is an Attorney Opinion Letter vs Title Insurance for a Home Mortgage?

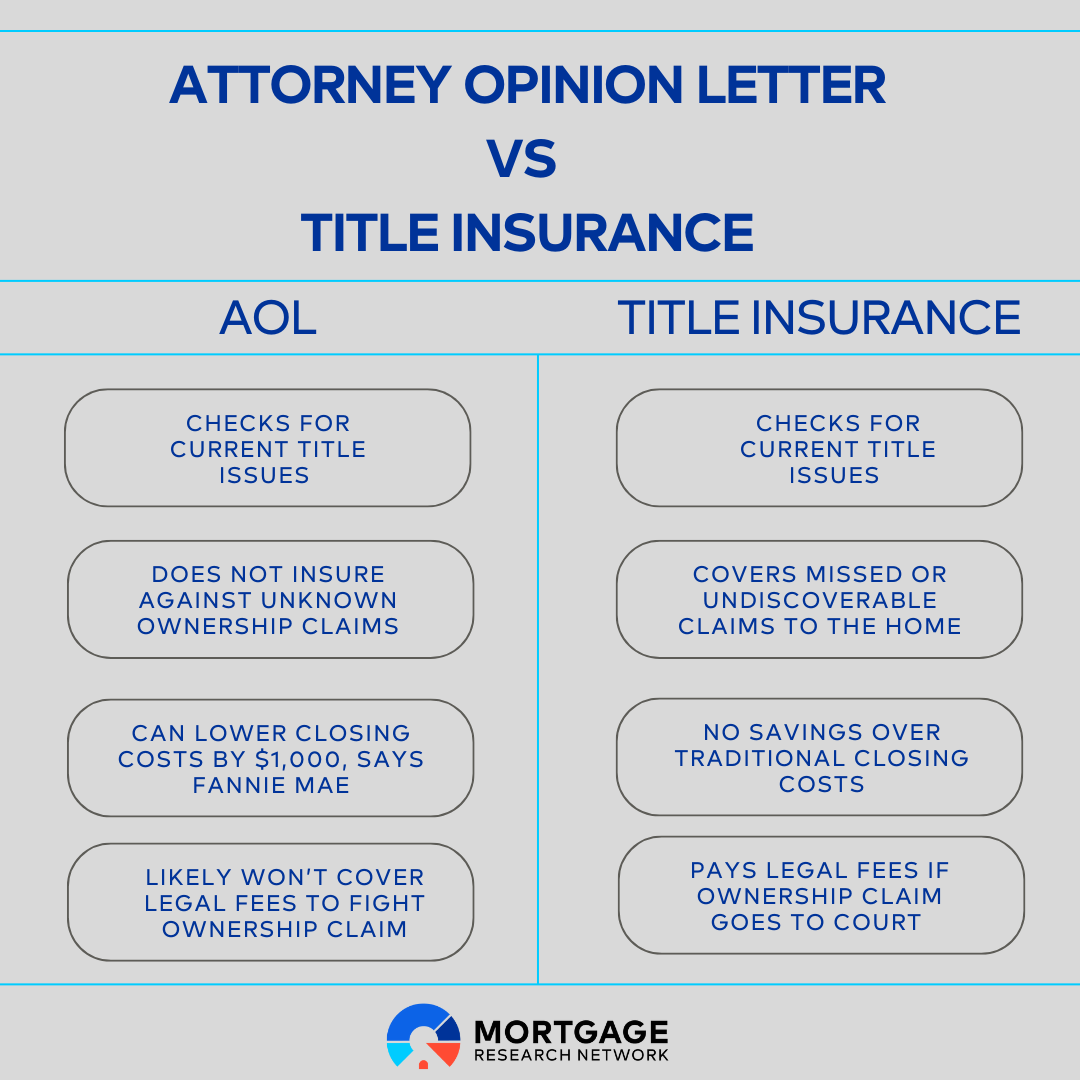

In regards to a residential home mortgage, an AOL is a letter from an attorney stating that a property’s title and ownership history is “clean.” There’s little or no risk that someone has a lawful ownership claim or lien against the property.

Title companies also research the property and give such an opinion. But they go a step further by backing it up with an insurance policy in case of errors or undiscoverable facts at the time.

Why Would Someone Want an Attorney Opinion Letter Instead of Title Insurance?

There’s only one reason someone would want an AOL over title insurance: cost.

Title can be downright expensive. Affordability is the reason conventional loan agencies Fannie Mae and Freddie Mac allow AOLs.

The agencies are seeking to reduce the upfront cost of homeownership by addressing one of its highest fees.

According to Fannie Mae, borrowers in its system who have used an AOL instead of title insurance have saved over $1,000 in closing costs.

What Are the Risks of an AOL?

If AOLs are less expensive, then why haven’t they become the industry standard?

They come with added risk to the homeowner.

An AOL is based on research of the property’s ownership history at the time. While an attorney’s errors and omissions insurance may cover some losses, it won’t cover others.

For example, an AOL may not cover legal fees associated with fighting an ownership claim, and it may not reimburse the value of the property if no evidence of claims existed at the time of review.

Does Anyone Advise Against AOLs?

It’s no surprise that title companies don’t like the idea of AOLs. Their business relies on issuing insurance policies to homebuyers and refinancing homeowners.

Still, title professionals bring up valid points. CEO of World Wide Land Transfer Marc Shaw says in Forbes that an AOL would not protect owners against myriad invisible land mines such as undiscoverable mechanics liens, tax liens, forgeries, or property ownership technicalities.

But not all AOL naysayers are in the title industry. Far from it.

Seventeen members of Congress issued a letter to the then-director of the Federal Housing Finance Agency (overseers of Fannie Mae and Freddie Mac) saying the lack of title insurance could “inadvertently cause irreparable damage to homeowners and lenders by leaving them without critical protection against financial loss.”

We would always recommend that clients have title insurance. There is a lot of property theft happening across the country right now with remote notary scams.

Interestingly, not even all attorneys think AOLs are a good idea, though it would certainly increase business for them. Thomas Lofton, an attorney at Oseran Hahn in Bellevue, Wash. says, “This is not something we do. We would always recommend that clients have title insurance.” Lofton goes on, “There is a lot of property theft happening across the country right now with remote notary scams.”

An AOL is an attorney’s best guess of the homeowner’s risk based on information at the time.

Although an imperfect example, it’s a little like getting a professional opinion that you’re a great driver and therefore bypassing car insurance. It works great until it doesn’t.

Title insurance can protect against unforeseen “accidents” in legal ownership, paying legal fees and even reimbursing the full property value, even if new evidence arises years later that was not discoverable at the time of home purchase.

Are AOLs Too Risky?

If AOLs are a risk, then why are Fannie Mae and Freddie Mac big proponents?

The argument is that this provision will encourage homeownership by shaving $1,000 or more off of closing costs, according to their data.

These agencies are fine with a few percent of their loans going bad for various reasons, such as foreclosures or title issues. For them, AOLs are a totally acceptable risk.

In fact, Fannie Mae has purchased 10,000 loans with AOLs since 2009 (they have allowed it under more strict guidelines prior to wider acceptance since 2022). It states it has not experienced any losses on these loans.

Homebuyers might decide they’re willing to chance it, too. Skipping title insurance may be a profitable gamble.

According to CEIC Data, title insurance companies have paid out anywhere from 2.2% to 8.5% of premiums since 2012 for losses and costs related to losses like legal fees.

Compare that with loss payouts of 60% of premiums for auto and home insurance companies.

In short, your risk of a title issue is much smaller than that of an auto accident or flooded basement. But if the odds aren’t in your favor, the losses could be catastrophic for the homeowner. What’s an acceptable risk to a massive corporation may not be to a homeowner.

How Much Can an AOL Save the Buyer?

To use an AOL, you should be saving a lot of money upfront.

But how much you spend on title as the buyer varies drastically by state.

When reviewing cost, it’s important to know there are two kinds of title insurance policies:

Lender’s title policy: Protects the loan

Owner’s title policy: Protects the owner and home

In many states, the seller pays for the owner’s policy. So as a buyer, you gain nothing by using an AOL for the owner’s policy.

According to real estate writer Ilyce Glink, the seller pays the owner’s policy in 19 states, and the buyer pays that cost in 19 states and the District of Columbia. The cost is split or negotiable in the remaining states.

According to the First American Title fee calculator, following are example title fees on a $500,000 home purchase with a $450,000 loan amount.

$500k home $450k loan | Lender’s policy (protects loan amount) | Owner’s policy (protects home value) | Buyer cost |

Seattle, Washington | $846 | $1,891 | $846 |

Dallas, Texas | $2,960 | $363 | $3,223 |

Sacramento, Calif. | $942 | $1,743 | $942 |

Raleigh, North Carolina | $1,261 | $0 | $1,261 |

Homebuyers in Dallas have a lot more to save than a homebuyer in Seattle, thanks to local title costs and customary real estate practices.

If you spend, say, $500 on an AOL, you might save $2,700 in Texas. In other areas, you may only save a few hundred dollars, if anything.

Part of your decision will be finding out how much title and AOL costs and seeing if the savings justify the risks.

How Much Does an Attorney Opinion Letter Cost?

The cost of an AOL is harder to pinpoint.

A major lender offers AOLs as part of the closing process for $350, says Banker and Tradesman. Another company charges $1,500 for a $400,000 loan, but includes “law firm protections” if issues arise.

The cost could vary widely with an individual lawyer. While Forbes reports that the average hourly fee for legal services was $313 in 2022, it’s hard to say how many hours it would take a lawyer to complete the AOL.

If AOLs become common practice, expect to see companies or law firms charging flat rates, or at least less confusing fee structures compared to title insurance companies.

Strategy: Use an AOL to Replace Lender’s Title Policy

As mentioned, two title insurance policies are issued with most sales: a lender’s policy and owner’s policy.

The lender’s policy protects the lender for the loan amount. The owner’s policy covers the home price and owner.

Loan agencies and lenders do not require that the homeowner get an owner’s title policy. It only requires:

A lender’s title policy, or

An AOL

One strategy would be to get an AOL for the lender’s title policy, but purchase title insurance to protect the home.

This doesn’t save as much money as using an AOL in lieu of both policies, but it protects you from the worst-case scenario.

Should You Consider an Attorney Opinion Letter?

No one can decide which route to take besides you. Much will depend on your tolerance for risk, local title fees, and AOL cost savings.

Just go into it realizing that an AOL is not the same thing as title insurance.